3 Growth Companies With High Insider Ownership And 15% Revenue Growth

Shift4 Payments FOUR | 0.00 |

The market has been flat in the last week but is up 27% over the past year, with earnings expected to grow by 17% annually in the coming years. In this context, growth companies with high insider ownership and significant revenue expansion can be particularly appealing as they often signal strong internal confidence and potential for sustained performance.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 33.4% | 74.1% |

| Upstart Holdings (UPST) | 13% | 58.1% |

| QT Imaging Holdings (QTI) | 23.9% | 103% |

| Laird Superfood (LSF) | 16.1% | 115.9% |

| KVH Industries (KVHI) | 16.3% | 146.1% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| Corcept Therapeutics (CORT) | 11.8% | 48.7% |

| Astera Labs (ALAB) | 10.7% | 31.5% |

| AppLovin (APP) | 27.4% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.7% | 32.9% |

Below we spotlight a couple of our favorites from our exclusive screener.

Niagen Bioscience (NAGE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Niagen Bioscience, Inc. is a bioscience company focused on developing healthy aging products, with a market cap of $299.29 million.

Operations: The company's revenue is primarily derived from Consumer Products at $98.58 million, followed by Ingredients at $29.07 million, and Analytical Reference Standards and Services contributing $2.69 million.

Insider Ownership: 29.5%

Revenue Growth Forecast: 15.6% p.a.

Niagen Bioscience is experiencing significant earnings growth, forecasted at 23% annually, outpacing the broader US market. Despite its revenue growth being slower than 20%, it still surpasses the US market average. Trading significantly below estimated fair value, Niagen's recent initiatives include launching an innovative telehealth platform and expanding strategic alliances to bolster its NAD+ product line. Recent financials show improved earnings and a completed share buyback program worth $2.61 million (US$).

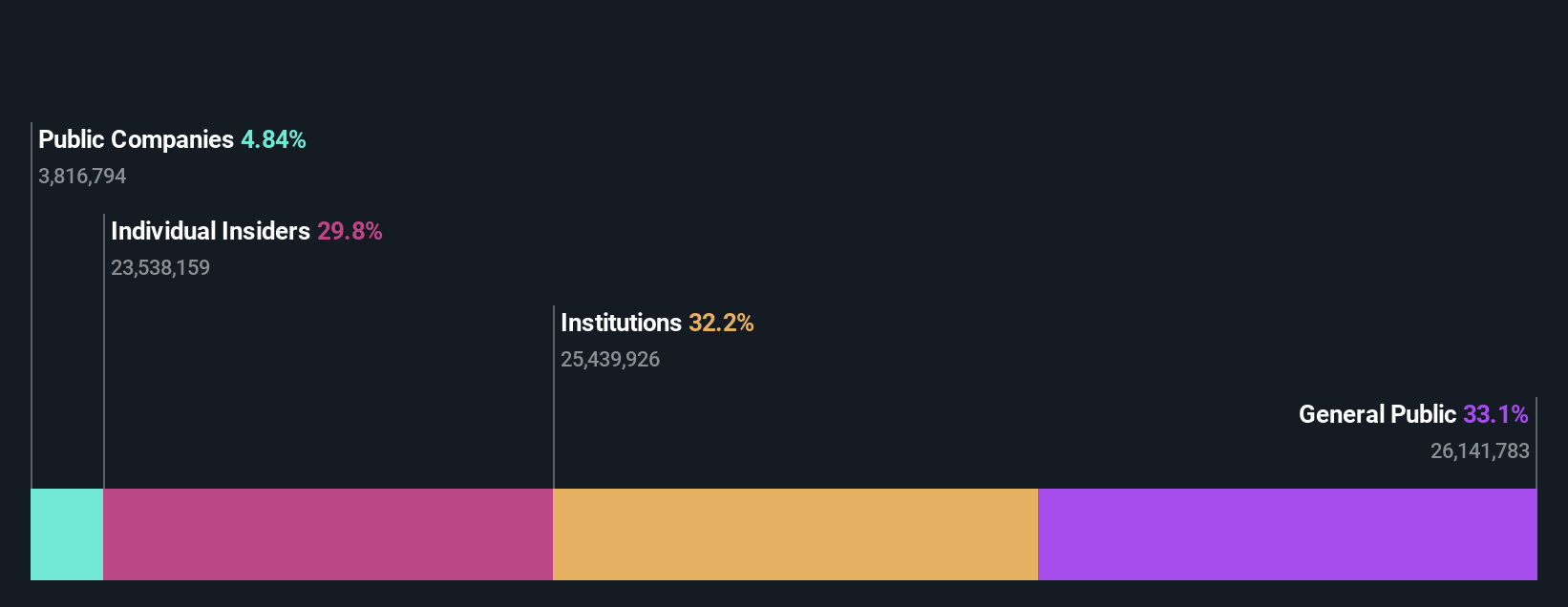

Shift4 Payments (FOUR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shift4 Payments, Inc. provides software and payment processing solutions both in the United States and internationally, with a market cap of $3.35 billion.

Operations: The company's revenue primarily comes from its data processing segment, which generated $4.45 billion.

Insider Ownership: 24.1%

Revenue Growth Forecast: 13.7% p.a.

Shift4 Payments is seeing substantial insider buying, indicating confidence in its growth prospects. The company recently partnered with Lydian to enhance its Pay with Crypto solution, allowing merchants to accept Tether without handling digital assets. Despite a volatile share price and lower profit margins compared to last year, Shift4's earnings are forecasted to grow significantly at 40% annually, outpacing the US market. Recent partnerships with major sports venues highlight its expanding commerce technology footprint.

Clear Secure (YOU)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Clear Secure, Inc. operates a secure identity platform under the CLEAR brand name primarily in the United States and has a market cap of approximately $8.29 billion.

Operations: The company's revenue is primarily derived from its Secure Biometric Identity Verification segment, which generated $942.41 million.

Insider Ownership: 11.2%

Revenue Growth Forecast: 14.5% p.a.

Clear Secure's high insider ownership underscores confidence in its growth trajectory. Recent strategic collaborations, such as with General Dynamics Information Technology and Expedia, enhance Clear's digital identity solutions across federal and travel sectors. Despite recent insider selling and a volatile share price, Clear reported strong Q1 results with US$253 million in sales and a 22.8% revenue growth forecast for Q2 2026. The company's expansion into new airports supports regional economic impact while maintaining robust earnings growth expectations above the market average.

Next Steps

- Gain an insight into the universe of 176 Fast Growing US Companies With High Insider Ownership by clicking here.

- Contemplating Other Strategies? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.