3 Growth Companies With High Insider Ownership And Earnings Up To 73%

Allegiant Travel Company ALGT | 0.00 |

The United States market has shown a steady trajectory, remaining flat over the last week but rising 20% in the past year, with earnings projected to grow by 18% annually in the coming years. In this environment, growth companies with high insider ownership can be appealing as they often indicate confidence from those closest to the business and align interests between insiders and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 69.4% |

| Upstart Holdings (UPST) | 14.1% | 60.1% |

| Laird Superfood (LSF) | 16.7% | 115.9% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| IREN (IREN) | 13.6% | 38.8% |

| ERock (EROC) | 20.1% | 56.3% |

| Corcept Therapeutics (CORT) | 10.9% | 48.9% |

| Cerebras Systems (CBRS) | 10.9% | 73.7% |

| AppLovin (APP) | 23.2% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.2% | 32.9% |

Let's dive into some prime choices out of the screener.

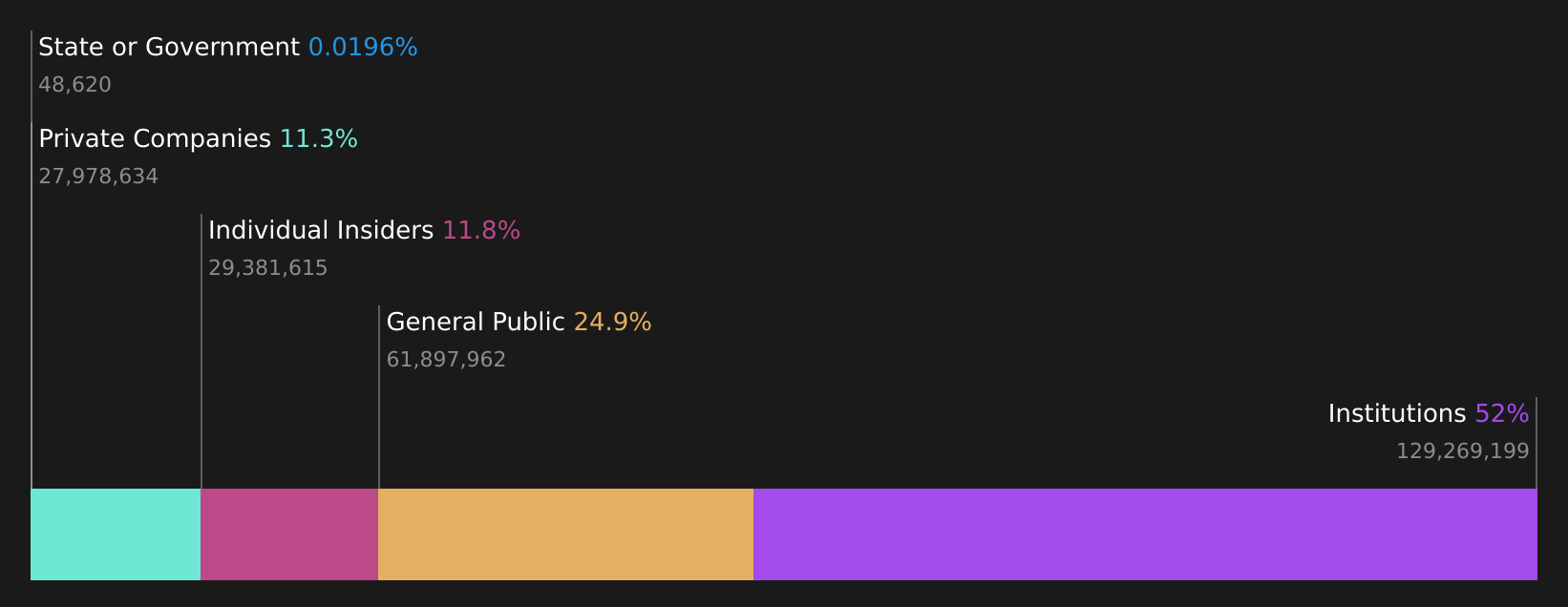

Allegiant Travel (ALGT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Allegiant Travel Company is a leisure travel provider offering services and products to residents of under-served U.S. cities, with a market cap of approximately $2.96 billion.

Operations: The company's revenue primarily comes from its airline segment, generating approximately $2.61 billion.

Insider Ownership: 10.1%

Earnings Growth Forecast: 73.5% p.a.

Allegiant Travel is poised for growth, with revenue expected to rise at 18.1% annually, surpassing the US market average. Despite recent shareholder dilution and low forecasted return on equity, Allegiant's expansion into new routes and its strategic refinancing of $650 million in debt reflect a proactive growth strategy. The company aims to become profitable within three years while managing interest payments effectively. Recent insider ownership data is unavailable, but no significant insider trading activity has been reported recently.

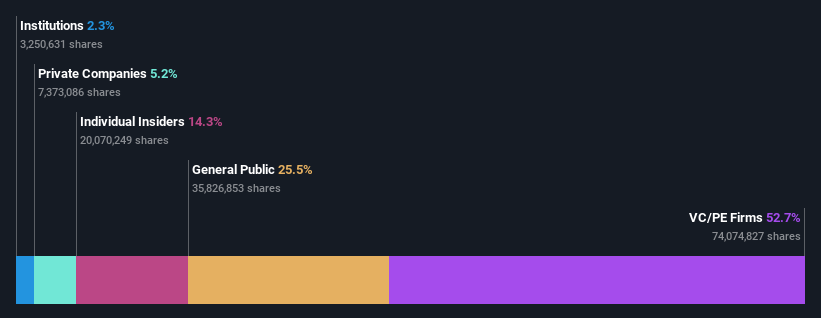

Circle Internet Group (CRCL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Circle Internet Group, Inc. operates as a platform, network, and market infrastructure for stablecoin and blockchain applications with a market cap of $16.44 billion.

Operations: The company generates revenue from data processing services, amounting to $2.86 billion.

Insider Ownership: 11.8%

Earnings Growth Forecast: 48.9% p.a.

Circle Internet Group is expanding its digital asset infrastructure, having received OCC approval to establish Circle National Trust, a federally regulated bank. This move enhances USDC's regulatory framework and aligns with Circle's growth strategy amid volatile share price trends. Despite low forecasted return on equity, revenue is expected to grow at 21% annually, outpacing the US market. Recent insider activity shows more shares bought than sold but not in substantial volumes.

Karman Holdings (KRMN)

Simply Wall St Growth Rating: ★★★★★★

Overview: Karman Holdings Inc., through its subsidiary, focuses on designing, testing, manufacturing, and selling mission-critical systems in the United States with a market cap of $6.63 billion.

Operations: The company's revenue segment includes the Space and Defense Industry, generating $522.59 million.

Insider Ownership: 15.6%

Earnings Growth Forecast: 52.6% p.a.

Karman Holdings is poised for significant growth, with revenue expected to increase by 27.8% annually, outpacing the US market. Despite challenges in covering interest payments with earnings, Karman's earnings are forecasted to grow significantly at 52.6% per year. Recent strategic moves include a follow-on equity offering raising US$854 million and leadership changes aimed at enhancing AI capabilities and growth strategy execution. The company also secured potential demand commitments worth over $1 billion from key defense clients.

Seize The Opportunity

- Click this link to deep-dive into the 164 companies within our Fast Growing US Companies With High Insider Ownership screener.

- Searching for a Fresh Perspective? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.