3 High‑Quality Undiscovered Gems With Standout ROE And Margins

Oceaneering International, Inc. OII | 0.00 |

With inflation pressures tied to energy and freight, shifting central bank policies, and uneven growth across regions, many investors are looking beyond the usual large cap stocks. That is where the High-Quality Undiscovered Gems screener comes in. It focuses on smaller companies with solid fundamentals that are less crowded by big funds. By targeting stocks that are not heavily owned by institutions, you are not just following the usual playbook; you are looking where others are not paying full attention. In this article, you will see 3 of the standout stocks filtered by this screener.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Oceaneering International (OII)

Overview: Oceaneering International provides engineered services, products, and robotic solutions to offshore energy, defense, aerospace, and manufacturing customers across multiple regions, using subsea robotics, specialized hardware, and advanced inspection services to support complex operations. Its five segments span remotely operated vehicles, subsea hardware and connectors, offshore installation services, asset integrity and digital tools, and aerospace and defense technologies.

Operations: Oceaneering generates most of its roughly US$2.8b in revenue from energy focused segments, led by Energy - Subsea Robotics at about US$863.5m, Energy - Offshore Projects Group at about US$586.5m, Energy - Manufactured Products at about US$577.6m, and Aerospace and Defense Technologies at about US$494.0m, with smaller contributions from Energy - Integrity Management & Digital Solutions.

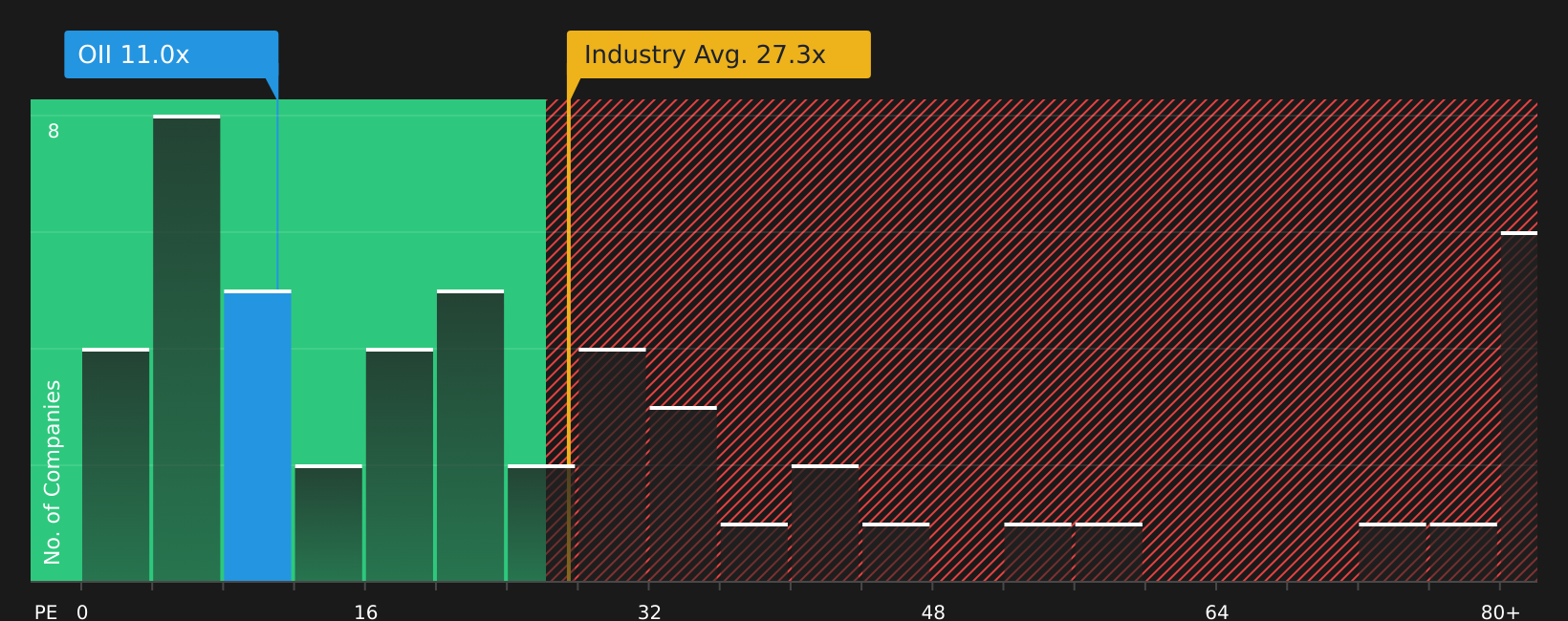

Market Cap: US$4.0b

Oceaneering International sits at the crossroads of offshore energy and high end robotics, offering exposure to subsea services and growing aerospace and defense work, while carrying real risks from the global energy transition and intense competition. The company combines a 30.5% return on equity and a 12.1% net margin with a relatively low P/E, plus recent contract wins such as the West Delta Deep Marine project that support its service pipeline. At the same time, analysts expect earnings to decline over the next few years and insider selling has picked up. To understand how factors such as business quality and contract visibility might interact with the earnings outlook and funding risks, it can be useful to look beyond the headline valuation and short term share price moves.

High return on equity, a double digit net margin, and a relatively low P/E can make Oceaneering look like a straightforward value story, but the real twist might sit inside the 2 key rewards and 2 important warning signs (1 is major!)

Yuanbao (YB)

Overview: Yuanbao is a Beijing based insurance platform that connects customers across China with medical, critical illness, accident, property, and pet insurance policies through licensed brokerage and agency services.

Operations: Yuanbao generates all of its roughly CN¥4.4b in revenue from insurance brokerage in Mainland China.

Market Cap: US$685.2m

Yuanbao stands out as a pure play on China’s online insurance distribution, with earnings that have grown very quickly in recent years and a net profit margin that widened from 13.3% to 45.9%. The stock trades on a low P/E relative to the US insurance sector. Analysis suggests there is a large gap between its current price and estimated cash flow value, which may interest value focused investors. At the same time, the business relies entirely on higher risk external borrowing rather than customer deposits and board independence is limited, so capital structure and governance deserve close attention before relying on the strong current return on equity and high quality earnings profile.

Surging margins and a low P/E can make Yuanbao look like a straightforward growth story, but the real question is whether that earnings strength is built to last, as the analysis report for Yuanbao starts to reveal.

Exzeo Group (XZO)

Overview: Exzeo Group provides an Insurance as a Service platform that runs core functions for property and casualty insurers, handling quoting, underwriting, policy and claims administration, and financial and data reporting for carriers and agents.

Operations: Exzeo generates about US$226.5m in revenue from property and casualty insurance services, all from customers in the United States.

Market Cap: US$1.1b

Exzeo Group provides direct exposure to the digital plumbing of property and casualty insurance, where insurers are shifting core systems onto cloud platforms. Exzeo already supports US$1.2b of managed premium with high margins and no debt, alongside more than US$140m of cash. Earnings growth has been very strong, supported by a 31% return on equity and a 36.1% net margin, and a new share repurchase program signals management’s confidence. The catch is that funding relies entirely on external borrowing and client exposure still leans heavily on Florida homeowners, so any hit to that market or tighter funding conditions could be challenging. How those strengths and pressure points balance out is what makes Exzeo particularly notable within this screener.

High margins, a 31% return on equity and more than US$140m of cash with no debt can make Exzeo look like a rare insurance tech engine, but the real story inside the analyst forecasts for Exzeo Group may explain why its Florida exposure and funding mix could matter much more than the headline numbers suggest.

The three stocks discussed here are just a starting point, as the full screener has identified 19 more companies with equally compelling narratives that could fit the same High-Quality Undiscovered Gems idea using the High-Quality Undiscovered Gems screener. Unlock deeper opportunities by using Simply Wall St to filter for the catalysts and storylines that matter most to you, so you can identify and analyze the highest conviction small cap ideas on your terms.

Take Control of Your Investment Journey

If Exzeo Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move fast, and the sharpest opportunities often gain momentum or drop off the radar before the crowd reacts. Scan these focused shortlists now and consider them before they become widely followed.

- Spot steady income candidates by reviewing 10 dividend fortresses that prioritize robust payouts and balance sheet strength while those yields are still flying under most investors’ radar.

- Evaluate potential infrastructure-related candidates by scanning 33 power grid technology and infrastructure stocks built around companies tied to grid upgrades, electrification, and critical hardware before capital flows fully catch up.

- Follow the computing shift by tracking 48 AI infrastructure stocks featuring businesses supporting AI demand with chips, data centers, and connectivity while they are still relatively under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.