3 Large Cap Dividend Stocks Worth Watching As Fed Rate Pressure Builds

Illinois Tool Works Inc. ITW | 0.00 |

With June inflation at 3.5% and a rare 0.4% monthly price decline driven by cheaper energy, income focused investors are weighing what shifting price pressures and a watchful Federal Reserve could mean for large dividend paying stocks. At the same time, renewed US Iran tensions keep the outlook for energy costs and future inflation uncertain, while the Fed signals that interest rates may stay higher for longer or even rise further. In this context, three large cap dividend stocks from the screener stand out as being closely tied to these cross currents, for better or worse.

A. O. Smith (AOS)

Overview: A. O. Smith is a long established Milwaukee based manufacturer of water heaters, boilers and water treatment systems used in homes, offices, hospitals, hotels and other commercial buildings across North America, China, Europe and India, selling through wholesale distributors, big box retailers, dealers and direct to consumers online.

Operations: A. O. Smith generates most of its revenue in North America at about US$3.0b, with roughly US$0.9b from the Rest of World and a small inter segment elimination of US$31.4m.

Market Cap: US$8.2b

Investors looking for steady income in a choppy inflation backdrop may find A. O. Smith interesting because it pairs a long dividend record with high profitability, including a 28.1% return on equity and resilient 13.8% net margins. The stock currently trades on a P/E below both peers and the broader US Building industry, while analyst and DCF estimates suggest it is below assessed fair value. At the same time, leadership changes, modest earnings growth expectations and ongoing China weakness highlight that execution and geographic risk are real issues to watch. With pricing actions, efficiency efforts and a strong balance sheet, the company offers a mix of quality, income and valuation that warrants a closer look.

A. O. Smith’s mix of high profitability, long dividend record and a P/E below peers raises a simple question: is the market missing something in the current valuation and risk balance? Walk through the DCF valuation analysis for A. O. Smith to see what might be hiding in the assumptions.

Illinois Tool Works (ITW)

Overview: Illinois Tool Works is a long established industrial group that makes a wide range of everyday but essential equipment and components, from auto parts and welding gear to commercial kitchen appliances and packaging machinery, serving manufacturers and service providers across major global end markets.

Operations: Illinois Tool Works generates most of its revenue from Automotive OEM at about US$3.3b, Test & Measurement and Electronics at US$2.9b, Food Equipment at US$2.7b, Welding at US$1.9b, Construction Products at US$1.8b, Polymers & Fluids at US$1.8b, and Specialty Products at US$1.8b, with a small intersegment elimination of US$17m.

Market Cap: US$78.1b

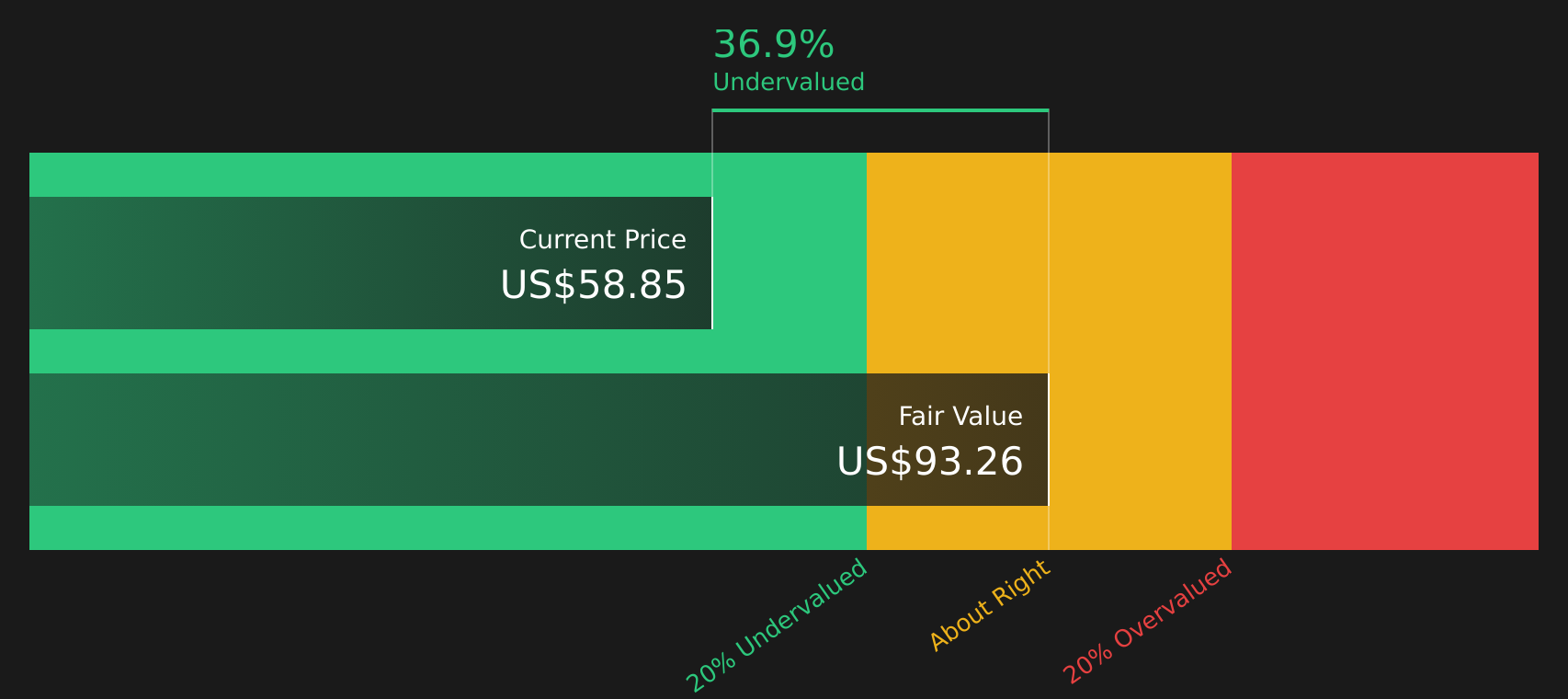

Income focused investors watching inflation cool but interest rates stay higher for longer may see Illinois Tool Works as a useful anchor, combining a long record of growing dividends with high margins, a 2.37% yield and a P/E below the Machinery industry average. The company is leaning on cost and margin initiatives, a decentralized structure and customer focused product development to support earnings, even as some segments and regions face softer demand and tariffs remain a swing factor. With active buybacks, modest but steady growth expectations and a balance of positives and risks that analysts see as roughly fairly priced, Illinois Tool Works becomes a stock where the details really matter.

Illinois Tool Works’ mix of a long dividend record, high margins and a P/E below the Machinery industry suggests the full story may not be priced in yet. The analysis report for Illinois Tool Works could reveal what the headline numbers are glossing over

MSC Industrial Direct (MSM)

Overview: MSC Industrial Direct is a large distributor of metalworking and maintenance, repair and operations products, supplying everything from cutting tools and abrasives to safety gear, janitorial supplies and power tools to machine shops, manufacturers and government customers across North America and abroad.

Operations: MSC Industrial Direct generates all of its roughly US$3.9b in revenue from distributing metalworking and MRO products and services, with the vast majority coming from the United States and smaller contributions from Canada, Mexico and other foreign markets.

Market Cap: US$6.9b

MSC Industrial Direct offers a mix of reliable income, with a 2.8% dividend yield, and exposure to an industrial cycle that could matter more if inflation cools but rates stay relatively high and investors look for cash generative large caps. The company is investing in In Plant programs, vending machines and a better ecommerce experience to support revenue and margin improvement. It also carries risks from softer demand, tariff exposure and an earnings multiple that sits above Trade Distributors peers. For investors weighing whether MSC Industrial Direct is priced fairly for its growth and cost saving plans, the real question is how much of that future is already reflected in today’s valuation and recent analyst optimism.

MSC Industrial Direct’s mix of a 2.8% yield, higher P/E than peers and heavy investment in In Plant, vending and ecommerce suggests something in the story is still underappreciated. The analyst forecasts for MSC Industrial Direct could clarify whether the market is overlooking a key twist or quietly bracing for one.

The three dividend stocks discussed so far are just a starting point. The full US, UK, Canada, Australia and New Zealand screener surfaces 17 more large cap companies with steady payouts and equally compelling income and stability stories through the Large Cap Dividend Stocks screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction large cap dividend opportunities.

Take Control of Your Investment Journey

If MSC Industrial Direct or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Dividends?

Some stocks are building quiet momentum while others risk getting caught dropping before the crowd notices. Scan these fresh ideas under the radar for now, and consider acting before they become more widely followed.

- Spot potential income opportunities by scanning a curated 8 dividend fortresses that appear structured to maintain payouts even if conditions remain choppy.

- Explore growth stories with balance sheet strength by running the list of solid balance sheet and fundamentals (48 results) so weaker companies are filtered out before they reach your watchlist.

- Follow the trend toward automation and efficiency by checking the 33 robotics and automation stocks featuring companies involved with robots, sensors, and factory upgrades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.