3 Promising Undervalued Small Caps With Insider Action In June 2026

Azenta, Inc. AZTA | 0.00 |

Over the last 7 days, the United States market has experienced a 2.7% decline, yet it remains up by 19% over the past year with earnings projected to grow by 18% annually. In this dynamic environment, identifying promising small-cap stocks that are perceived as undervalued and exhibit insider activity can offer intriguing opportunities for investors seeking potential growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 9.6x | 0.8x | 45.64% | ★★★★★★ |

| Appian | 1711.3x | 2.0x | 40.70% | ★★★★★☆ |

| Kingstone Companies | 7.9x | 1.1x | 45.54% | ★★★★☆☆ |

| Bank of the James Financial Group | 10.1x | 2.2x | 20.56% | ★★★★☆☆ |

| Angel Oak Mortgage REIT | 13.7x | 6.2x | 22.31% | ★★★★☆☆ |

| Similarweb | NA | 1.6x | 33.19% | ★★★★☆☆ |

| German American Bancorp | 13.0x | 4.8x | 40.32% | ★★★☆☆☆ |

| Patria Investments | 24.3x | 4.4x | 10.52% | ★★★☆☆☆ |

| NameSilo Technologies | 423.8x | 2.0x | 41.28% | ★★★☆☆☆ |

| National Vision Holdings | 31.0x | 0.7x | 34.65% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

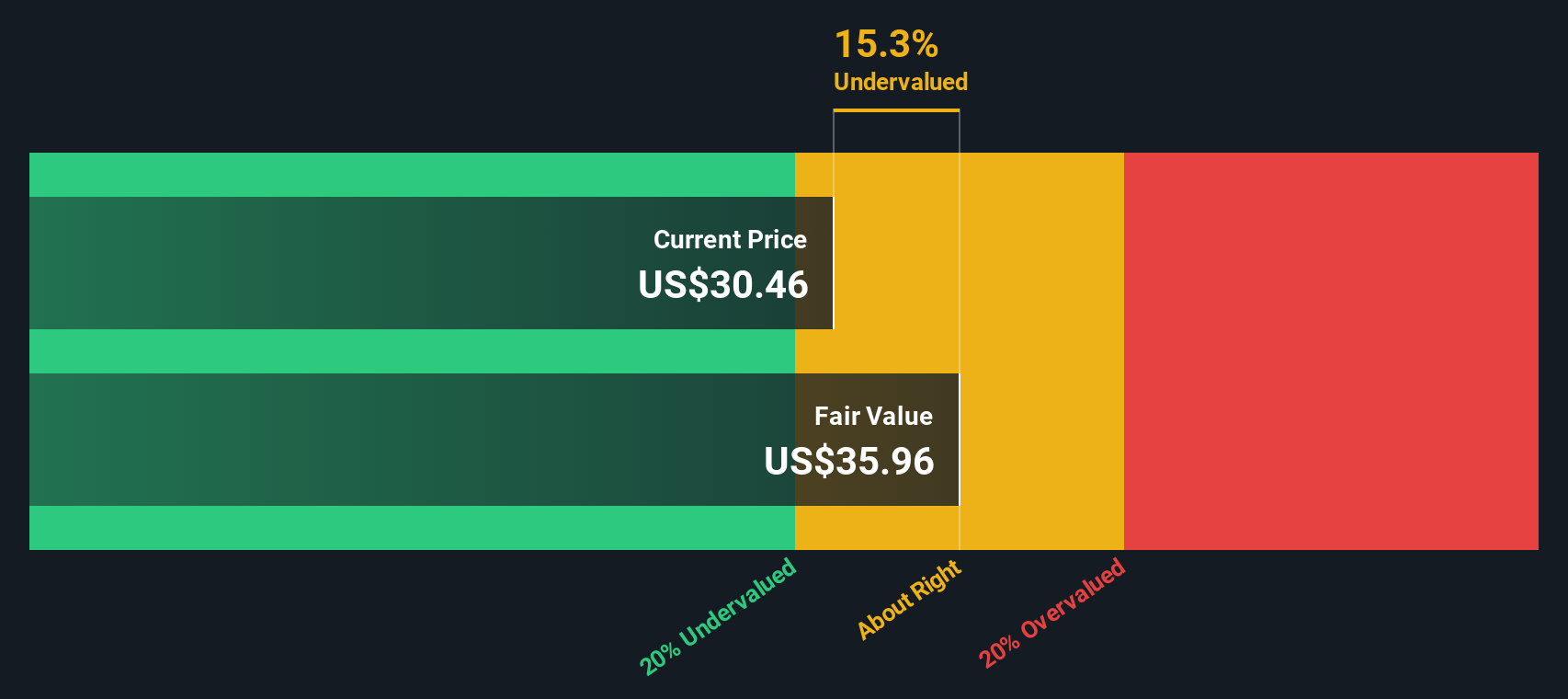

Azenta (AZTA)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Azenta operates in the life sciences sector, focusing on multiomics and sample management solutions, with a market cap of approximately $4.46 billion.

Operations: Azenta generates revenue primarily from its Multiomics and Sample Management Solutions segments, with the latter contributing slightly more to total revenue. The company's gross profit margin has fluctuated over time, reaching 45.52% as of September 2025. Operating expenses, including R&D and general & administrative costs, significantly impact profitability.

PE: -10.2x

Azenta, a company with promising growth potential, has caught attention due to insider confidence shown by William Cornog's purchase of 10,000 shares for US$163,800 in early 2026. Despite reporting a net loss of US$160.8 million for Q2 2026 and impairment charges of US$149 million, the company forecasts revenue between US$603 million and US$621 million for fiscal year ending September 30, 2026. The appointment of Trey Martin as President aims to enhance their Multiomics business strategy.

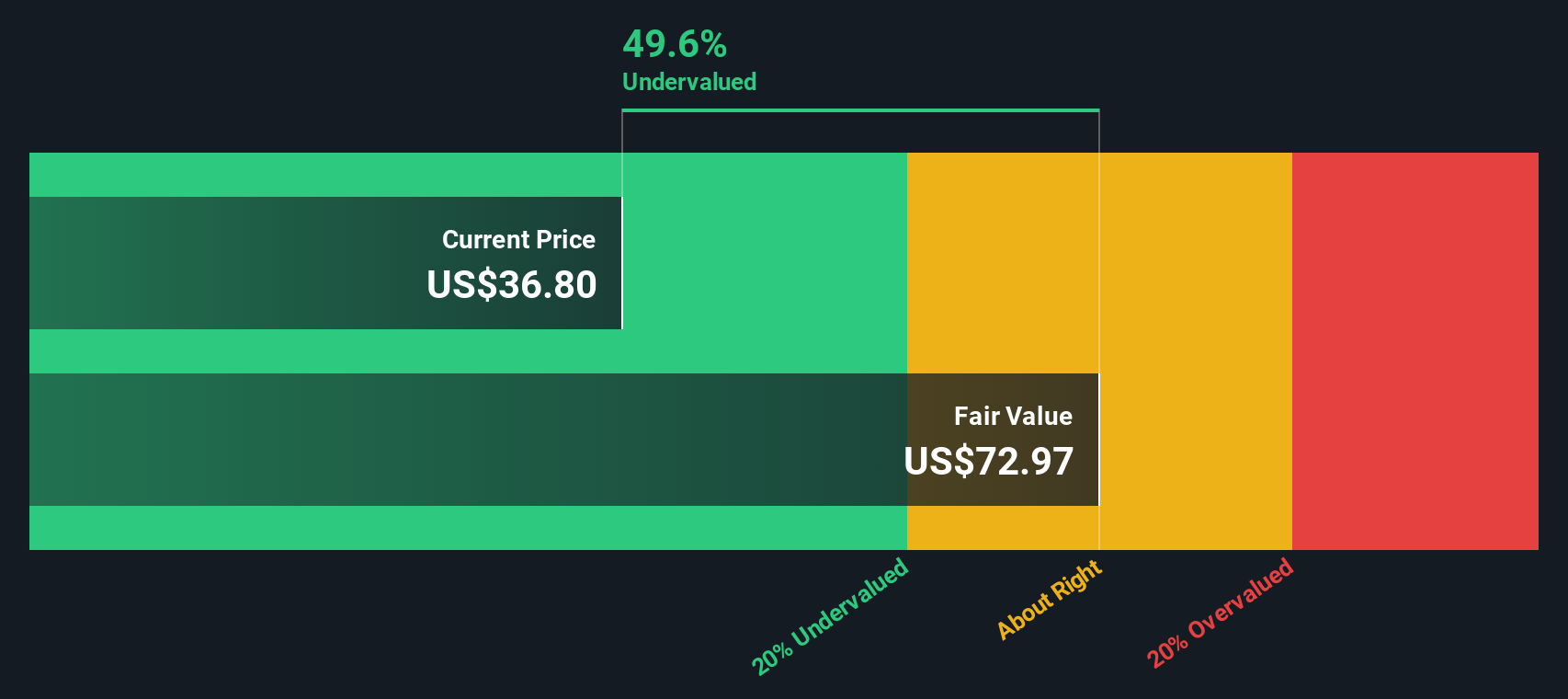

German American Bancorp (GABC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: German American Bancorp operates as a financial services holding company providing core banking, wealth management, and other financial services, with a market capitalization of approximately $1.16 billion.

Operations: Core Banking is the primary revenue source at $310.60 million, complemented by Wealth Management Services generating $17.86 million. Operating expenses are significant, with General & Administrative Expenses consistently forming a large portion of costs. The company has seen variations in its net income margin, which was 36.56% in March 2026 and 29.34% in March 2025, reflecting changes in profitability over time.

PE: 13.0x

German American Bancorp, a smaller player in the financial sector, shows potential with earnings projected to grow 5.83% annually. Their recent AGM approved doubling authorized shares to 90 million, hinting at strategic expansion plans. Insider confidence is evident from share purchases earlier this year. The first quarter saw net interest income rise to US$78.85 million and net income jump to US$33.15 million, reflecting strong operational performance despite increased charge-offs of US$1.15 million compared to last year's US$486,000.

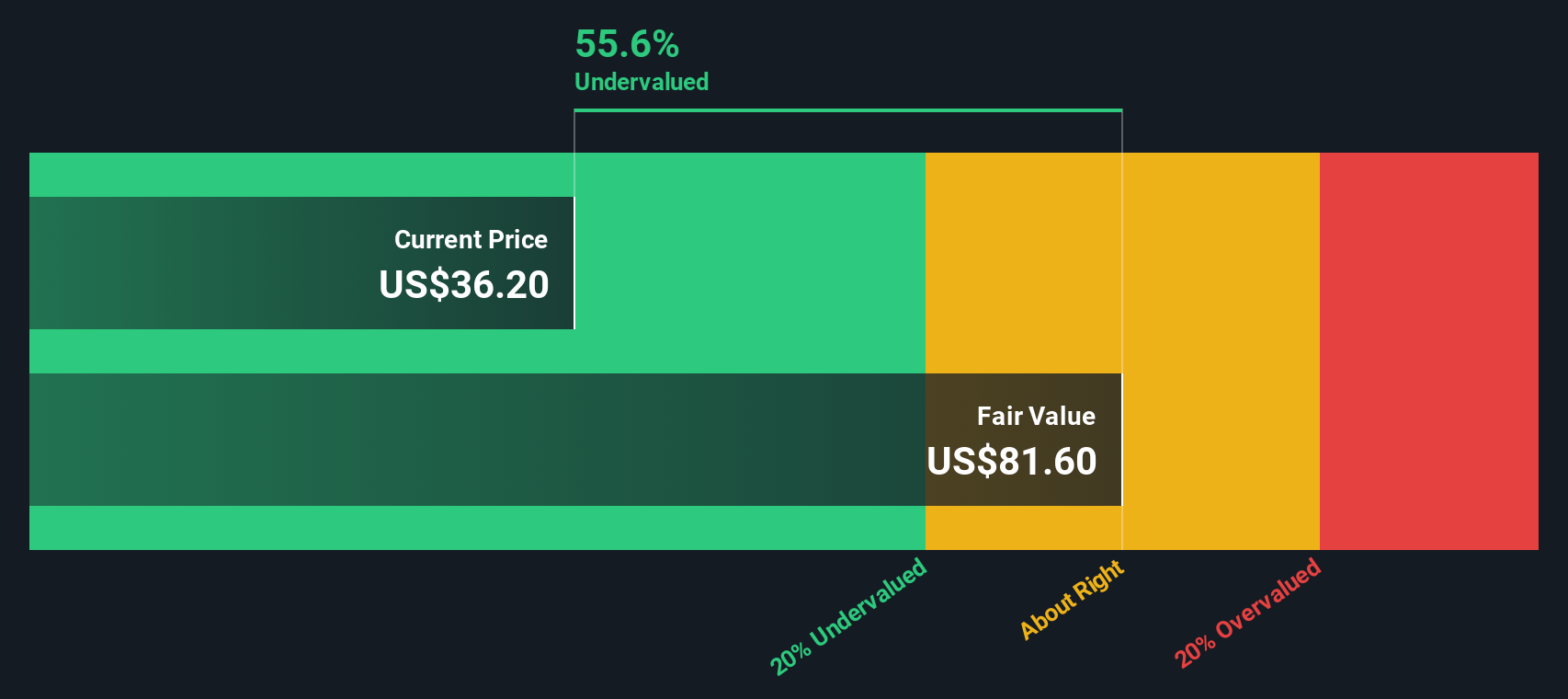

PAR Technology (PAR)

Simply Wall St Value Rating: ★★★★★☆

Overview: PAR Technology provides software and hardware solutions for the restaurant and retail industries, with a focus on point-of-sale systems, and has a market cap of approximately $1.52 billion.

Operations: PAR Technology generates revenue primarily from its Restaurant/Retail segment, reporting $475.66 million in recent data. The company has seen fluctuations in its gross profit margin, recently reaching 43.67%. Operating expenses include significant allocations for R&D and General & Administrative costs, impacting overall financial performance.

PE: -8.6x

PAR Technology, a smaller company in the U.S., is making strides with recent partnerships and technological advancements. They secured deals with Bolla Oil Corporation and Pizza Factory, enhancing customer engagement through loyalty programs and modernized restaurant tech. Despite a net loss of US$16 million in Q1 2026, revenue rose to US$124 million from the previous year. Insider confidence is evident as Director Keith Pascal purchased 13,000 shares for US$197,080 this June. With ongoing innovations like PAR Intelligence and strategic buybacks totaling over 2 million shares earlier this year, there's potential for growth despite current unprofitability challenges.

Turning Ideas Into Actions

- Click this link to deep-dive into the 63 companies within our Undervalued US Small Caps With Insider Buying screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.