3 Stocks Retail Investors Should Watch As Tariffs Raise Pressure on 3M and Kohl's

Kohl's Corporation KSS | 0.00 |

Tariff headlines are back at the center of the market conversation, with President Trump pushing for broad new charges on imports from the EU and dozens of other countries, while legal challenges and rising costs for businesses add to the uncertainty. For investors, that kind of policy volatility tends to reward close attention to companies most exposed to shifting trade rules and imported inputs. This article breaks down three stocks from the Tariff Exposure Plays Amid Volatile US Trade Policy Risks screener that appear more vulnerable to these moves, helping you identify where tariff pressure might be building into the story.

3M (MMM)

Overview: 3M is a global industrial and consumer products company that makes everything from factory abrasives and auto repair materials to healthcare supplies and household staples like cleaning products and adhesives, selling into industries such as automotive, electronics, construction, energy, government, and transportation.

Operations: 3M generates most of its revenue from Safety and Industrial products at US$11.6b, followed by Transportation and Electronics at US$8.3b and Consumer products at US$4.9b, with meaningful exposure to the United States and a broad international footprint.

Market Cap: US$83.0b

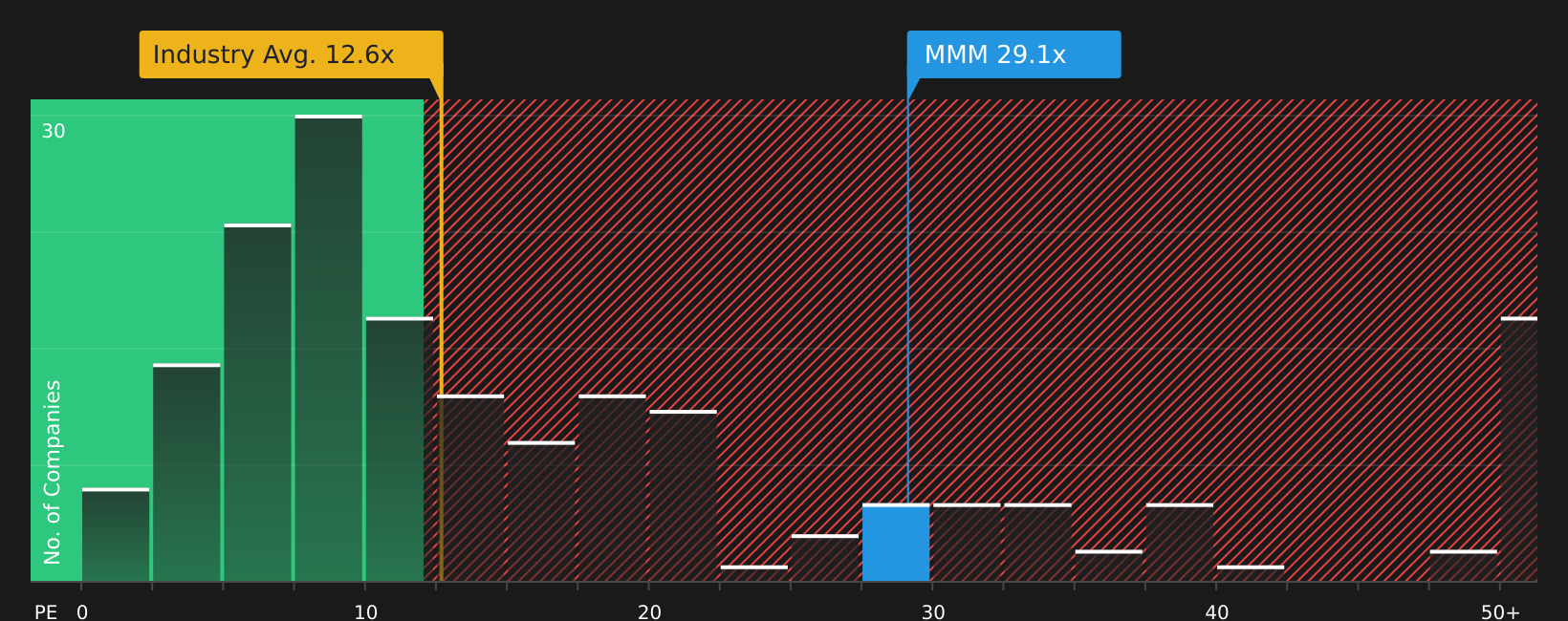

Investors watching tariff headlines may monitor 3M, because a global manufacturing network that imports US$1.6b into the US and exports US$4.1b from it leaves the company exposed to rising trade barriers and higher input costs. Management has flagged up to US$850m of potential annual tariff impact before mitigation, in addition to existing legal and PFAS liabilities that already pressure margins and keep debt elevated. Recent analyst commentary and buy ratings highlight potential upside if litigation fears ease. However, earnings volatility, tariff sensitivity and a high P/E relative to many industrial peers mean the risk side of 3M’s situation is significant, and a key consideration is how much of that risk is already reflected in today’s price.

3M’s tariff exposure, heavy litigation and elevated P/E could be masking deeper pressure on its balance sheet, so it may be worth reviewing the 3M financial health report

Kohl's (KSS)

Overview: Kohl's is a US omnichannel department store chain that sells apparel, footwear, accessories, beauty, and home products through a large store network and its website, leaning heavily on a mix of in house brands like Sonoma Goods for Life and Apt. 9 alongside well known labels such as LC Lauren Conrad and Simply Vera Vera Wang.

Operations: Kohl's generates all of its US$15.5b in revenue from department store retail in the United States.

Market Cap: US$1.9b

Investors looking at Kohl's are weighing a pressured middle income customer base, shrinking transactions and tariff exposed imports against a low valuation and a complicated turnaround story. Management highlights cost discipline, proprietary brands and the Sephora rollout as margin supports. However, tariffs on imported inventory, heavier promotions and wage inflation all push in the opposite direction, especially with US consumers already cutting discretionary spend. Earnings benefited from a large one off gain, the dividend track record is uneven, and funding relies fully on external borrowing, which can matter if operating trends weaken. For anyone watching Kohl's, the key question is whether cost cuts and brand refreshes can offset these structural and tariff related headwinds before patience runs out.

Kohl's shrinking transactions and tariff exposed inventory may be masking deeper pressure underneath the low valuation story, so reviewing the analysis report for Kohl's could surface the real risk investors are underestimating

Kimberly-Clark (KMB)

Overview: Kimberly-Clark is a U.S. based consumer products company that manufactures and sells everyday personal care and tissue products, including diapers, wipes, feminine and incontinence care, toilet paper, paper towels, and professional hygiene supplies under brands such as Huggies, Pull-Ups, Goodnites, Kotex, Poise, Depend, Kleenex, Scott, Cottonelle, Viva, and Wypall.

Operations: Kimberly-Clark generates about US$10.7b in revenue from North America and US$5.8b from International Personal Care, with both segments focused on baby, adult and feminine care, wipes, and tissue products.

Market Cap: US$37.5b

Kimberly-Clark appears to be a classic “steady” consumer stock at first glance. However, investors may see reasons to be cautious. Earnings growth has been modest over five years, net margins have moved from 12.6% to 10.4%, and the dividend, while yielding 4.46%, is not well covered by earnings or free cash flow. High debt and a return on equity figure that is influenced by leverage add financial risk at a time when tariffs, including a recent US$300m cost impact, are raising input costs and complicating sourcing. The Kenvue deal and US$3b productivity program are central to the more optimistic view, yet execution risk is significant and the stock has already trailed both the US market and the Household Products sector. This leaves open questions about how resilient Kimberly-Clark may be if tariff pressure intensifies.

Kimberly-Clark’s high debt, thin dividend cover and rising tariff costs suggest the story might be more fragile than it looks. Before assuming “defensive,” read the 2 key rewards and 2 important warning signs (1 is major!)

Take Control of Your Investment Journey

If Kohl's or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh opportunities move quickly, and the stocks with real breakout potential rarely stay under the radar for long. Spot momentum shifts while it matters and get in early.

- Capture potential upside in early stage turnarounds by scanning 18 high quality undiscovered gems that have solid fundamentals before the wider market catches on.

- Ride powerful secular trends by tracking infrastructure companies through the 35 power grid technology and infrastructure stocks while capital is still rotating into the space.

- Target companies with room to grow and less balance sheet strain by filtering the list of solid balance sheet and fundamentals (47 results) before valuations get crowded.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.