3 Undervalued Small Caps With Insider Buying Across Regions

Arbor Realty Trust Inc ABR | 0.00 |

The United States market has shown robust performance, climbing 1.6% in the last week and rising 28% over the past year, with earnings expected to grow by 17% annually. In this thriving environment, identifying small-cap stocks that may be undervalued and exhibit insider buying can provide unique opportunities for investors looking to leverage potential growth across various regions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Financial Institutions | 9.2x | 3.0x | 29.47% | ★★★★★☆ |

| Angel Oak Mortgage REIT | 12.9x | 5.8x | 26.66% | ★★★★★☆ |

| AVITA Medical | NA | 1.8x | 47.33% | ★★★★★☆ |

| Ferroglobe | NA | 0.6x | 21.14% | ★★★★★☆ |

| First Bancorp | 9.0x | 3.4x | 30.27% | ★★★★☆☆ |

| New Peoples Bankshares | 8.8x | 2.3x | 20.57% | ★★★★☆☆ |

| Similarweb | NA | 1.3x | 40.81% | ★★★★☆☆ |

| Metropolitan Bank Holding | 12.9x | 3.7x | 40.25% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 34.36% | ★★★☆☆☆ |

| Angel Studios | NA | 1.3x | -42.42% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

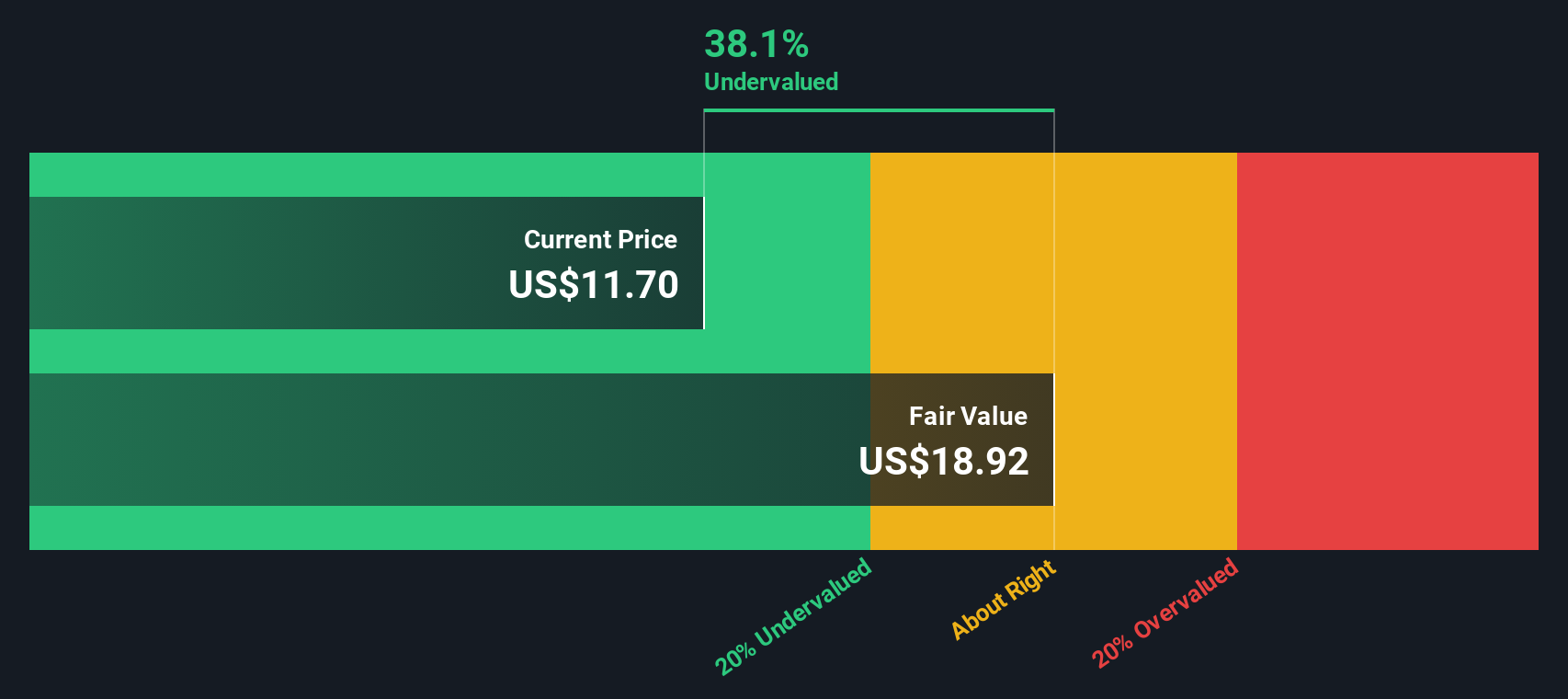

Arbor Realty Trust (ABR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Arbor Realty Trust is a real estate investment trust that primarily focuses on investing in a diversified portfolio of structured finance assets in the multifamily, single-family rental, and commercial real estate markets, with a market cap of approximately $2.95 billion.

Operations: The company generates revenue primarily from its Agency Business and Structured Business segments. Its gross profit margin has shown a trend of reaching up to 93.44% in recent periods, indicating efficient cost management relative to revenue. Operating expenses, including general and administrative costs, form a significant portion of the company's expenditure structure.

PE: 14.3x

Arbor Realty Trust, a smaller U.S. company, recently enhanced its financial flexibility by redeeming $787 million of notes and transferring $1.21 billion in assets to improved repurchase facilities with JPMorgan Chase Bank, N.A., boosting liquidity by $132.3 million. Despite a dip in net income to US$10.97 million for Q1 2026 from US$40.78 million the previous year, insider confidence is evident through share purchases earlier this year, suggesting potential growth prospects amidst current challenges like lower profit margins and impairment losses.

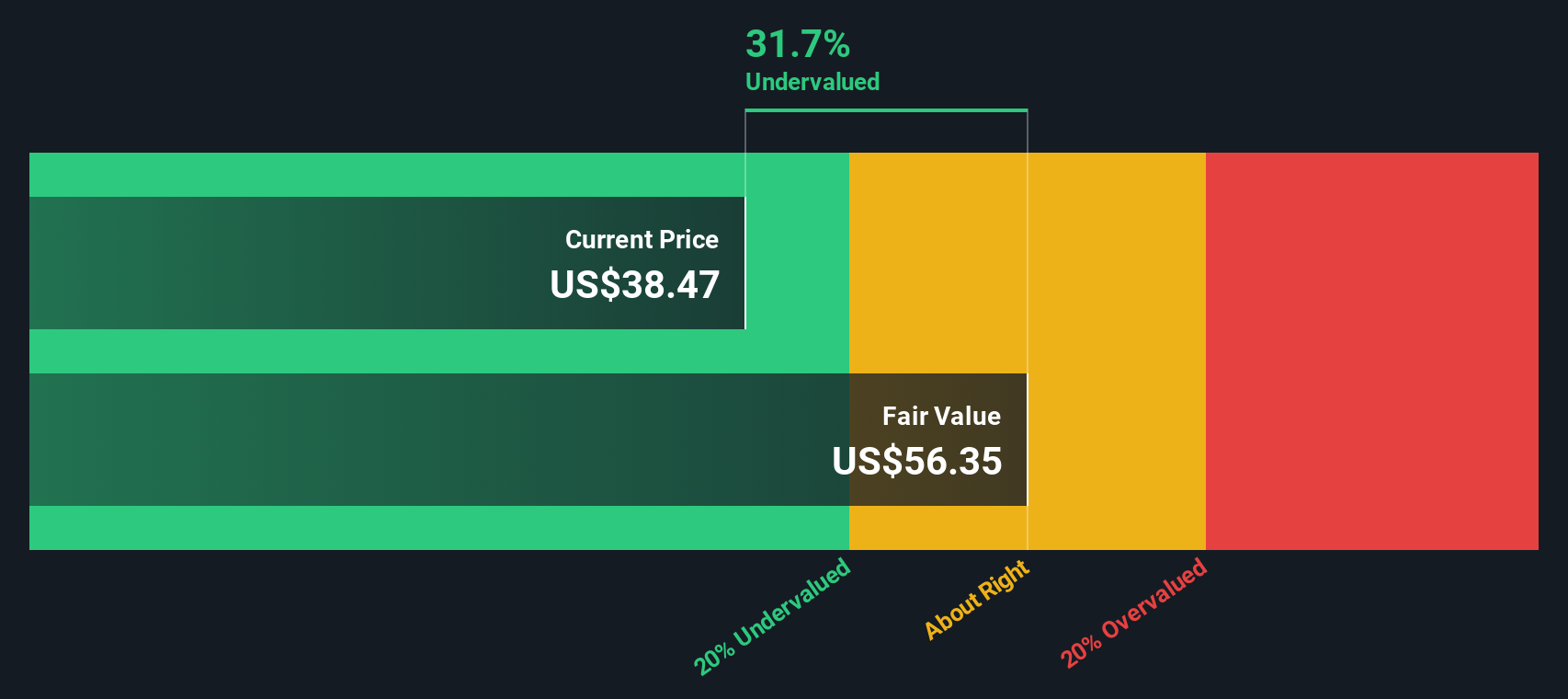

FMC (FMC)

Simply Wall St Value Rating: ★★★★★☆

Overview: FMC is a company that operates in the agricultural sciences sector, focusing on providing innovative solutions, with a market capitalization of approximately $13.45 billion.

Operations: The company's revenue primarily stems from its Innovative Solutions segment, with recent figures showing $3.43 billion in revenue. The gross profit margin has shown a notable downward trend, dropping to 32.09% as of March 2026. Operating expenses have been significant, with general and administrative costs being a major component alongside research and development expenses. Net income has experienced volatility, recently recording substantial losses driven by high non-operating expenses.

PE: -0.7x

FMC Corporation, a smaller player in the market, is catching attention with its recent financial maneuvers. Despite facing challenges like a net loss of US$281.3 million in Q1 2026 and declining sales, FMC's strategic debt offerings—US$1.2 billion and US$750 million notes—aim to refinance existing obligations and support corporate activities. The company's earnings are projected to grow significantly at 112% annually, hinting at potential recovery. Insider confidence through share purchases underscores belief in future prospects amid ongoing product innovations like Isoflex active's EU approval for agricultural use starting 2027.

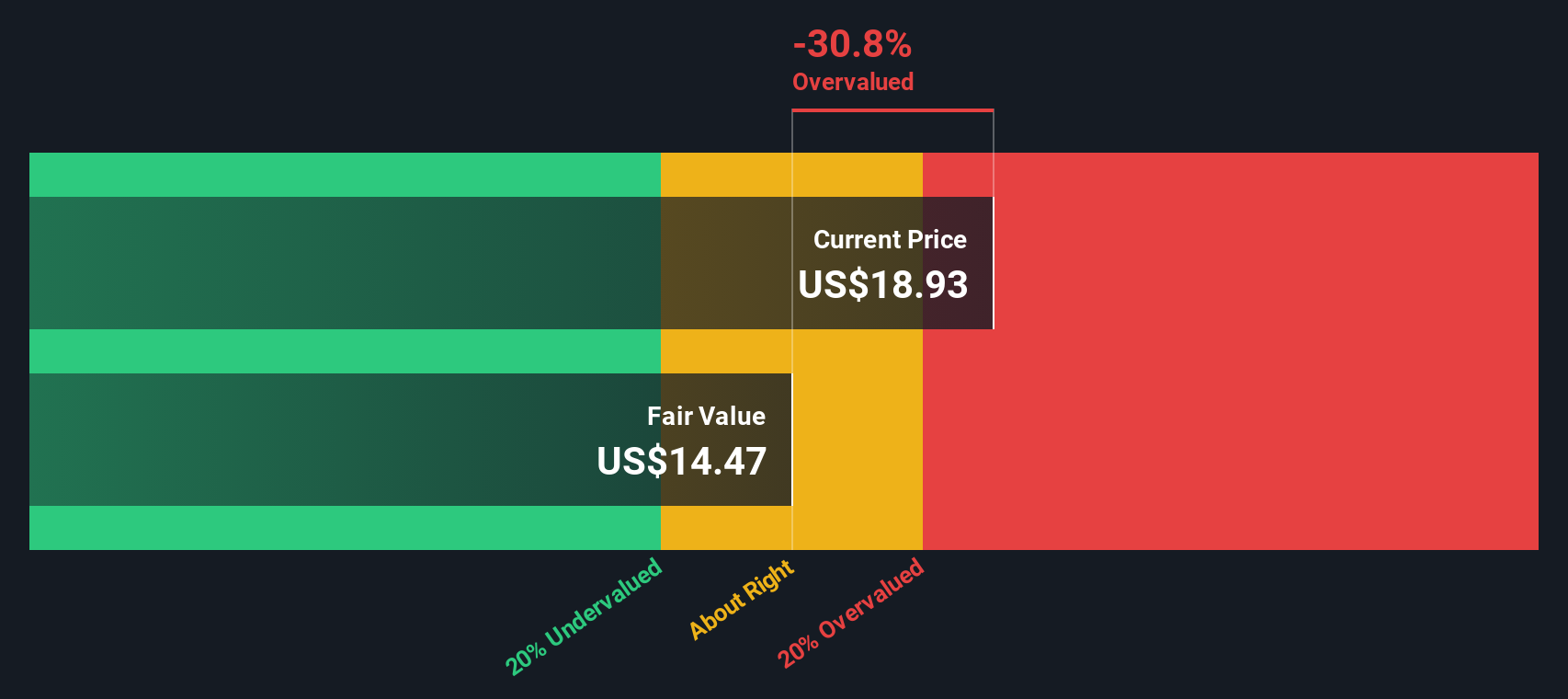

Exzeo Group (XZO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Exzeo Group operates in the insurance industry, focusing on property and casualty segments, with a market capitalization of $3.45 billion.

Operations: Exzeo Group's revenue is primarily derived from its Property & Casualty insurance segment, with recent figures showing $226.52 million. The company has experienced a notable shift in its financials, achieving a gross profit margin of 100% over the last six periods, reflecting efficient cost management.

PE: 15.4x

Exzeo Group, a dynamic player in the insurance tech sector, has caught attention with its recent inclusion in multiple Russell indexes, signaling potential growth. The company's earnings for Q1 2026 reached US$20.41 million, up from US$17.95 million last year. Its innovative WindForm Pro solution addresses new regulatory requirements in Florida, enhancing operational efficiency for insurers. Insider confidence is reflected through a share repurchase program of up to US$12 million announced recently.

Summing It All Up

- Click here to access our complete index of 73 Undervalued US Small Caps With Insider Buying.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.