3 U.S. Bank Stocks Built For Higher Interest Rates

First Merchants Corporation FRME | 0.00 |

The sharp drop in gold prices, a stronger U.S. dollar, and rising expectations for higher Federal Reserve interest rates are reshaping where money flows in the market. While some assets like precious metals face pressure, certain U.S. bank stocks could see their core lending and deposit businesses influenced by these shifts in rates and currency. This article examines how that backdrop connects to a curated U.S. Bank Stocks screener and highlights 3 stocks that appear positively exposed to the latest Fed driven news, helping you decide whether they deserve a closer look for your portfolio watchlist.

Heritage Financial (HFWA)

Overview: Heritage Financial is a regional bank based in Olympia, Washington, focused on serving small and medium sized businesses and their owners with a mix of commercial lending, real estate financing, consumer credit, and everyday deposit and digital banking services.

Operations: Heritage Financial generates about US$265.6m in revenue from commercial banking activities in the United States.

Market Cap: US$1.19b

Heritage Financial provides exposure to a higher rate backdrop through a loan-focused regional bank that already reports net profit margins of 27.3% and recent gains in net interest income and earnings per share. The situation has some tension, as rising nonaccrual and criticized loans, insider selling, and an unstable dividend record all require careful consideration of credit risk and capital discipline. At the same time, with analysts expecting faster earnings growth than the broader market and the stock trading below some intrinsic value estimates, the key question is whether current pricing already reflects those credit and competition risks or still underestimates Heritage Financial’s long-term earnings potential.

Heritage Financial’s lending engine, profit margins and analyst earnings expectations all point in one direction, but the real story sits in how those forecasts stack up against credit risk and capital pressure in the analyst forecasts for Heritage Financial

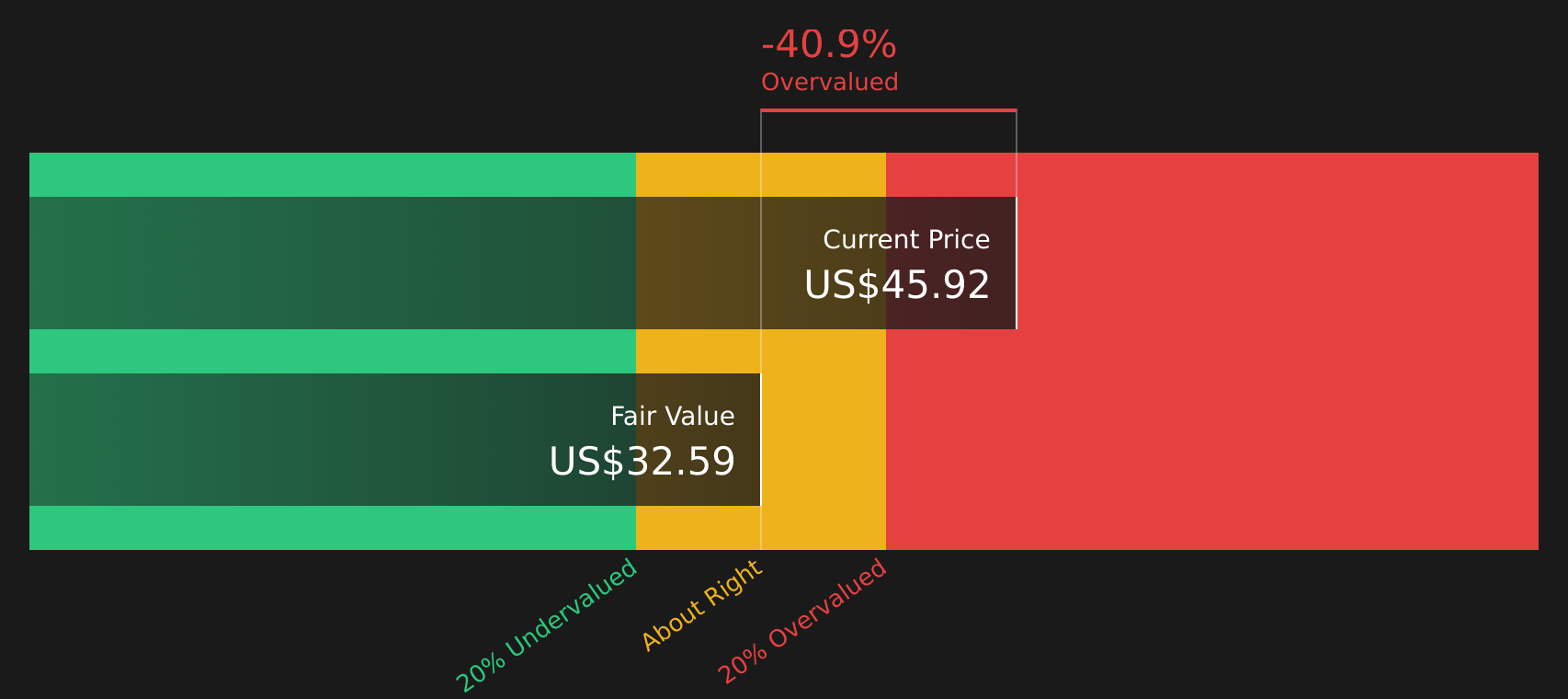

First Merchants (FRME)

Overview: First Merchants is a regional banking group headquartered in Muncie, Indiana, offering everyday banking, mortgages, business lending, and wealth management services to households and businesses across Indiana, Ohio, and Michigan through its branch network and digital channels.

Operations: First Merchants generates about US$637.8m in revenue from community banking services in the United States.

Market Cap: US$2.68b

First Merchants gives you exposure to a large regional lender that can be directly influenced by higher interest rates, with a substantial loan book that can benefit when net interest margins improve. Analysts expect earnings and revenue growth ahead of the broader U.S. market, while the stock trades below some estimates of its future cash flow value. At the same time, return on equity is relatively low at 7.4% and there has been meaningful insider selling, which calls for a closer look at capital allocation and growth quality. In addition, there is a growing dividend track record, a sizeable new share buyback and a multi billion dollar Community Benefits Agreement. The key question is whether the current price fairly reflects both the opportunity and the risks in First Merchants.

First Merchants sits at an interesting crossroads, with growth expectations, a large loan book, and fresh capital return plans that raise as many questions as they answer. The next step is to see how those pieces fit together in the analysis report for First Merchants

Peapack-Gladstone Financial (PGC)

Overview: Peapack-Gladstone Financial is a New Jersey based bank holding company for Peapack Private Bank & Trust, offering private banking, commercial lending, and wealth management services to businesses, non-profits, and affluent individuals through a mix of branch, private banking offices, and digital channels.

Operations: Peapack-Gladstone Financial generates about US$207.7m from its Banking segment and US$67.1m from Wealth Management, with all reported revenue coming from the United States.

Market Cap: US$810.1m

Peapack-Gladstone Financial may appeal to investors who want a mid-sized lender with meaningful fee based wealth management alongside interest income, which can be sensitive to wider lending spreads when rates rise. Recent results show higher net interest income and earnings per share, with margins improving. The P/E sits above the U.S. banks sector. The trade off is that return on equity remains modest and the stock is priced above some cash flow based estimates, so investors are paying for this profile. The company also has a long serving, mostly independent board and fresh preferred equity capital. The key question is whether current conditions and pricing fairly reflect the balance of potential and execution risk at Peapack-Gladstone Financial.

Peapack-Gladstone Financial’s mix of fee based wealth management and interest income can make its P/E look less straightforward. It is worth seeing what the market might be missing in the DCF valuation analysis for Peapack-Gladstone Financial

The three U.S. bank stocks covered here are only a starting point. The full U.S. Bank Stocks screener surfaces 43 more companies that share similar interest rate sensitivity and financial profile narratives. Identify and analyze the banks that best fit your preferred catalysts, risk profile, and investment timeframe by using Simply Wall St to filter for the specific earnings, capital, and valuation stories that matter most to you.

Take Control of Your Investment Journey

If Heritage Financial or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Alternative Stock Opportunities?

Fresh ideas can gain breakout momentum fast, and by the time everyone is talking, the best entry points might be gone. Scan new angles while it matters and consider acting early.

- Explore reliable income streams by reviewing a curated set of higher yielding companies through the 9 dividend fortresses.

- Look for early movers in disruptive computing by scanning the 29 quantum computing stocks while these potential opportunities are still less widely followed.

- Track next generation infrastructure developments by checking the 35 power grid technology and infrastructure stocks and see which companies are positioned around grid upgrade trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.