3 U.S. Financial Stocks Worth Watching Before Social Security Runs Dry

TowneBank TOWN | 0.00 |

Social Security’s trust fund is projected to run dry by 2032, and that kind of deadline can reshuffle risk across the U.S. financial sector. Higher government borrowing, pressure on Treasury markets, and shifting interest rates can all influence how banks, insurers, and lenders are priced and perceived. This article looks at what that backdrop could mean for investors and highlights 3 stocks from our U.S. Financial Sector Stocks screener that currently screen well on health, value, and growth potential. The goal is to help you judge whether these opportunities fit your own approach, or are ones to avoid.

FirstSun Capital Bancorp (FSUN)

Overview: FirstSun Capital Bancorp is a regional banking group headquartered in Denver that, through Sunflower Bank, provides a full range of commercial, consumer, and wealth management services to individuals and small and medium-sized businesses across Texas, Kansas, Colorado, New Mexico, Arizona, California, and Washington.

Operations: FirstSun generates the bulk of its approximately US$325 million in revenue from Banking activities, with around US$83 million from Mortgage Operations and a small Corporate loss, all earned in the United States where total reported revenue is about US$404 million.

Market Cap: US$1.8b

FirstSun Capital Bancorp offers exposure to regional banking with meaningful sensitivity to higher interest rates through core lending, along with a growing mix of fee income from wealth management and other services that can help support earnings if margins tighten. Forecast revenue and earnings growth are described as strong, yet the stock is reported to trade well below one estimate of fair value, and analysts reportedly see only modest near-term upside. This creates a tension between perceived long-term potential and current expectations. Recent charge-offs and substantial shareholder dilution highlight risks related to credit quality and capital decisions, and a relatively new board adds another factor for investors to monitor. For investors willing to assess whether the growth narrative justifies these trade-offs, FirstSun may warrant further research.

FirstSun’s mix of rate sensitive lending and fee income hints at a story investors may be underpricing, but the real twist shows up when you compare that narrative with the 3 key rewards and 1 important major warning sign

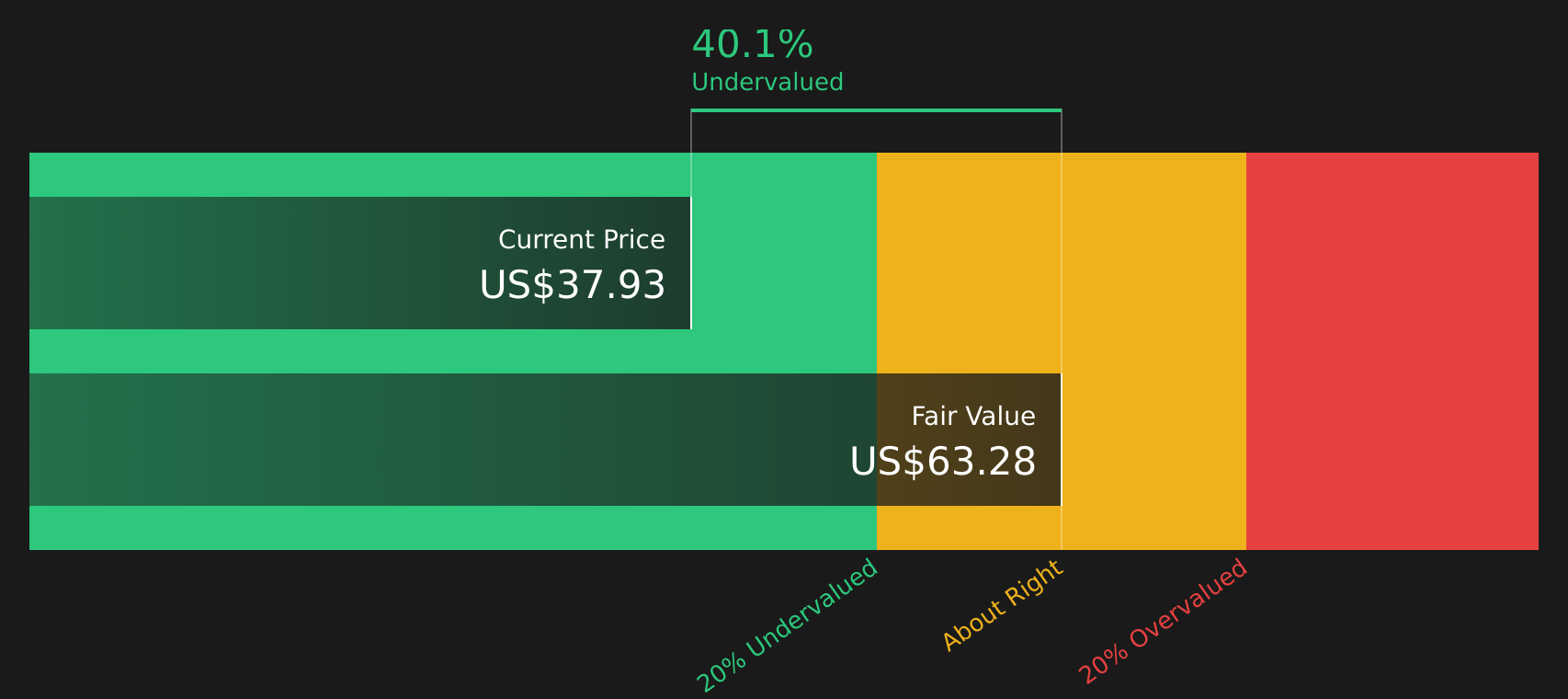

TowneBank (TOWN)

Overview: TowneBank is a community focused financial services company based in Portsmouth, Virginia, offering retail and commercial banking, mortgages, resort property management, and a broad suite of insurance and wealth planning services to individuals and businesses in the United States.

Operations: TowneBank generates about US$656.9 million of its revenue from Banking, with additional contributions of roughly US$102.9 million from Insurance, US$59.6 million from Resort Property Management, and US$57.7 million from Mortgage activities, all in the United States where total reported revenue is about US$877.2 million.

Market Cap: US$3.3b

TowneBank sits at an interesting crossroads for investors who expect higher interest rates to stick around, with its regional lending model directly tied to rate spreads and net interest income. Forecasts pointing to strong earnings growth and double digit revenue growth contrast with a recent period of earnings decline, a large one off loss, and shareholder dilution. This helps explain why the stock is described as trading well below one estimate of fair value even as its P/E is close to that fair range. Add in a roughly 3% dividend yield and a long tenured board, and this is a company where the gap between underlying franchise strength and messy reported numbers could matter a lot for patient investors.

Messy earnings and one off hits at TowneBank could be masking a stronger core bank and fee engine, so it is worth seeing how the story lines up in the analysis report for TowneBank

Radian Group (RDN)

Overview: Radian Group is a U.S. based mortgage insurer that helps lenders manage mortgage credit risk by providing private insurance and reinsurance on residential first lien home loans, primarily serving mortgage banks, commercial banks, credit unions, and other originators.

Operations: Radian Group generates about US$1.21b from Mortgage Insurance and a segment adjustment of roughly US$169.2m, with total revenue of around US$1.37b earned entirely in the United States.

Market Cap: US$5.1b

Radian Group stands out because its core mortgage insurance business is closely tied to U.S. housing demand, and current conditions of tight housing supply, strong millennial household formation, and tax deductibility for mortgage insurance premiums are supporting both portfolio stability and pricing power. Analysts expect earnings and revenue to keep growing, net margins are currently high, and management has been returning cash through dividends and sizeable buybacks. At the same time, reliance on mortgage insurance, uneven results in non core segments, and funding entirely through external borrowing keep risk on the table. To judge whether the balance of growth, valuation, and housing related risk really works in your favor, you will want to see what the rest of the Radian Group story looks like behind these headline numbers.

Radian Group’s high margins and housing tied engine look stronger than many investors assume, but the real story sits inside the analyst forecasts for Radian Group and what it signals about the next turn in mortgage risk.

The three stocks covered here are just a starting point. The full U.S. Financial Sector Stocks screener surfaces 33 more U.S. financial companies with balance sheets, valuations, and growth profiles that can support similarly compelling narratives. Use Simply Wall St to identify and analyze the catalysts that matter to you, so you can filter this broader set of banks, insurers, and lenders down to the highest conviction ideas for your watchlist.

Take Control of Your Investment Journey

If TowneBank or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Others Catch On?

Fresh stock ideas do not stay under the radar for long. As momentum builds and prices start moving quickly, late entries can end up chasing. Use these curated lists while they may still be relevant and consider acting promptly based on your own research.

- Identify companies quietly building strength before a potential breakout by scanning our hand picked group of resilient businesses in the 74 resilient stocks with low risk scores.

- Explore long term themes with companies involved in AI infrastructure, data centers, and networking upgrades surfaced through the curated 52 AI infrastructure stocks.

- Review a focused collection of companies in the 9 dividend fortresses for income-oriented ideas before yields change and valuations move away from levels you consider attractive.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.