3 U.S. Industrial Stocks Building Internal Talent Engines Investors Should Watch

Boise Cascade Co. BCC | 0.00 |

Private equity owners are pushing mid-market operators to prove that training actually improves field performance, not just compliance slide decks. That shift toward outcome focused, operationally embedded learning sits at the heart of the recent news driving this screener. For investors, the question is which mid-sized U.S. industrial and business services stocks are positioned to build real internal talent engines and which might struggle if expensive external learning platforms fall out of favor. This article walks through 3 stocks exposed to that news theme, all with potential upside from better aligned learning functions and internal manager development.

Tennant (TNC)

Overview: Tennant is a Minnesota based company that designs, manufactures, and services professional floor cleaning machines, including manual and autonomous equipment, detergents, parts, and repair services for commercial and industrial sites such as retailers, warehouses, schools, hospitals, and public venues worldwide.

Operations: Tennant generates about US$1.2b from designing, manufacturing, and selling products used in the maintenance of nonresidential surfaces, with reported regional disclosures across Asia Pacific, Europe, the Middle East, Africa, and segment level adjustments.

Market Cap: US$1.5b

Investors looking at Tennant get a company tightly linked to real world operations, where cleaning equipment uptime, labor efficiency, and on site management capability are critical. Its push into autonomous scrubbers and robotics, along with a growing focus on internal talent and an ERP overhaul, aligns closely with the shift toward outcome based learning and performance in field teams. At the same time, recent earnings pressure, thin 2.6% profit margins, higher debt reliance, and a P/E above sector averages mean execution on robotics, cost control, and manager development really matters. The picture is even more interesting when you weigh buybacks, new leadership in the COO role, and analyst expectations against these operational and balance sheet risks.

Tennant’s robotics push and thin 2.6% margins make execution the whole story, but the missing piece is how that trade off between growth projects, debt use, and buybacks really stacks up in the DCF valuation analysis for Tennant

Barrett Business Services (BBSI)

Overview: Barrett Business Services provides outsourced HR, payroll, workers compensation coverage, and staffing solutions to small and mid-sized U.S. companies, using a co employment model and consulting style support to help owners handle day to day people management and compliance.

Operations: Barrett Business Services generates about US$1.3b from staffing and outsourcing services across the United States.

Market Cap: US$830.9m

Investors focusing on mid market operators may pay attention to Barrett Business Services because it sits directly in the middle of rising demand for outsourced HR, compliance, and manager development, at the same time that private equity and business owners emphasize outcome based performance from their field teams. The company has been investing in internal training tools such as its BBSIU learning portal and a new performance management module, with the goal of keeping clients tied into a broader operating system rather than just transactional payroll. On the other hand, declining staffing demand, recent earnings pressure including a Q1 2026 loss, a tax court ruling, and reliance on higher risk external funding provide considerations that investors may weigh against analyst growth expectations and ongoing buybacks.

Barrett Business Services sits at the intersection of stalled staffing demand and an expanding HR operating system, yet many investors still treat it like a simple payroll contractor. To see how the full picture of growth potential, funding structure, and tax court overhang fits together, review the analysis report for Barrett Business Services

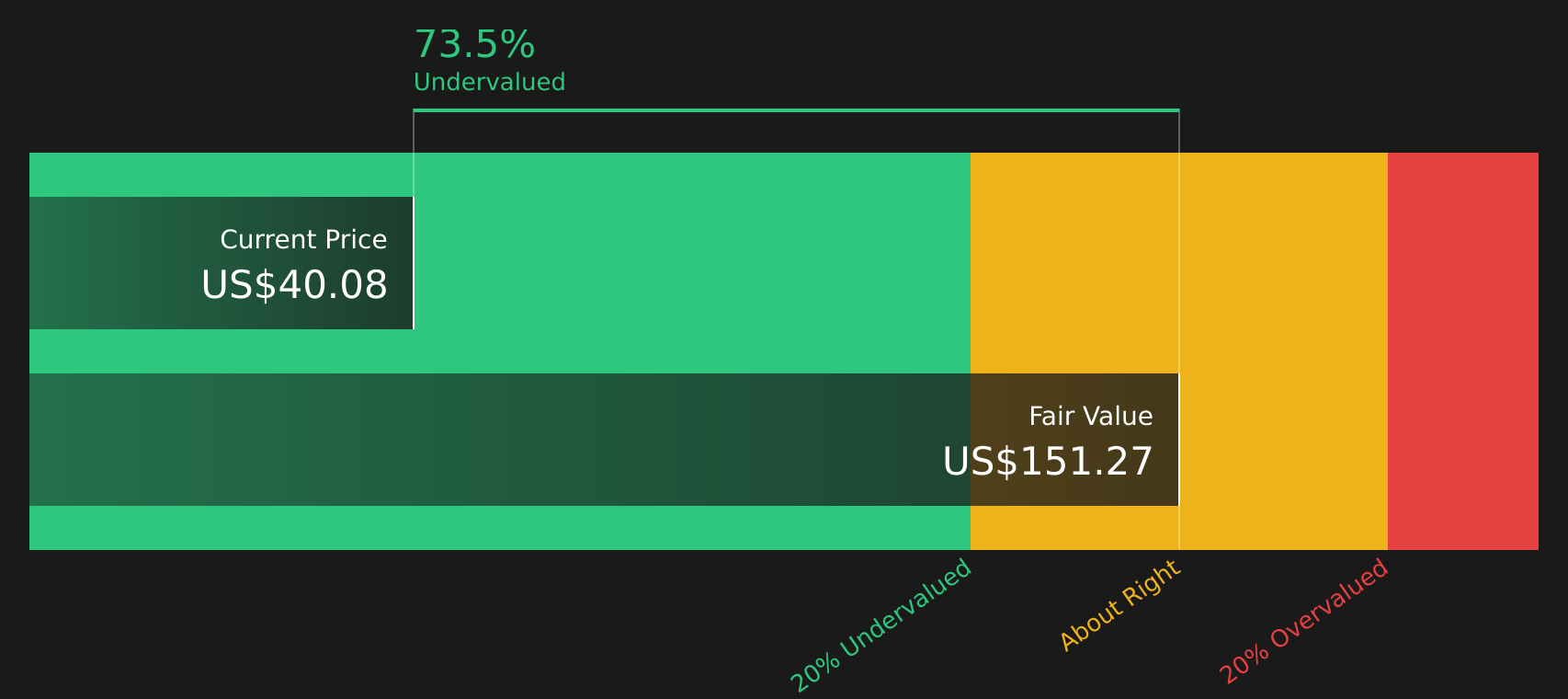

Boise Cascade (BCC)

Overview: Boise Cascade is a U.S. based manufacturer and distributor of engineered wood products, plywood, lumber, and a wide range of building materials that feed into residential construction, repair and remodeling, and light commercial projects across North America.

Operations: Boise Cascade generates about US$1.6b from its Wood Products segment and about US$5.9b from its Building Materials Distribution segment, with intersegment eliminations of roughly US$1.2b.

Market Cap: US$2.5b

Boise Cascade deserves attention if you are looking at how real operating improvement can turn a capital intensive business into a compounding story. The company is wrestling with soft demand, thinner 1.7% profit margins, and earnings that declined sharply in the most recent quarter, yet it is also modernizing mills, expanding distribution, and returning cash through regular dividends and meaningful buybacks. Forecast earnings growth of about 27% a year, combined with recognition as one of America’s Best Large Employers, points to a business investing heavily in both physical assets and its 7,500 strong workforce. The open question for investors is whether margin resilience, internal talent depth, and capital allocation can outweigh construction headwinds and pricing pressure in wood products.

Boise Cascade’s mills and distribution upgrades hint at an earnings story that many investors may be underestimating. The real twist shows up when you line that spending up against the analyst forecasts for Boise Cascade

The three stocks covered here are only a starting point, and the full screener surfaced 31 more mid-market industrial and business services companies with equally compelling narratives in the U.S. Mid-Market Industrial & Business Services Operators screener. Use Simply Wall St to identify and analyze the specific catalysts, capital allocation patterns, learning investments, and field execution traits that matter most to you, so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Tennant or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move first, and the strongest stories can be flying before most investors even notice. Scan these focused lists while the data still matters and get in early.

- Spot cash rich operators with room to run by scanning a curated list of solid balance sheet and fundamentals (48 results). This keeps you focused on resilient business models, not short lived hype.

- Ride potential income momentum by tracking a tight group of 7 dividend fortresses designed for investors who want yield and business strength working together, not just eye catching payout ratios.

- Follow structural growth trends by reviewing a focused pool of 49 AI infrastructure stocks built around companies supplying the hardware and backbone behind expanding AI adoption while it is still under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.