3 US Manufacturing Stocks With Balance Sheet And Funding Risk ուշադրություն

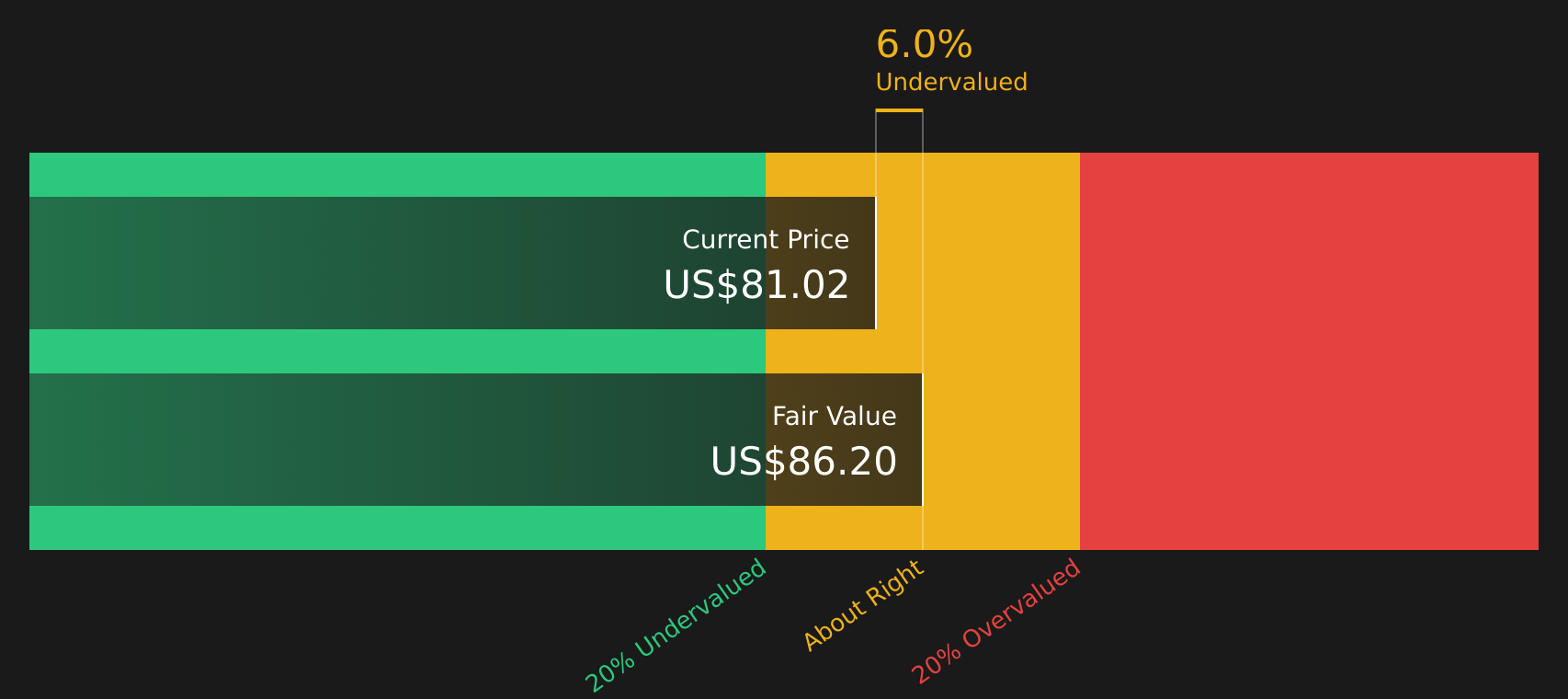

Legence Corp. Class A LGN | 0.00 |

U.S. manufacturing is expanding, reshoring projects are gathering pace, and business investment is taking center stage, even as inflation stays above the Fed’s 2% target and energy costs remain elevated. For investors, that mix can reward companies positioned to benefit from stronger domestic production and supply chain resilience, while pressuring others that are more sensitive to higher funding and input costs. This article looks at how the latest macro catalysts, from the Middle East ceasefire talks to firm U.S. factory data, connect to three U.S. Manufacturing and Industrial Reshoring screener stocks that appear positively exposed to the news flow.

LSI Industries (LYTS)

Overview: LSI Industries is a Cincinnati based manufacturer of commercial lighting, graphics, and display systems. It supplies non residential customers such as fuel stations, grocery chains, quick service restaurants, warehouses, and sports facilities with fixtures, digital signage, refrigerated displays, and related project services.

Operations: LSI Industries generates about US$282.4 million of revenue from Lighting and US$342.3 million from Display Solutions. Total revenue of roughly US$609.8 million comes from North America.

Market Cap: US$947.0 million

LSI Industries is notable in the reshoring story because it sits at the intersection of rising U.S. manufacturing and retail investment and the need for energy efficient lighting, digital signage, and refrigeration. The exclusive North American partnership with Carter Thermal for remote refrigeration broadens its role with grocery and retail chains. A growing mix of higher margin services and integrated solutions contributes to the case for stronger earnings quality over time. At the same time, higher debt from recent financing, reliance on external funding, and insider selling mean investors need to weigh balance sheet pressures and governance signals carefully. Overall, it is a company with clear exposure to capex driven demand, but also a capital structure and execution path that investors may want to understand in more detail.

LSI Industries sits where reshoring capex and energy efficient demand intersect, but the real story may be how its funding mix and services shift affect risk and reward, which the 3 key rewards and 3 important warning signs (1 is major!)

Legence (LGN)

Overview: Legence is a U.S. building services company that designs, installs, fabricates, and maintains complex HVAC and other mechanical, electrical, and plumbing systems for data centers, technology, healthcare, life sciences, education, and government facilities.

Operations: Legence generates about US$746.6 million from Engineering & Consulting and US$2.3 billion from Installation & Maintenance, with total revenue of roughly US$3.1 billion coming from the United States.

Market Cap: US$9.2 billion

Legence stands out in the reshoring theme because its engineering and fabrication work sits directly on the critical path of new data centers, semiconductor plants, and complex healthcare and education projects, all areas tied closely to U.S. industrial and infrastructure investment. A large backlog linked to these multi year projects, expansion of modular fabrication capacity, and recent rating and loan pricing improvements indicate that the balance sheet is being tuned to support growth, even as the business works through the impact of past impairments and one off items. With profitability still relatively early and governance and funding risks to weigh, the central question for investors is how this mix of high demand end markets and execution complexity ultimately affects Legence’s earnings quality and resilience.

Legence’s accelerating project pipeline across data centers and complex facilities raises a big question: how well is the balance sheet set up for what comes next, and what the Legence financial health report

Symal Group (ASX:SYL)

Overview: Symal Group is an Australian construction and infrastructure contractor that handles everything from civil works, bridges, utilities and community infrastructure to recycling, remediation and quarry materials. It often acts as both head contractor and specialist subcontractor across sectors like transport, power, renewables, defense and data centers.

Operations: Symal Group generates about A$801.4 million from Contracting Services, A$187.8 million from Plant & Equipment and a small loss from Other and Eliminations, with total revenue of roughly A$986.9 million earned in Australia.

Market Cap: A$736.6 million

Investors watching global reshoring and infrastructure spending may note Symal Group because its mix of civil construction, plant hire and recycling is closely linked to long-duration projects in renewables, data centers, defense and transport. Recent gains in profitability and high projected returns on equity indicate a focus on returns rather than volume alone. At the same time, reliance on external borrowing and a relatively new board and management team create execution and funding risks, even as a seasoned CFO is being brought in to tighten capital discipline. This combination of growth themes, balance sheet choices and leadership changes may significantly influence Symal’s overall risk and reward profile.

Symal Group’s mix of long duration projects and higher projected returns on equity hints at a story that many investors may be underestimating. The analyst forecasts for Symal Group could reveal what the headline numbers are not telling you yet.

The three stocks covered here are just a starting point, and the full U.S. Manufacturing and Industrial Reshoring screener turns up 10 more U.S. manufacturing and industrial reshoring companies with equally compelling stories that could fit different portfolio styles. Use Simply Wall St to identify the specific catalysts, analyze financial health, and filter for the narratives that matter most so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Symal Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh stock ideas can move from quiet to crowded quickly, as momentum builds and prices start flying before the crowd catches on. Check these curated lists now and get in early.

- Spot established income plays with sturdy payouts by scanning a curated group of 7 dividend fortresses before yields drop or attention shifts elsewhere.

- Track powerful structural themes in electricity, renewables and transmission by reviewing a hand picked 34 power grid technology and infrastructure stocks while many of these stories stay under the radar for now.

- Zero in on companies built for durability by using a filtered 66 resilient stocks with low risk scores so you are not caught chasing safety after prices already break out.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.