3 US Retail Stocks For Tariff Risk And Sourcing Resilience

National Vision Holdings, Inc. EYE | 0.00 |

Trade tensions are back in focus as new Section 301 tariffs of 10 to 12.5% on imports from 60 economies threaten to reshape costs for retailers that rely heavily on global supply chains. For investors, the question is which US retail stocks look better placed if these measures bite, and which could face more pressure as legal challenges grind through the courts. This article looks at three large, litigation resistant US retailers with diversified sourcing and resilient operations that appear relatively well positioned against tariff risk, and explains how their exposure to the new measures could matter for your portfolio decisions.

JD.com (JD)

Overview: JD.com is a Beijing based e-commerce and supply chain company that runs one of China’s largest online retail platforms, selling everything from electronics and groceries to healthcare products, while also offering logistics, online marketplace services, and technology driven supply chain solutions for third parties in China and parts of Europe.

Operations: JD.com generates most of its CN¥1.32t revenue from JD Retail (about CN¥1.13t), with additional contributions from JD Logistics (around CN¥231b) and New Businesses (roughly CN¥50b), primarily in the People’s Republic of China.

Market Cap: US$37.2b

JD.com attracts attention as a large scale Chinese retailer with its own logistics network, and a business mix that spans electronics, daily necessities, and online services. Analysts currently see the stock trading below their consensus price target and below an estimated future cash flow value. A P/E that sits under peer averages is sometimes interpreted as hinting at expectations that may be conservative if margins recover from the recent decline. At the same time, investors need to weigh competition, rising costs, and geopolitical and tariff risks that could pressure profitability, especially as JD.com expands internationally and contests around global trade rules sharpen.

JD.com’s low P/E and scale in China suggest that expectations may be too muted, especially if margins stabilize. Get the full story in the 3 key rewards and 1 important warning sign

Pattern Group (PTRN)

Overview: Pattern Group is a Lehi, Utah based e-commerce accelerator that uses proprietary technology and on demand expertise to help consumer brands sell more effectively across major online marketplaces in categories such as health and wellness, beauty, home, pet, sports, and electronics.

Operations: Pattern Group generates about US$2.73b in revenue from online retailers, with roughly US$2.42b from the United States and US$311m from international markets.

Market Cap: US$3.78b

Investors looking at tariff sensitive retailers may find Pattern Group interesting because it operates primarily as a US based e-commerce platform, yet still gives exposure to global brand growth. The company sits at the intersection of AI driven commerce and marketplace expansion, with tools like Pattern Intelligence (Pi) and a large data set aimed at improving pricing and advertising outcomes for brand partners. Analysts have highlighted potential earnings growth and have described the stock as trading below some estimated value measures. However, investors still need to watch funding risk, current unprofitability on some metrics, and high executive pay. The full picture of how those trade offs balance out is where the real opportunity, or caution, lies.

Pattern Group’s accelerating e-commerce engine and data tools could mean the real story is hiding in plain sight, with valuation and execution pulling in different directions. Weigh the full Pattern Group setup in the analysis report for Pattern Group

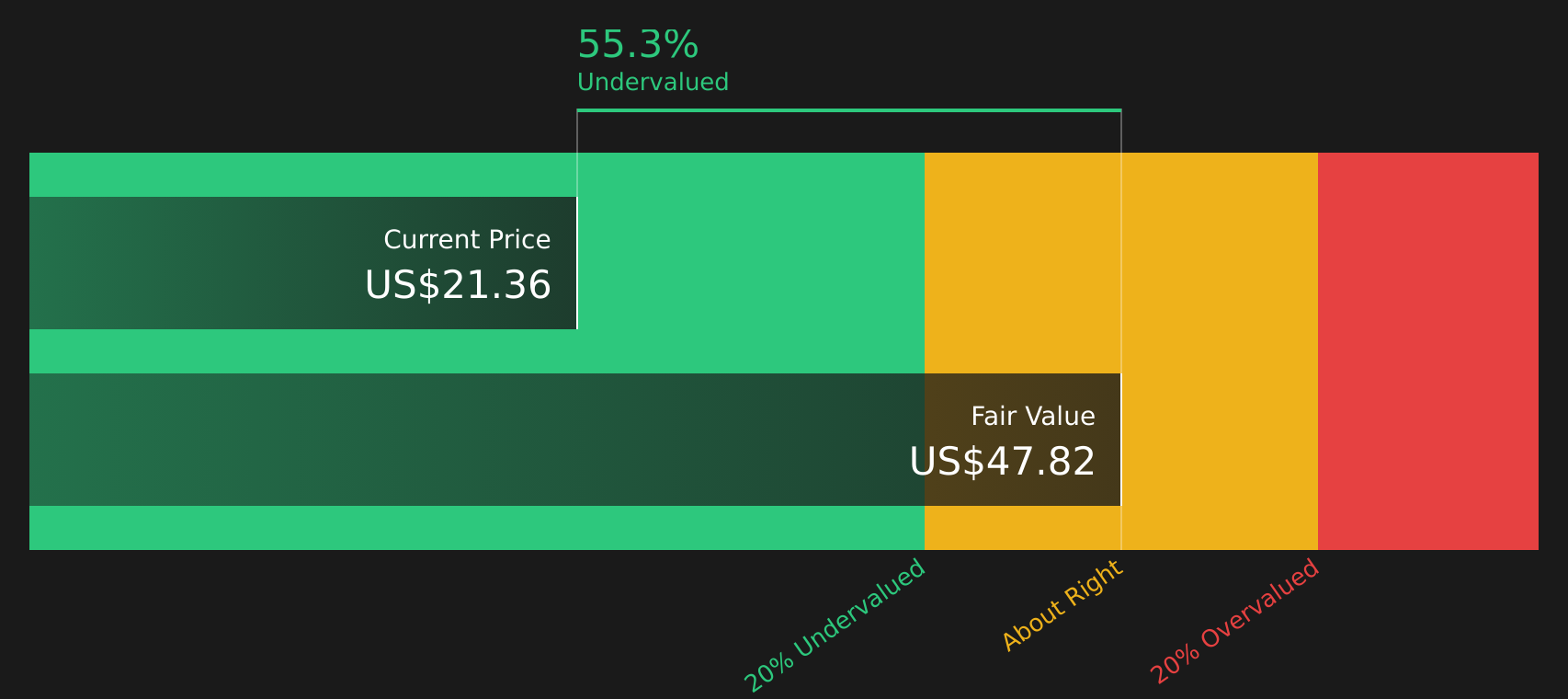

National Vision Holdings (EYE)

Overview: National Vision Holdings is a US based optical retailer that provides eye exams, eyeglasses, contact lenses, and accessories through banners such as America's Best, Eyeglass World, Vista Optical, and DiscountContacts.com, serving value focused and style conscious customers as well as those using vision benefits and managed care plans.

Operations: National Vision Holdings generates about US$2.0b in revenue mainly from its Owned & Host segment (US$2.0b), with a small contribution from Corporate/Other and a modest unallocated adjustment for unearned and deferred revenue.

Market Cap: US$1.34b

National Vision Holdings stands out in this tariff heavy backdrop because it earns its money in US optical retail, yet has already been working to spread sourcing across countries. Management has said recent tariffs are now a fractional cost that can be offset with pricing and efficiency moves. The company is benefiting from higher value eyewear assortments, growth in managed care customers, and expanding roles such as becoming the sole eye care provider on all US Army and Air Force bases. However, it still carries a higher P/E and a funding mix fully reliant on external capital. For investors, the tension between improving profitability, tariff resilience, and that higher risk profile is where the key considerations lie.

National Vision Holdings looks like a retailer where higher value eyewear, managed care traffic, and that US Army and Air Force contract could be masking a very different future than its current P/E suggests. It is worth seeing how the analyst forecasts for National Vision Holdings fits with its tariff story before the next twist appears.

The three stocks covered here are a useful starting point, but the full screen of litigation resistant US retailers surfaced 9 more companies with equally compelling narratives that could round out your watchlist in different ways. It is worth seeing what else shows up in the Litigation-Resistant US Retailers screener. Use Simply Wall St to identify and analyze the precise catalysts, tariff exposure, and business drivers that matter to you so you can focus on the highest conviction retail opportunities rather than sorting through the entire market alone.

Take Control of Your Investment Journey

If National Vision Holdings or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly

Fresh stock ideas can move from under the radar to full momentum quickly, and the best entry points rarely last. Scan these curated themes before the crowd and consider them promptly.

- Target reliable portfolio anchors by reviewing a curated group of income focused compounders inside the 8 dividend fortresses while yields and payout strength still look compelling.

- Spot tomorrow's infrastructure candidates by scanning the curated 34 power grid technology and infrastructure stocks before grid upgrades and electrification trends are fully reflected in prices.

- Evaluate the next wave of automation by assessing the hand picked companies in the 31 robotics and automation stocks while adoption and productivity gains are still being treated as optional.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.