3 US Textile Stocks Investors Are Watching As China Apparel Tariffs Hold

Kontoor Brands, Inc. KTB | 0.00 |

The latest US China trade thaw has a clear gap: textiles and apparel remain under the same US tariffs on Chinese goods through 2027, while sectors like agriculture and large manufacturers take center stage for relief. With Chinese apparel shipments to the US down 51% in Q1 2026, some US based textile and apparel manufacturers sit in the middle of this policy divide. This article walks through 3 stocks exposed to this news, explains why the tariff backdrop matters to their businesses, and outlines the risk and reward profile you might see if you choose to research them further.

Unifi (UFI)

Overview: Unifi is a Greensboro based manufacturer of synthetic and recycled polyester and nylon yarns, supplying brands and fabric makers for apparel, hosiery, automotive, home furnishings, industrial and medical uses, with a focus on its REPREVE recycled fiber products.

Operations: Unifi generates about US$325.8 million of revenue from the Americas, US$110.0 million from Brazil and US$89.8 million from Asia, with US$287.0 million of sales in the United States, US$110.0 million in Brazil, US$87.9 million in China and US$40.7 million across other countries.

Market Cap: US$89.2 million

Unifi sits at the intersection of two factors: tariffs that favor US based textile production, and demand for recycled materials. The stock is priced at a discount to one estimate of fair value and trades on a low P/S ratio. The business remains loss making and has relied on external borrowing, so funding risk and weak recent earnings, including a reported net loss of US$23.37 million for the first nine months of 2026, are important for you to weigh. Management has highlighted brand interest in Central America and Asia as supply chains adjust to tariffs, which could reshape Unifi’s customer demand in a way the market may not be fully focused on yet.

Tariff tailwinds and recycled demand might be masking the real story at Unifi, so walk through the DCF valuation analysis for Unifi to see how its loss making profile and funding needs change the picture right at the end.

Jerash Holdings (US) (JRSH)

Overview: Jerash Holdings (US) is a Jordan based apparel manufacturer that produces customized sportswear and outerwear, including t shirts, jackets, vests, pants, shorts, polo shirts and personal protective equipment for global brands and retailers across the United States, Europe and Asia.

Operations: Jerash Holdings (US) generates about US$166.3 million of revenue from apparel, with roughly US$138.2 million coming from customers in the United States and the rest spread across China including Hong Kong, the Republic of Korea, Jordan and other markets.

Market Cap: US$56.6 million

Jerash Holdings (US) sits in the crosscurrents of tariff realignment, with production in Jordan that benefits from lower duties into the US and EU at a time when Chinese apparel imports to the US are under pressure. The company has reported US$166.26 million of sales and US$3.54 million of net income for FY 2026 and also pays a regular dividend, which may appeal if you want income as well as exposure to this segment of the apparel industry. At the same time, the dividend is not fully backed by free cash flow and the business relies on external borrowing, so funding and working capital management are important considerations. Investors may also want to consider how the company’s tariff position, order pipeline and capacity build out might be affected if trade rules or demand were to shift again.

Jerash Holdings (US) sits where tariff advantages, US customer concentration and a cash dividend intersect, but the real story only comes into focus in the 4 key rewards and 1 important warning sign and what that balance could mean next

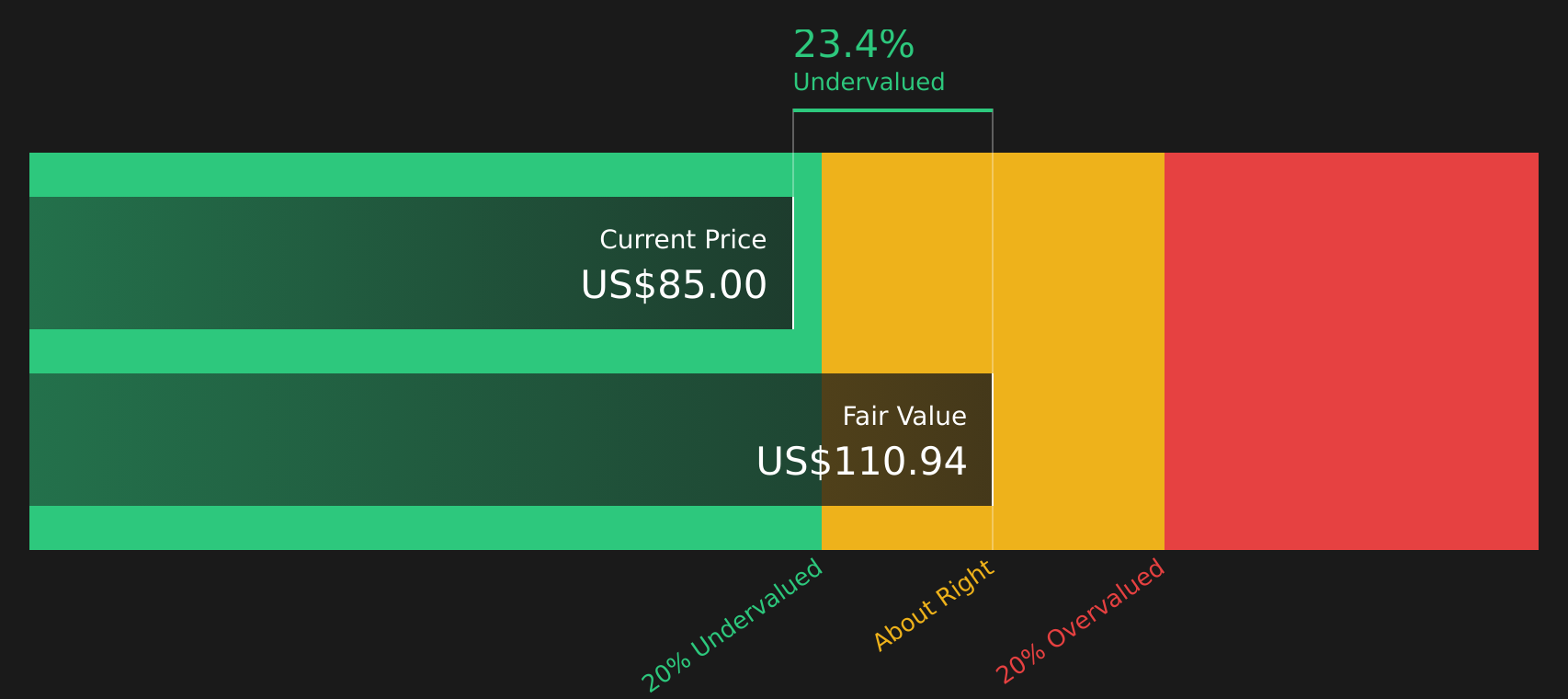

Kontoor Brands (KTB)

Overview: Kontoor Brands is a Greensboro based apparel company behind Wrangler, Lee and Helly Hansen, designing and selling denim, lifestyle apparel, footwear and accessories through retailers, workwear channels and its own direct to consumer and online operations across the Americas, EMEA and Asia Pacific.

Operations: Kontoor Brands generates about US$1.93b of revenue from Wrangler, US$37.0m from Other activities and reports a US$1.38b segment adjustment. Total sales are roughly US$3.34b, split between about US$2.33b from the United States and US$1.01b from international markets.

Market Cap: US$4.63b

Kontoor Brands offers a mix of well known Western denim labels, tariff protected US sourcing and an increasingly important Helly Hansen outdoor business. The stock trades below some estimates of fair value and below many peers on common valuation measures. The company is working through higher tariff costs, a large one off loss and a high debt load. Analysts expect changes in earnings and return on equity, with Lee divestiture proceeds and a sizeable buyback program among the factors they monitor. If you think tariff pressure on Chinese apparel and Kontoor’s supply chain shifts could affect how the market views this earnings and cash flow profile, there is more to unpack in the detailed work on risks, rewards and value.

Kontoor Brands looks like a classic valuation outlier, with tariffs, debt and a large one off loss pulling the story in different directions, while the 4 key rewards and 4 important warning signs could reveal the real hinge for where sentiment goes next.

If these three stocks have sparked ideas, they are only a slice of the opportunity set, with the full US-based Textile and Apparel Manufacturers screener surfacing 13 more companies with equally compelling tariff and reshoring narratives. Use Simply Wall St to analyze these businesses side by side, filter for the specific catalysts and narratives that matter to you, and identify the highest conviction plays in this corner of the market.

Take Control of Your Investment Journey

If Unifi or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh ideas do not stay under the radar for long. Strong stories gain momentum, weak ones get caught dropping, and pricing windows close fast, so getting in early can help investors access opportunities while they are still developing.

- Spot companies quietly building momentum before they start flying by scanning the 43 high quality undervalued stocks curated to highlight quality with support from cash flows and balance sheets.

- Hunt for cash generative growth where hype has not fully caught up by using the 62 profitable AI stocks that aren't just burning cash to surface focused, revenue producing AI stocks.

- Zero in on resilient balance sheets that can handle shocks with the list of solid balance sheet and fundamentals (46 results) and filter for businesses where fundamentals still drive the story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.