A Fresh Look at Western Digital (WDC) Valuation as Shares Extend Their Recent Climb

Western Digital Corporation WDC | 343.43 | +1.64% |

If you have Western Digital (WDC) on your watchlist, recent price movements might have sparked a few questions. The stock has continued a run that has caught the eye of value-seeking investors, especially as the company’s core business in data storage continues to evolve. While there hasn't been a major headline event, the steady climb over the past month has some wondering if this is simply more of the same or an early signal of something bigger ahead.

Taking a step back, Western Digital’s shares have had a strong year by any measure, more than doubling over the past 12 months. In the past month alone, the stock is up 30%, and over the past 3 months, it has gained 69%. That momentum sets Western Digital apart from many in the tech hardware space, especially after the company posted year-on-year revenue and net income growth. In context, the broader tech sector has seen its share of volatility, but Western Digital’s performance suggests growing confidence from investors in the company’s turnaround story.

With Western Digital’s sharp rise this year, many are asking if there is real value left for new investors or if the market has already factored in the company’s growth potential.

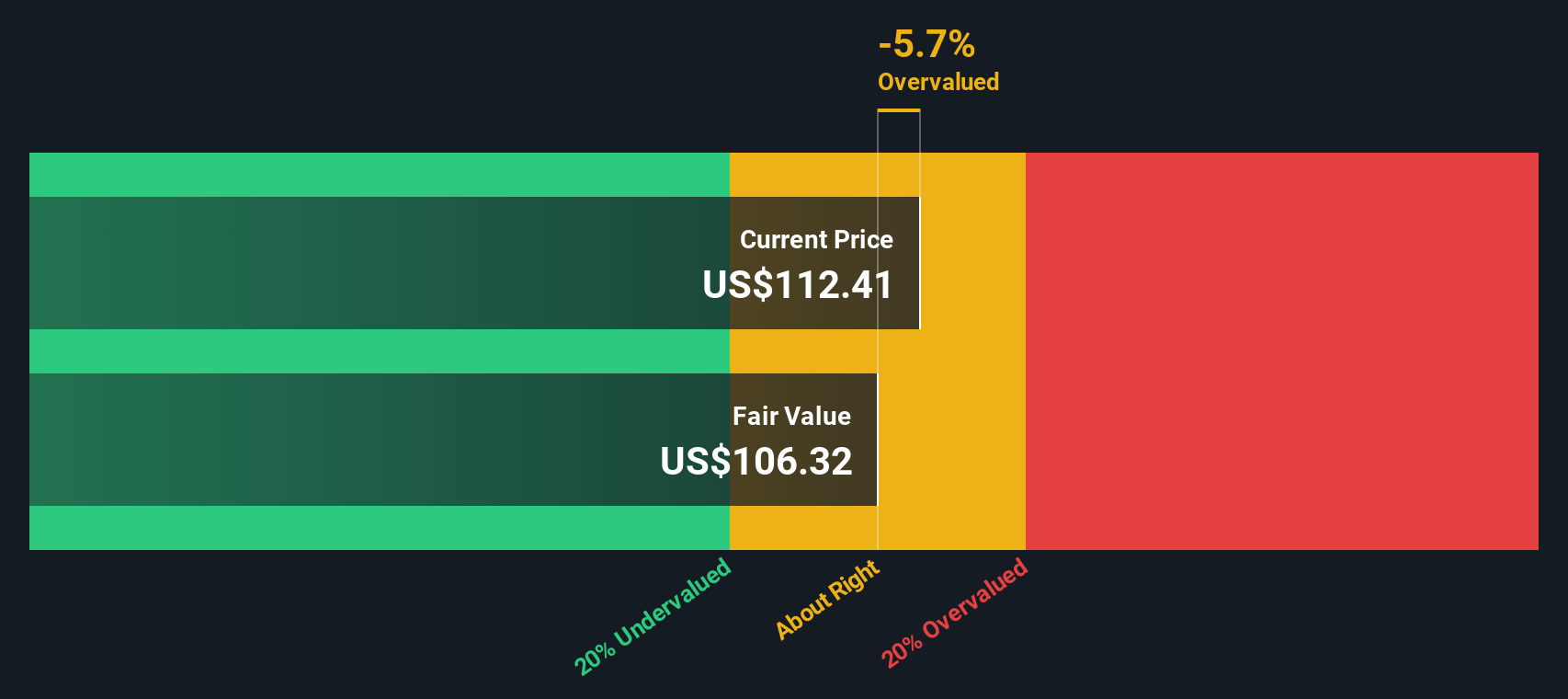

Most Popular Narrative: 9% Overvalued

Western Digital is currently considered overvalued by the most widely followed narrative, with analysts citing strong demand and rising price targets, but also noting that the current share price sits above fair value estimates.

• Bullish analysts cite sharply improving demand for both NAND and hard disk drives, primarily driven by artificial intelligence, cloud storage expansion, and overall data growth. Lead times for high-capacity drives have extended significantly and industry supply remains tight, even with increased output.

Some may think Western Digital’s valuation story is all about past momentum, but this narrative focuses on explosive growth assumptions and a bold future profit forecast. The outlook is closely tied to major demand shifts resulting from advancements in technology. The premium fair value is being driven by forecasted metrics, with several noteworthy numbers setting a high bar for Western Digital.

Result: Fair Value of $97.91 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, heavy reliance on a few major cloud customers and potential disruptions from emerging storage technologies could quickly challenge Western Digital’s bullish outlook.

Find out about the key risks to this Western Digital narrative.Another View: What Do the Numbers Say?

Looking at the company through our DCF model paints a similar picture, suggesting Western Digital is trading just above its estimated fair value. This method digs deeper into cash flow expectations rather than market hype. But does that make it more reliable?

Build Your Own Western Digital Narrative

If you see things differently or want to explore your own perspective, it takes just a few minutes to dive into the numbers and shape your own story. Do it your way

A great starting point for your Western Digital research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t limit yourself to just one stock when new opportunities are only a click away. The right idea now could set up your next win.

- Unlock rapid growth by exploring the AI penny stocks shaping tomorrow’s technology landscape through powerful breakthroughs in artificial intelligence and automation.

- Strengthen your passive income and financial stability through dividend stocks with yields > 3% that offer attractive yields and a history of rewarding shareholders.

- Position yourself ahead of the curve by considering quantum computing stocks at the forefront of quantum innovation and next-level computing potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.