A Look At ADTRAN Holdings (ADTN) Valuation After Wi‑Fi 7 Expansion And Improved Quarterly Results

ADTRAN Holdings, Inc. ADTN | 0.00 |

ADTRAN Holdings (ADTN) has drawn fresh attention after expanding its SDG 8700 Series with new Wi-Fi 7 platforms and reporting first quarter 2026 results that showed higher revenue and a smaller net loss than a year earlier.

The Wi-Fi 7 expansion and improved first quarter results have come alongside a 90-day share price return of 47.19% and a year-to-date share price return of 71.77%. The 1-year total shareholder return of 83.39% contrasts with a 5-year total shareholder return that is down 19.50%, suggesting recent momentum has picked up after a weaker longer-term experience.

If this kind of rebound has your attention, it could be a useful moment to broaden your search and check out 19 top founder-led companies

With the stock up strongly over the past year but still trading below some analyst targets, and with the company reporting a loss, you have to ask yourself: is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 24% Undervalued

ADTRAN Holdings' most followed valuation narrative sets a fair value of $19.50 per share versus a last close of $14.91. This frames the recent rebound in a very different light.

Expanding global demand for high-speed broadband, particularly residential fiber upgrades and multi-gigabit services, is fueling strong customer wins and backlog growth across both North America and Europe, supporting continued revenue acceleration over the coming quarters. Rising infrastructure investment for AI computing, cloud, and 5G densification is driving higher demand for ADTRAN's optical networking solutions and cross-selling opportunities, which should boost both revenue and market share as these trends intensify.

Curious how a loss-making company still lands on a higher fair value? The narrative leans heavily on revenue expansion, margin repair and a future earnings profile that assumes a much richer valuation multiple than today.

Result: Fair Value of $19.50 (UNDERVALUED)

However, this upbeat narrative still leans on revenue growth and margin improvement, and currency swings between the U.S. dollar and euro could easily upset those expectations.

Another Way to Look at It

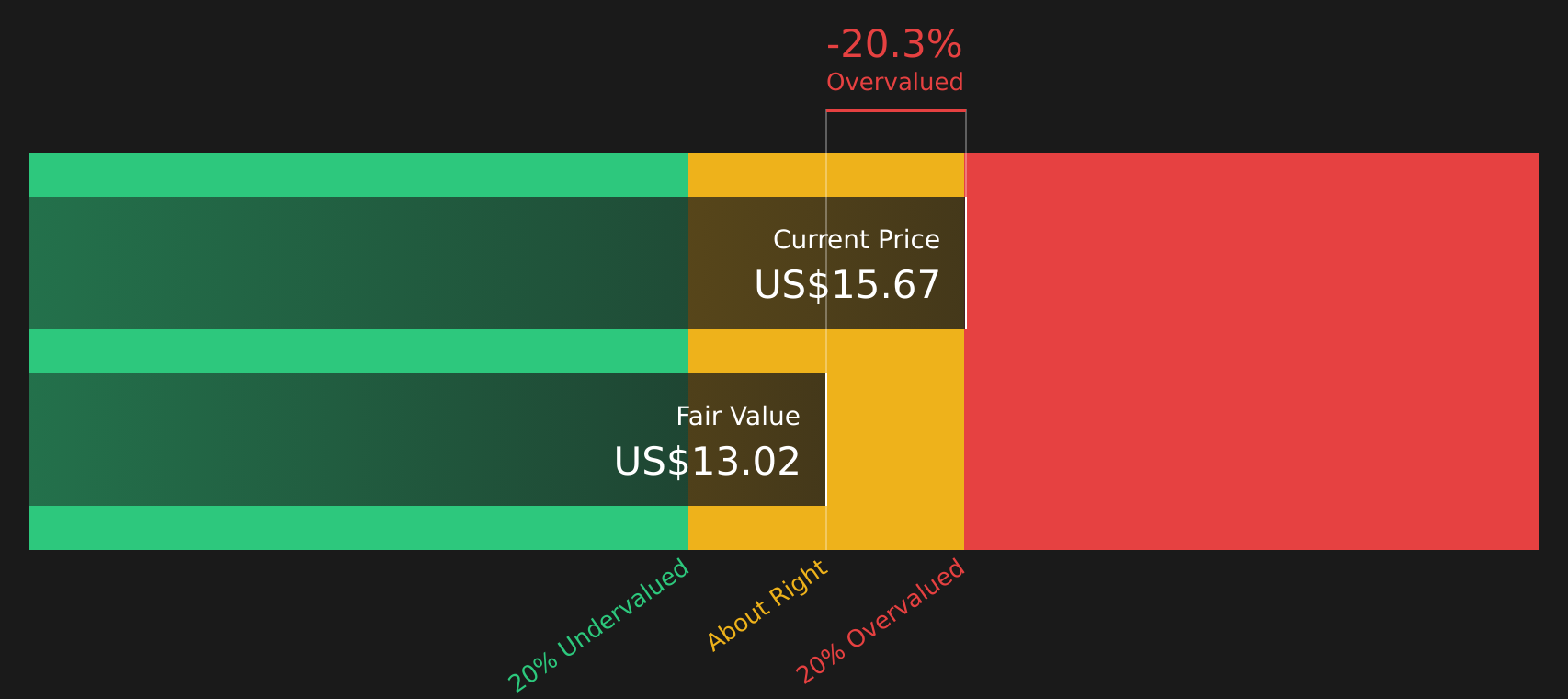

There is a catch. Simply Wall St's DCF model points to a fair value of about $13.04 per share, which is below the current $14.91 price and implies ADTRAN is overvalued on that cash flow view. So which story do you think is closer to reality: cash flows or narratives?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ADTRAN Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution feels familiar, use it as a prompt to move quickly and review the numbers yourself using 3 key rewards

Ready for more investment ideas?

If ADTRAN has sharpened your focus, do not stop here. Use this momentum to uncover other stocks that could fit neatly alongside or even compete with it.

- Target potential mispricings by scanning for quality stocks that look cheap on fundamentals with the 51 high quality undervalued stocks.

- Prioritise stability by checking companies with robust finances and steady metrics using the solid balance sheet and fundamentals stocks screener (45 results).

- Get ahead of the crowd by reviewing the screener containing 21 high quality undiscovered gems before others start paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.