A Look At Agree Realty (ADC) Valuation After Raised 2026 Investment Guidance And Dividend Increase

Agree Realty Corporation ADC | 0.00 |

Agree Realty (ADC) shares are reacting to fresh guidance after the company lifted its 2026 investment outlook following record 2025 deployment, higher adjusted funds from operations per share, and an increased annual dividend.

The updated guidance comes alongside steady share price gains, with a 1-day share price return of 1.96%, a 30-day share price return of 6.68%, and a year-to-date share price return of 8.26%. Over the longer term, total shareholder returns of 14.70% over 1 year and 52.69% over 5 years reflect momentum that has built gradually as the REIT has continued to execute on its net lease strategy and dividend growth.

If this earnings update has you thinking about where else capital might work hard, it could be worth scanning our list of 25 power grid technology and infrastructure stocks tied to long term infrastructure themes.

With ADC trading at $78.08 and sitting only slightly below the average analyst target of $81.86, plus an internal estimate suggesting a larger intrinsic discount, the key question is whether this recent strength still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 4.6% Undervalued

Agree Realty's most followed narrative sets a fair value of $81.88 per share, sitting modestly above the recent $78.08 close and presenting a measured upside case.

The durability of essential retail categories (grocery, pharmacy, home improvement, auto parts) is translating into high-quality, e-commerce-resistant tenant composition, supporting rent stability and protecting net margins against shifts in consumer behavior or economic cycles.

Curious what kind of revenue ramp, margin shape, and future earnings power are reflected in that fair value, and how the required valuation multiple compares? The narrative connects those elements in a way the current share price alone does not convey.

Result: Fair Value of $81.88 (UNDERVALUED)

However, these assumptions can be tested quickly if aggressive acquisition funding leads to meaningful dilution or if key national tenants consolidate and reduce store counts.

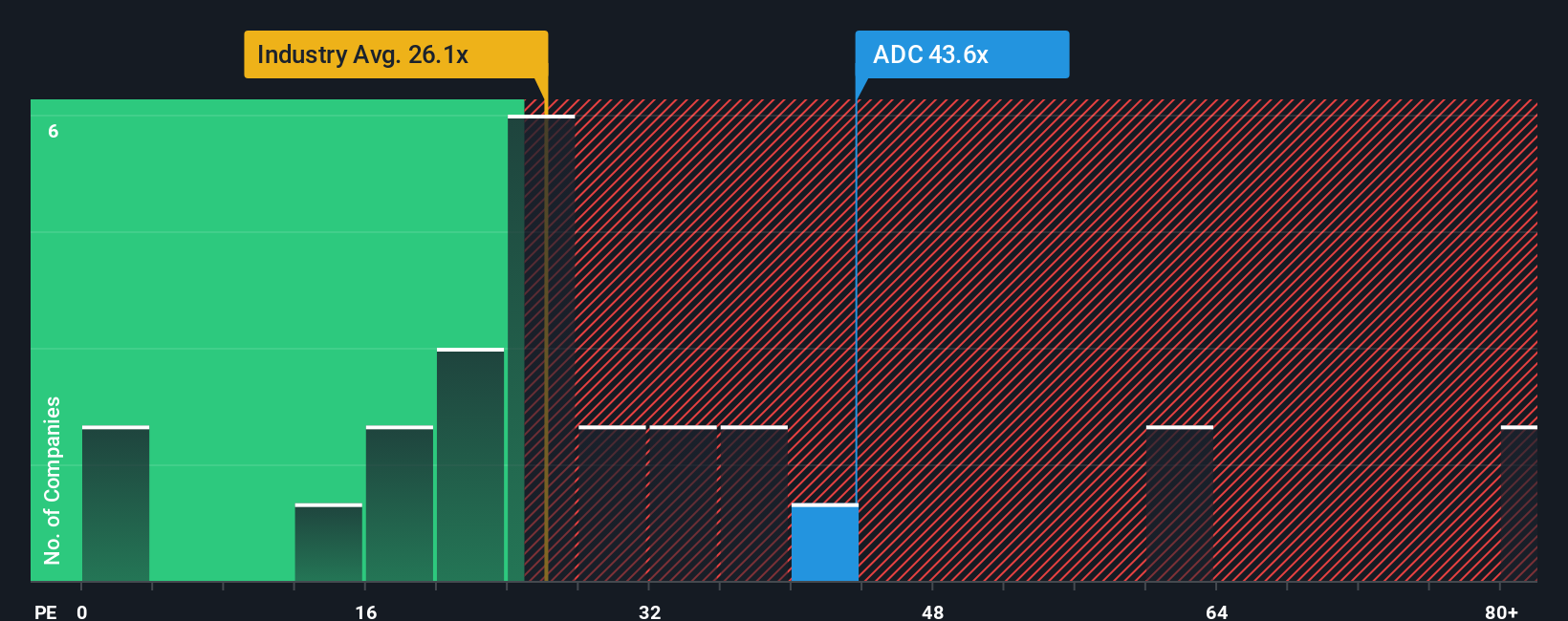

Another View: High P/E Puts The Brakes On

While the narrative and our fair value estimate suggest upside, the current P/E of 47.6x tells a different story. It sits well above the US Retail REITs industry at 28x, peers at 23.6x, and even the fair ratio of 35.3x, which points to valuation risk if sentiment cools.

That kind of gap can close in more than one way. The key question for you is whether future earnings can grow fast enough to justify this premium or if the share price eventually does the heavy lifting instead.

Build Your Own Agree Realty Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can create your own view in minutes with Do it your way.

A great starting point for your Agree Realty research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing your next move after reviewing Agree Realty, do not stop here. A broader watchlist can help you spot opportunities you might otherwise miss.

- Target reliable cash flow by scanning 13 dividend fortresses that focus on income first and may suit a portfolio built around regular payouts.

- Hunt for mispriced quality with our screener containing 24 high quality undiscovered gems that surface companies with strong fundamentals the market may be overlooking.

- Prioritise resilience with the 83 resilient stocks with low risk scores to focus on businesses that score well on stability and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.