A Look At Allison Transmission (ALSN) Valuation As Analysts See Shares 9.4% Over Fair Value

Allison Transmission Holdings, Inc. ALSN | 117.06 | -1.50% |

Allison Transmission Holdings (ALSN) has drawn fresh attention after recent share price moves, with the stock showing mixed short term returns but stronger gains over the past 3 months and year to date.

While the latest 1 day and 7 day share price returns have been slightly negative, the 30 day share price return of 8.7% and 90 day share price return of 32.35% suggest momentum has been building. This has been supported by longer term total shareholder returns of 157% over 3 years and 192.02% over 5 years from a current share price of US$109.57, despite a 7.32% total shareholder return decline over the past year.

If Allison Transmission’s recent move has you thinking about other opportunities in the auto space, this could be a good moment to check out auto manufacturers.

With Allison Transmission trading at US$109.57, sitting only modestly below an average analyst price target of US$114.80 but with some models pointing to a larger intrinsic discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 9.4% Overvalued

Compared with Allison Transmission’s last close at $109.57, the most followed narrative points to a fair value of $100.20, creating a valuation gap that is hard to ignore.

The analysts have a consensus price target of $104.889 for Allison Transmission Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $129.0, and the most bearish reporting a price target of just $84.0.

Curious what earnings path and margin profile sit behind that $100.20 fair value and tight price target range? The narrative leans on specific long term revenue growth, profitability and valuation multiple assumptions. The tension between expected growth and a relatively low implied P/E is where the story gets interesting.

Result: Fair Value of $100.20 (OVERVALUED)

However, there are still clear risks here, including faster adoption of fully electric drivetrains and any stumble in integrating the Dana Off Highway acquisition that could challenge this thesis.

Another View: Multiples Tell a Different Story

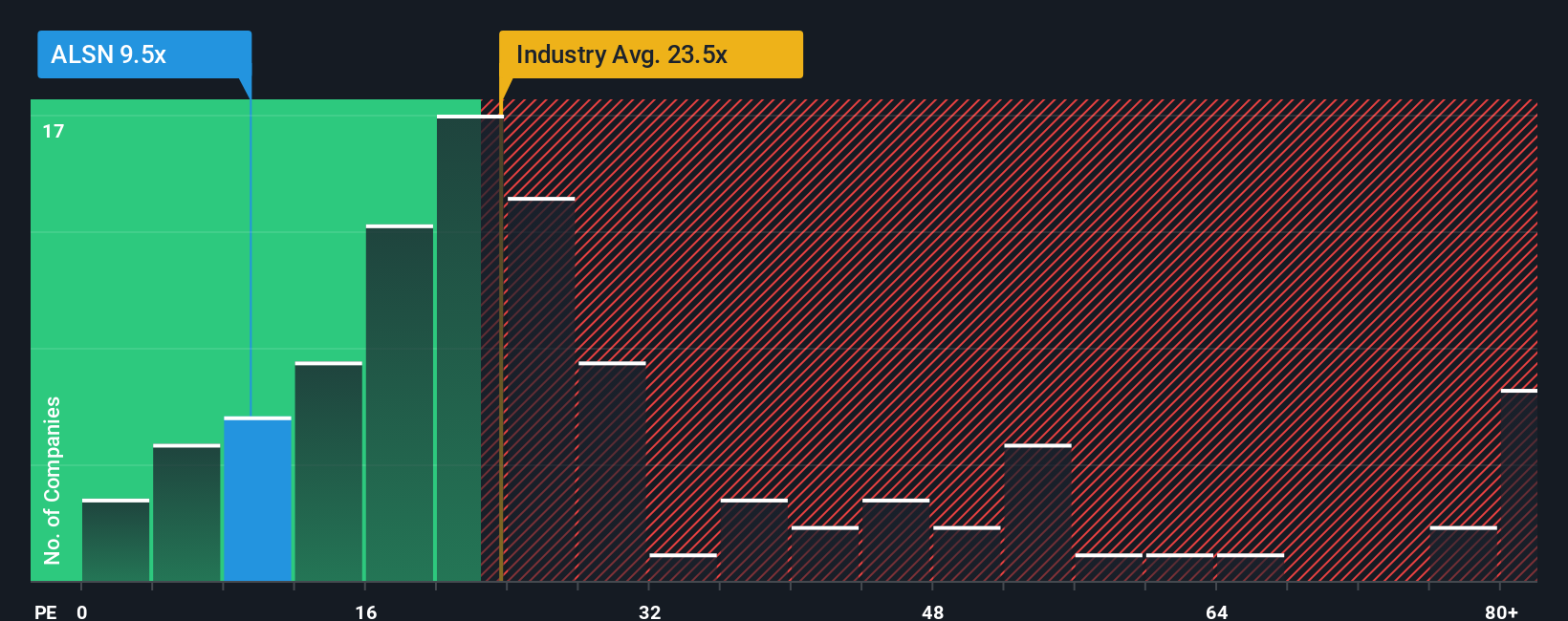

While the most popular narrative flags Allison Transmission as 9.4% overvalued against a $100.20 fair value, our P/E based view looks very different. At 13x earnings versus 27.4x for the US Machinery industry, peers at 22.9x and a fair ratio of 24x, the gap points to meaningful valuation risk or opportunity depending on which story you believe.

Build Your Own Allison Transmission Holdings Narrative

If you are not fully on board with this view, or simply prefer to test the numbers yourself, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Allison Transmission Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Allison Transmission is on your radar, do not stop there. Widen your watchlist with a few focused screeners that can surface fresh stock ideas in minutes.

- Hunt for potential mispricings by scanning these 864 undervalued stocks based on cash flows that might align better with your risk and return preferences.

- Spot emerging themes in artificial intelligence with these 24 AI penny stocks and see which businesses are building real earnings around this technology.

- Add a different source of income to your portfolio by checking these 13 dividend stocks with yields > 3% before the next round of payouts passes you by.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.