A Look At Amentum Holdings (AMTM) Valuation After Its New Fortune 500 Recognition

Amentum Holdings Inc TEMP AMTM | 0.00 |

Amentum Holdings (AMTM) has just been added to the Fortune 500 at position 313, putting a spotlight on the company’s scale, global reach, and relevance for investors tracking large defense and engineering contractors.

Despite the Fortune 500 recognition, Amentum’s share price has been under pressure, with the 30 day share price return down 8.4% and the year to date share price return down 25.2%. However, the 1 year total shareholder return is still positive at 1.74%.

If this kind of large scale engineering and infrastructure story interests you, it is a good moment to look across the sector using our 33 power grid technology and infrastructure stocks

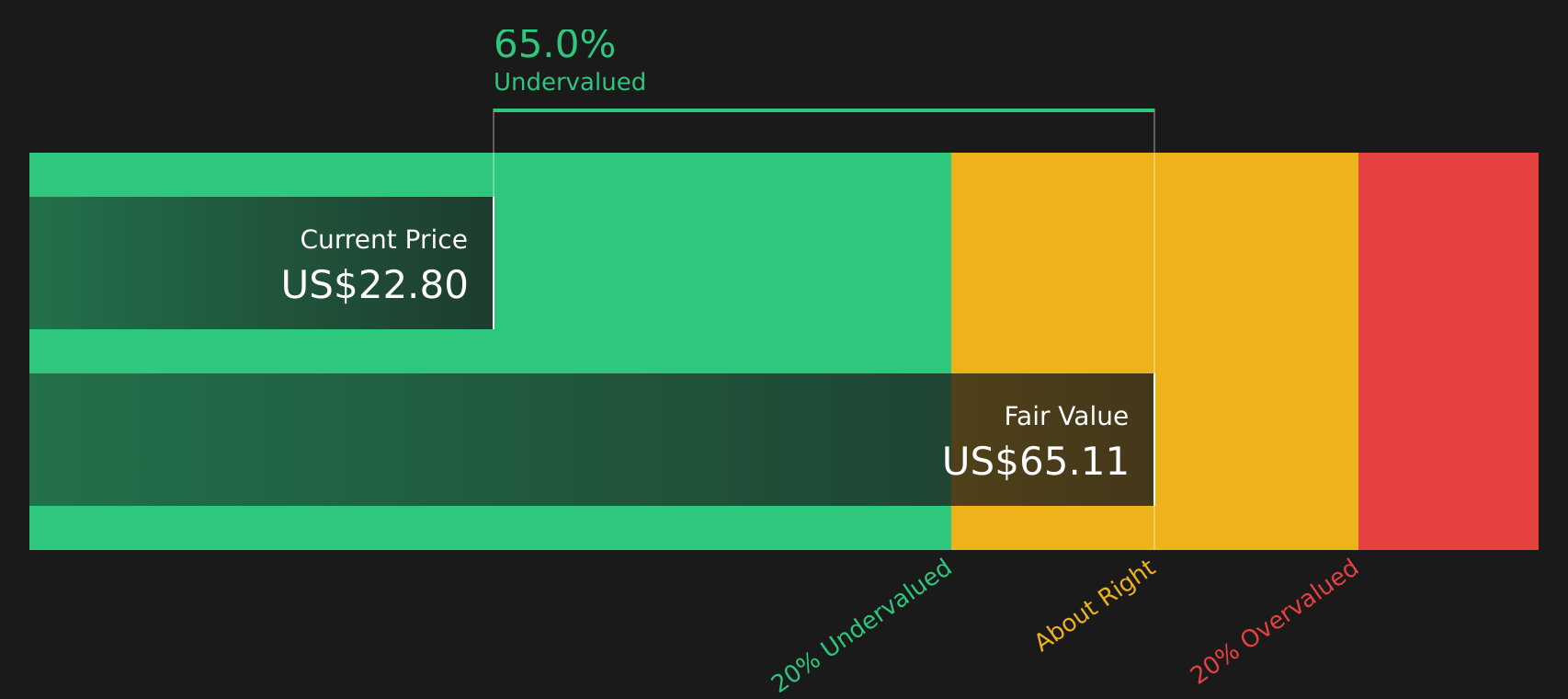

With Amentum trading at $22.80 and sitting at a sizeable discount to an average analyst price target of $33.50 and a reported intrinsic value gap, you have to ask: is there a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 20% Overvalued

The most widely followed narrative puts Amentum’s fair value at $22.75, almost exactly in line with the recent $22.80 close, yet still tags the stock as modestly overvalued once the full earnings path and risk profile are factored in.

Although demand for critical digital infrastructure is supported by rising AI and data workloads across data centers, networks and edge environments, the need to ramp new programs in Digital Solutions while margins currently track near 7.2% could limit how much of that revenue growth converts into higher segment earnings.

Want to see how a slow build in revenue, a step up in margins, and a lower future P/E all fit together? The key to this fair value call is how much earnings need to scale without relying on an aggressive multiple. Curious which profit, revenue and valuation assumptions the narrative threads together to land so close to today’s price? The full breakdown lays those moving parts out in black and white.

Result: Fair Value of $22.75 (OVERVALUED)

However, several factors could still flip this cautious view, including faster conversion of the US$48b backlog and proposal pipeline or stronger margin progress from higher value contracts.

Another View: Cash Flows Point a Different Way

The fair value of $22.75 comes from analyst earnings and P/E assumptions, but the SWS DCF model paints a very different picture. Amentum is trading at $22.80 compared with an estimated future cash flow value of $65.17. That implies the market could be pricing in much more caution than this cash flow view suggests, so which story do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Amentum Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment pulled between risks and rewards, it makes sense to move quickly, review the numbers for yourself and decide where you stand. To weigh the upside against the concerns in one place, start with these 3 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop with one stock when there are clear ways to broaden your watchlist and spot opportunities that better fit your goals and risk comfort.

- Target stability first by scanning companies in the 64 resilient stocks with low risk scores that aim to keep downside surprises in check.

- Hunt for quality at a discount using the 49 high quality undervalued stocks to spot stocks where fundamentals and price appear out of sync.

- Build a watchlist of stronger balance sheets with the solid balance sheet and fundamentals stocks screener (46 results), so you are not rushing to react when conditions change.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.