A Look At American Electric Power (AEP) Valuation After Recent Share Price Weakness

American Electric Power Company, Inc. AEP | 0.00 |

American Electric Power Company (AEP) has drawn investor attention after recent share price weakness, with the stock down about 7% over the past month and roughly 5% over the past 3 months.

Short term momentum has cooled, with the share price down 3.7% over the past week and 7.5% over the past month. However, the year to date share price return of 9.4% and 1 year total shareholder return of 26.3% indicate that the broader trend has still rewarded patient holders.

If you are looking beyond one utility stock and want to see where capital spending on grids and electrification could support other opportunities, check out 33 power grid technology and infrastructure stocks

So with AEP trading around $126.67, recent share price weakness, analyst price targets sitting higher, and an intrinsic value estimate implying a premium, should you see a mispriced opportunity here or assume the market is already factoring in future growth?

Most Popular Narrative: 12.1% Overvalued

According to the widely followed narrative, American Electric Power Company's fair value sits at $113, which is below the recent close around $126.67 and frames the current premium through a long term grid build out lens.

The most compelling driver is the unprecedented surge in data center load commitments. AEP’s incremental load pipeline has skyrocketed to 56 GW, a staggering 100% increase from just six months ago. This visibility into the next decade of demand allows AEP to aggressively expand its $72B+ capital plan, transforming "projected growth" into "guaranteed rate-base expansion."

Want to understand why a regulated utility is being framed as critical digital infrastructure? Instead of focusing on yield, this narrative leans on compounding revenue growth, higher margins and a richer profit multiple tied to data center demand. Curious how those ingredients add up to a fair value below the current share price?

Result: Fair Value of $113 (OVERVALUED)

However, this story can break if data center demand slows or if regulators hesitate on large grid projects. These factors could challenge the premium investors are currently paying.

Another View: P/E Paints a Different Picture

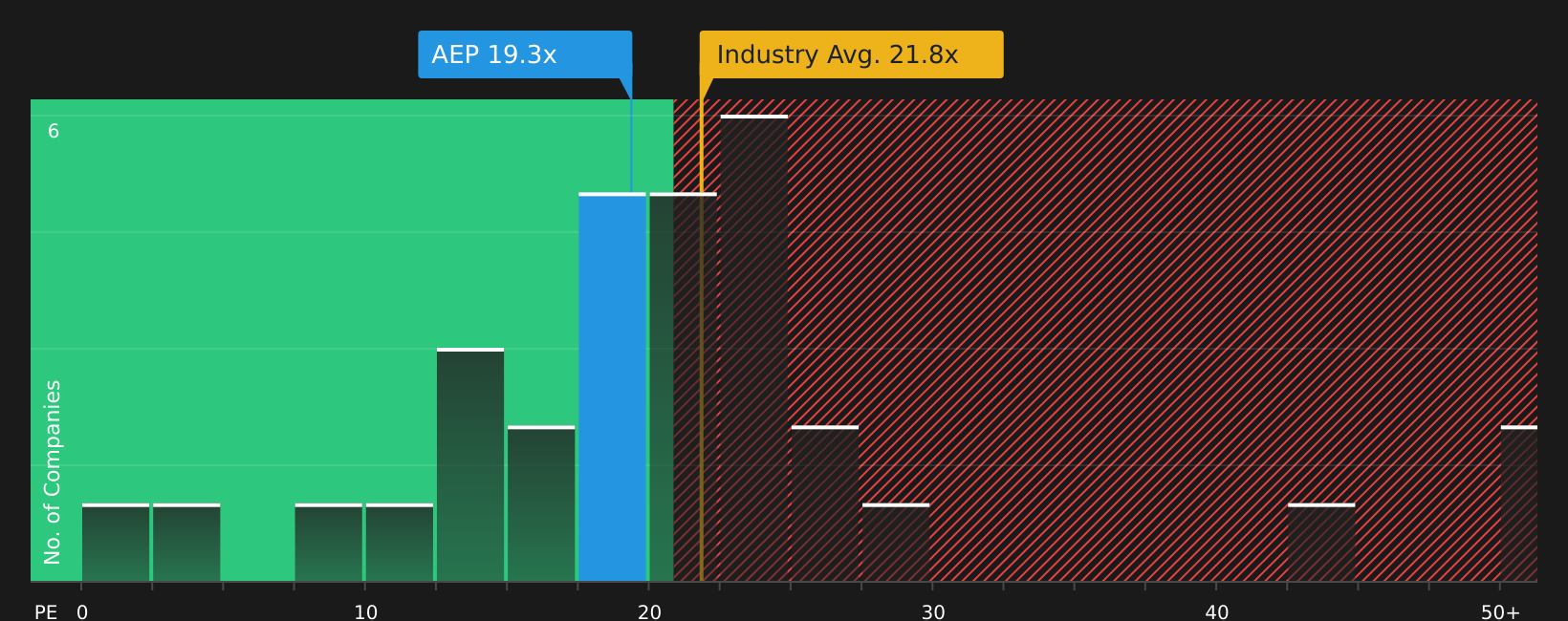

That $113 fair value from the narrative leans on long term grid growth, but the simple P/E comparison sends a softer message. AEP trades on 18.9x earnings, below the US Electric Utilities average of 21.3x, the peer average of 21.9x, and an estimated fair ratio of 25.3x. If the market ever moved closer to that fair ratio, today’s P/E would look more like a valuation cushion than a warning sign. The question is which signal you treat as more important.

Next Steps

The mixed messages on valuation and growth can make the story feel finely balanced.The mixed messages on valuation and growth can make the story feel finely balanced. Move quickly, pull up the underlying data, and weigh both the upside and the warning signs for yourself with 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop here, you risk missing other stocks that could fit your goals even better, so widen the lens and compare fresh ideas side by side.

- Spot potential bargains with solid fundamentals by scanning 46 high quality undervalued stocks before they attract broader attention.

- Strengthen your income focus by reviewing 10 dividend fortresses that pair higher yields with an emphasis on resilience.

- Prioritise capital preservation and steadier returns by filtering for 63 resilient stocks with low risk scores that score well on risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.