A Look At American Electric Power (AEP) Valuation After US$2.6b Follow On Equity Offering

American Electric Power Company, Inc. AEP | 0.00 |

American Electric Power Company (AEP) has just completed a roughly US$2.6b follow on equity offering of more than 20 million common shares, a material move tied directly to its expanding capital investment plans.

The follow on offering came after a strong first quarter update and guidance reaffirmation. The announcement initially saw the stock fall about 3% in after hours trading as investors weighed dilution risk against future project funding. Even with recent weakness, including a 1 month share price return of down 6.9%, momentum over longer horizons has been positive, with 1 year total shareholder return of 25.3% and 5 year total shareholder return of 73.0%.

If you are thinking about how grid investments and rising power demand could affect other companies, it may be a good time to scan 38 power grid technology and infrastructure stocks

With AEP’s share price around US$125 after a 1 month decline of 6.9%, yet a 1 year total return of 25.3%, the key question is simple: is this pullback a chance to buy, or is the market already pricing in its future growth?

Most Popular Narrative: 10.8% Overvalued

Based on the most followed narrative fair value of $113 compared with the last close at $125.15, American Electric Power Company looks priced above that reference point, but the narrative itself leans heavily on long term grid demand.

The most compelling driver is the unprecedented surge in data center load commitments. AEP’s incremental load pipeline has skyrocketed to 56 GW, a staggering 100% increase from just six months ago. This visibility into the next decade of demand allows AEP to expand its $72B+ capital plan, transforming "projected growth" into "guaranteed rate-base expansion."

Curious what earnings path and margin profile sit behind that fair value and capital plan story? The narrative leans on specific growth, profitability and discount rate assumptions that are not obvious from the headline numbers.

Result: Fair Value of $113 (OVERVALUED)

However, this hinges on hyperscaler demand remaining firm and on regulators continuing to approve and rate base large grid projects according to the assumed timelines and terms.

Another View: Multiples Paint a Different Picture

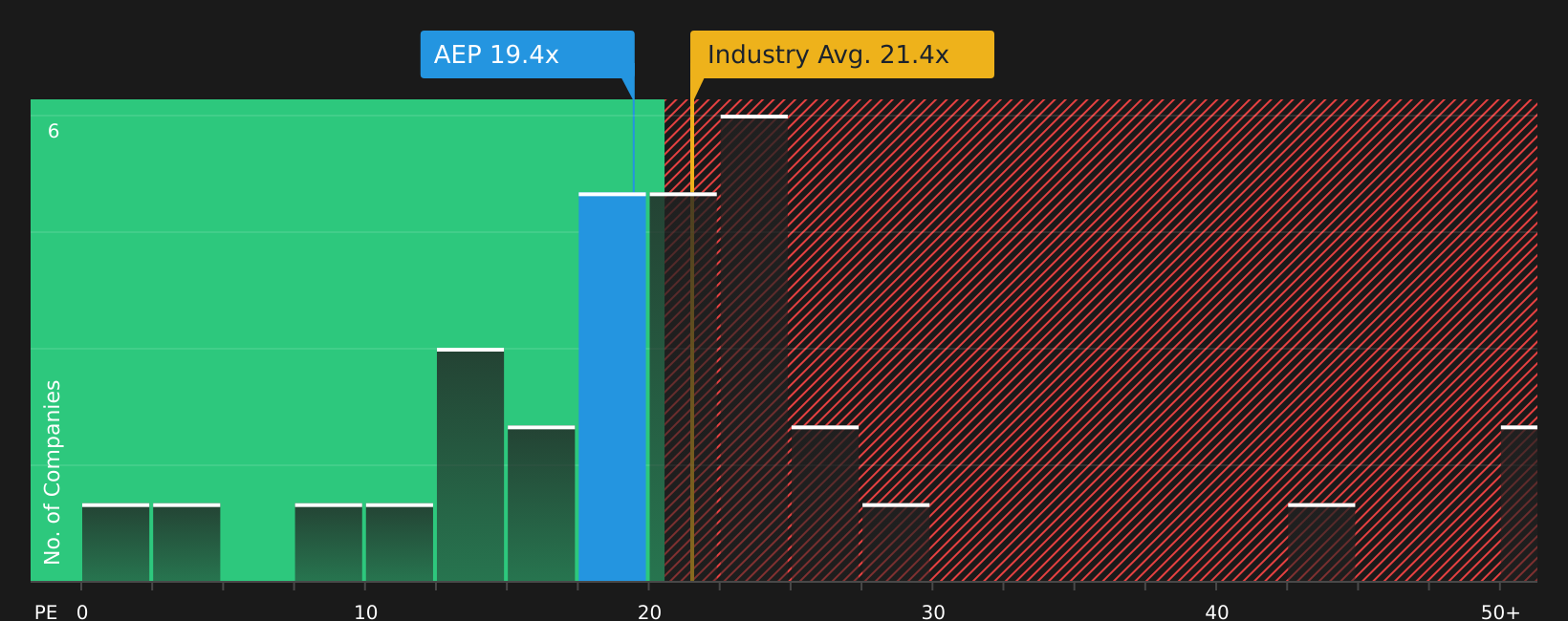

While the user narrative flags AEP as about 10.8% overvalued versus a $113 fair value, the current P/E of 18.6x tells a different story. It sits below both the Electric Utilities industry average of 21.6x and the peer average of 23.5x, and below a fair ratio of 25.4x. This points to more valuation risk if sentiment cools or a potential cushion if enthusiasm returns. Which signal do you put more weight on?

Next Steps

With sentiment clearly mixed, it makes sense to check the full picture for yourself and decide how the balance of risks and rewards stacks up. To see how the positives compare with the concerns highlighted by other investors, review the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other compelling setups, so take a few minutes to scan fresh ideas that match your preferences.

- Target long term value potential by checking out 50 high quality undervalued stocks with strong fundamentals that might not yet be fully appreciated by the market.

- Strengthen your income stream by reviewing 12 dividend fortresses that aim to pair higher yields with business resilience.

- Lower your portfolio stress by focusing on 66 resilient stocks with low risk scores that screen well on financial health and volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.