A Look At American Electric Power (AEP) Valuation As Ohio Data Center Grid Plan Faces Regulatory Scrutiny

American Electric Power Company, Inc. AEP | 0.00 |

American Electric Power Company (AEP) is in the spotlight after consumer advocates challenged the proposed formula rate for a roughly $1.1b Ohio transmission project tied to data center driven demand.

The recent regulatory pushback comes after a period of firm momentum, with a 90 day share price return of 13.68% and a 1 year total shareholder return of 25.71%. This points to interest that has built rather than faded across both shorter and longer horizons.

If this kind of large scale grid investment has your attention, it could be a good moment to size up similar power grid opportunities using our 26 power grid technology and infrastructure stocks

With AEP shares up 25.71% over the past year and the stock trading about 4.9% below the average analyst price target, the key question is whether current valuations still leave room for upside or if the market is already baking in expectations for future performance.

Most Popular Narrative: 4.7% Undervalued

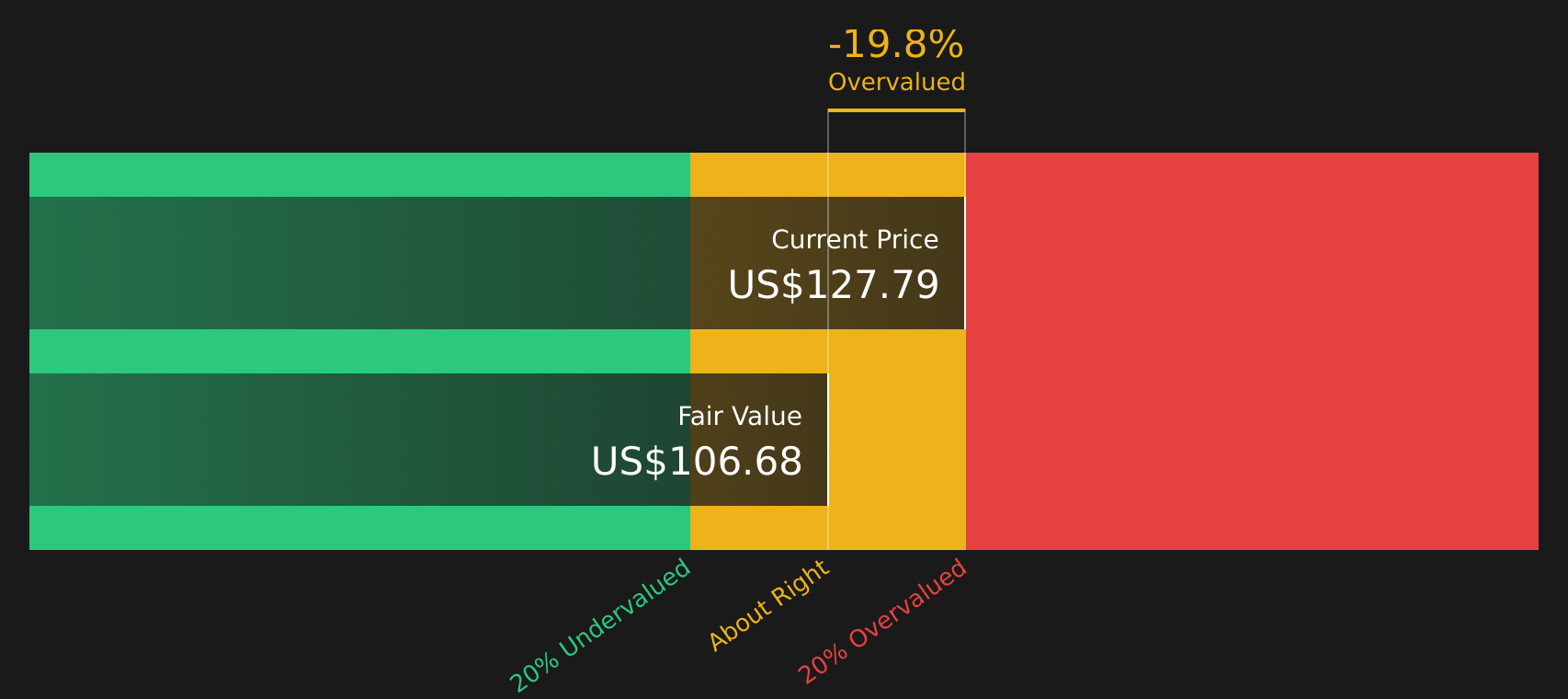

With American Electric Power Company last closing at $131.08 versus a narrative fair value of $137.47, the current setup centers on how far data center driven load and transmission spend can carry future earnings.

AEP is capitalizing on increased load growth, expecting retail load growth of 8% to 9% annually through 2027, driven by commercial and industrial demand, which should significantly boost revenue.

The company has a substantial capital investment plan of $54 billion over the next 5 years, with an additional potential of $10 billion, primarily aimed at expanding transmission and distribution, indicating future growth in earnings.

Analysts are effectively tying a multiyear construction runway to steady earnings expansion, together with modest margin pressure and a richer future earnings multiple. The key questions are which specific growth, profitability and discount rate assumptions anchor that $137.47 fair value, and how sensitive the outcome is to even small changes in those inputs.

Result: Fair Value of $137.47 (UNDERVALUED)

However, this depends on commercial load growth as well as complex Ohio and federal regulatory decisions, which could slow project timing or reduce returns if outcomes fall short of expectations.

Another View: DCF Flags A Different Story

While analysts see about 4.7% upside to $137.47, the SWS DCF model points the other way, with an estimated future cash flow value of $109.43 versus the current $131.08 share price. That gap suggests investors are paying up for long term growth. The question is which set of assumptions you trust more.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out American Electric Power Company for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and plenty of opinion around growth, it pays to check the numbers yourself and act before sentiment shifts. To weigh both sides of the story, start with the 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one company, you risk missing other opportunities that could fit your goals even better, so broaden your search with a few focused screens.

- Target potential mispricings by scanning 58 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their underlying strengths.

- Build a steadier income stream by checking out 12 dividend fortresses that concentrate on higher yielding names with a focus on durability.

- Aim for peace of mind by reviewing 64 resilient stocks with low risk scores designed to highlight companies with more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.