A Look At American Electric Power Company (AEP) Valuation After Data Center Driven Earnings Beat And Capex Expansion

American Electric Power Company, Inc. AEP | 0.00 |

American Electric Power Company (AEP) has just posted first quarter 2026 earnings that came in ahead of expectations, reaffirmed its full year outlook and outlined a larger, data center driven contracted load pipeline.

The strong first quarter earnings beat and reaffirmed guidance come after a 90 day share price return of 9.74% and a year to date share price return of 14.46%. The 1 year total shareholder return of 30.22% and 5 year total shareholder return of 82.21% suggest momentum has been building over time, despite a recent 1 day share price decline of 3.27% following the results.

If you are thinking about how data center demand and grid upgrades could affect other opportunities, it is worth reviewing our focused list of 34 power grid technology and infrastructure stocks

With AEP shares up 30.22% over the past year and trading about 8.8% below the average analyst price target despite an implied premium to some intrinsic estimates, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 17.3% Overvalued

At a last close of $132.56 versus a narrative fair value of $113.00, the current setup reflects a premium that, according to sorkdhkddlek, rests on a very specific view of data center driven grid demand and long term capital deployment.

The most compelling driver is the unprecedented surge in data center load commitments. AEP’s incremental load pipeline has skyrocketed to 56 GW, a staggering 100% increase from just six months ago. This visibility into the next decade of demand allows AEP to aggressively expand its $72B+ capital plan, turning projected growth into a clearer path for rate-base expansion.

Curious how a 56 GW pipeline, a multi decade capex roadmap and a premium P/E all tie into one fair value anchor? The full narrative connects earnings power, regulated returns and hyperscaler commitments into a single valuation logic that is far from obvious at first glance.

Result: Fair Value of $113.00 (OVERVALUED)

However, this hinges on data center commitments and long term grid projects holding up, while regulatory decisions or shifts in capital costs could easily unsettle that premium story.

Another Take: P/E Ratios Point to a Different Story

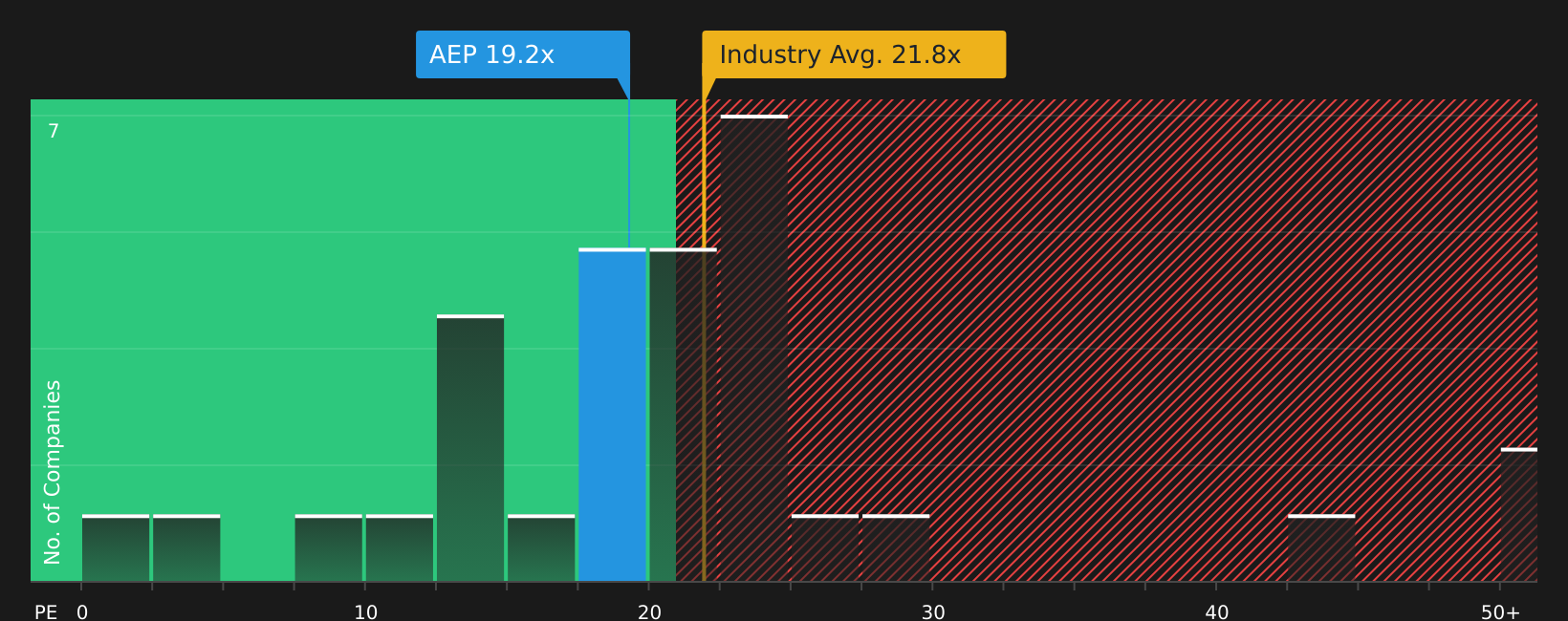

While the narrative fair value pins AEP at $113.00 and calls the stock overvalued, the current P/E of 19.7x looks cheaper than peers at 24.1x, the Electric Utilities industry at 21.9x, and even a fair ratio of 25.4x. This raises the question: is the premium really as stretched as it sounds, or is the market still catching up?

Next Steps

With mixed signals on value and sentiment, the real question is how it all stacks up for you, right now, on your terms. Take a close look at the full picture of potential upsides and concerns by reviewing the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

Once you are clear on how AEP fits your plan, do not stop there, the wider market still holds plenty of potential opportunities worth a closer look.

- Target quality at a discount by scanning companies that combine robust fundamentals with attractive pricing using the 44 high quality undervalued stocks.

- Build income potential into your portfolio by reviewing companies highlighted in the 12 dividend fortresses.

- Dial down portfolio risk by focusing on companies that pass the strict filters in the 74 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.