A Look At Antero Midstream (AM) Valuation After Earnings Beat And $400 Million Utica Asset Sale

Antero Midstream Corp. AM | 22.60 22.60 | -0.66% 0.00% Pre |

Antero Midstream (AM) has been in focus after reporting fourth quarter 2025 earnings per share above analyst expectations, while revenue lagged projections, and after closing a $400 million sale of its Utica Shale midstream assets.

Those earnings and asset sale headlines have come alongside strong share price momentum, with a 17.12% 1 month share price return, 28.87% year to date share price return, and a very large 5 year total shareholder return of 272.98% suggesting interest has been building rather than fading.

If events around Antero Midstream have you looking across the energy value chain, this could be a good moment to scan 23 power grid technology and infrastructure stocks as another way to spot potential opportunities.

With earnings per share ahead of expectations, a $400 million asset sale completed, and the share price already up sharply, the key question now is simple: Is Antero Midstream still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 10.8% Overvalued

Analysts in the most followed narrative see fair value for Antero Midstream at $20.86, below the last close of $23.12, which sets up a clear valuation debate.

Long-term, exclusive contracts with Antero Resources, combined with over 20 years of high-quality, dedicated natural gas inventory, ensure stable minimum volume commitments, supporting strong earnings visibility and reducing risk for future net margins.

Curious what kind of revenue growth, margin profile, and future P/E multiple underpin that fair value and justify a higher valuation than the broader oil and gas group? The narrative lays out a detailed earnings path, assumptions for profitability, and how higher future pricing of those earnings fits with Antero Midstream's current position in the Appalachian Basin.

Result: Fair Value of $20.86 (OVERVALUED)

However, heavy reliance on Antero Resources in Appalachia and potential pressure on long term natural gas demand could both challenge the earnings and valuation story.

Another View: Cash Flows Point To A Very Different Story

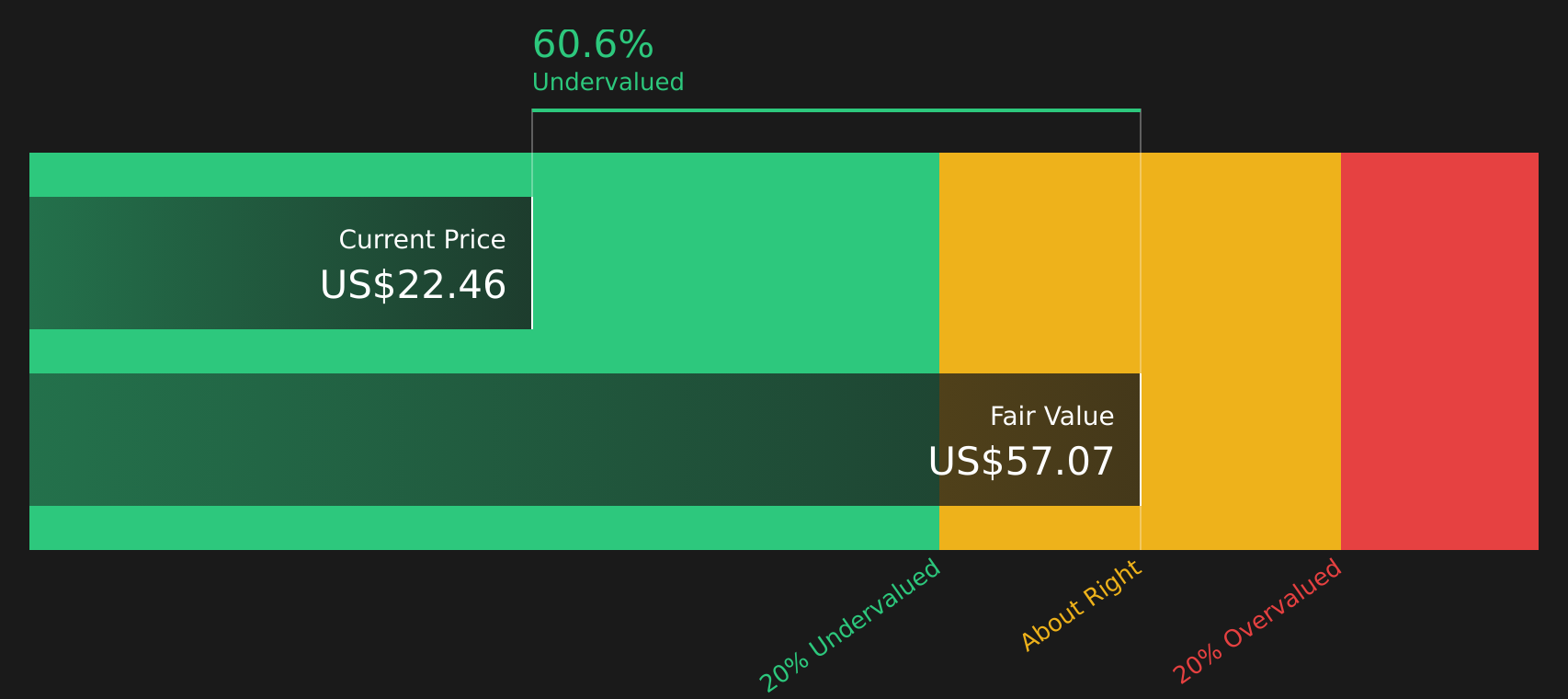

While the most followed narrative sees Antero Midstream as 10.8% overvalued at $23.12 versus a $20.86 fair value, our DCF model paints almost the opposite picture. It shows an estimated future cash flow value of $59.05, suggesting the current price sits far below that level.

DCF models lean heavily on long term cash generation and discount rates. The gap between $23.12 and $59.05 raises a simple question for you: are analysts being too cautious on long term cash flows, or is the DCF too optimistic about how durable those cash streams really are?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Antero Midstream for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed views on value and plenty of moving parts, it makes sense to look at the data yourself and decide where you stand. To help frame that view quickly, you can weigh up 3 key rewards and 2 important warning signs and see how the trade off between concern and optimism looks to you.

Looking for more investment ideas?

If you stop at Antero Midstream, you miss a wider field of opportunities. Use the Simply Wall St screener to quickly spot other stocks that fit your style.

- Target reliability with 67 resilient stocks with low risk scores to aim to keep risk scores in check while still giving you a broad set of options to review.

- Hunt for value with 50 high quality undervalued stocks to combine quality fundamentals with prices that may still sit below what the underlying business could justify.

- Build a watchlist of potential standouts using a screener containing 23 high quality undiscovered gems before they sit firmly on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.