A Look At Calumet (CLMT) Valuation After First Quarter Sales Growth And A Wider Net Loss

Calumet, Inc. CLMT | 0.00 |

Calumet (CLMT) opened the quarter with an earnings update that will likely catch investors’ attention, as sales reached US$1,029.7 million while the company reported a wider net loss of US$317 million.

The latest earnings update comes after a strong run in Calumet’s stock, with the share price at US$31.43 and a year to date share price return of 60.77%, while the 1 year total shareholder return of 126.60% suggests momentum has been strong despite recent short term share price weakness, including a 7 day share price return down 8.90%.

If this quarter’s move has you thinking about where else strong trends might appear next, it could be worth scanning a focused list of 37 power grid technology and infrastructure stocks

So with Calumet’s strong recent share price performance sitting alongside a wider quarterly loss, the key question is whether the current valuation leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 34% Overvalued

Calumet’s most followed narrative points to a fair value of $23.45, which sits well below the last close at $31.43, putting the current price under scrutiny.

Repositioning away from commoditized products toward high-margin specialties, together with scale advantages and sustained regulatory tailwinds for renewable fuels, strategically positions Calumet to benefit from the multi-decade shift to sustainable infrastructure, transportation, and alternative energy markets, trends expected to underpin top-line growth and improve earnings quality in coming years.

Curious what kind of revenue trajectory and margin lift this narrative is banking on, and how that ties into a premium future earnings multiple? The fair value relies on a specific path for sales, profitability and the cost of capital that differs from current market pricing. The full narrative spells out exactly how those moving parts are expected to line up.

Result: Fair Value of $23.45 (OVERVALUED)

However, this narrative still leans heavily on continued regulatory support for renewable fuels and on managing substantial debt, either of which could quickly challenge the current thesis.

Another View: Multiples Tell a Different Story

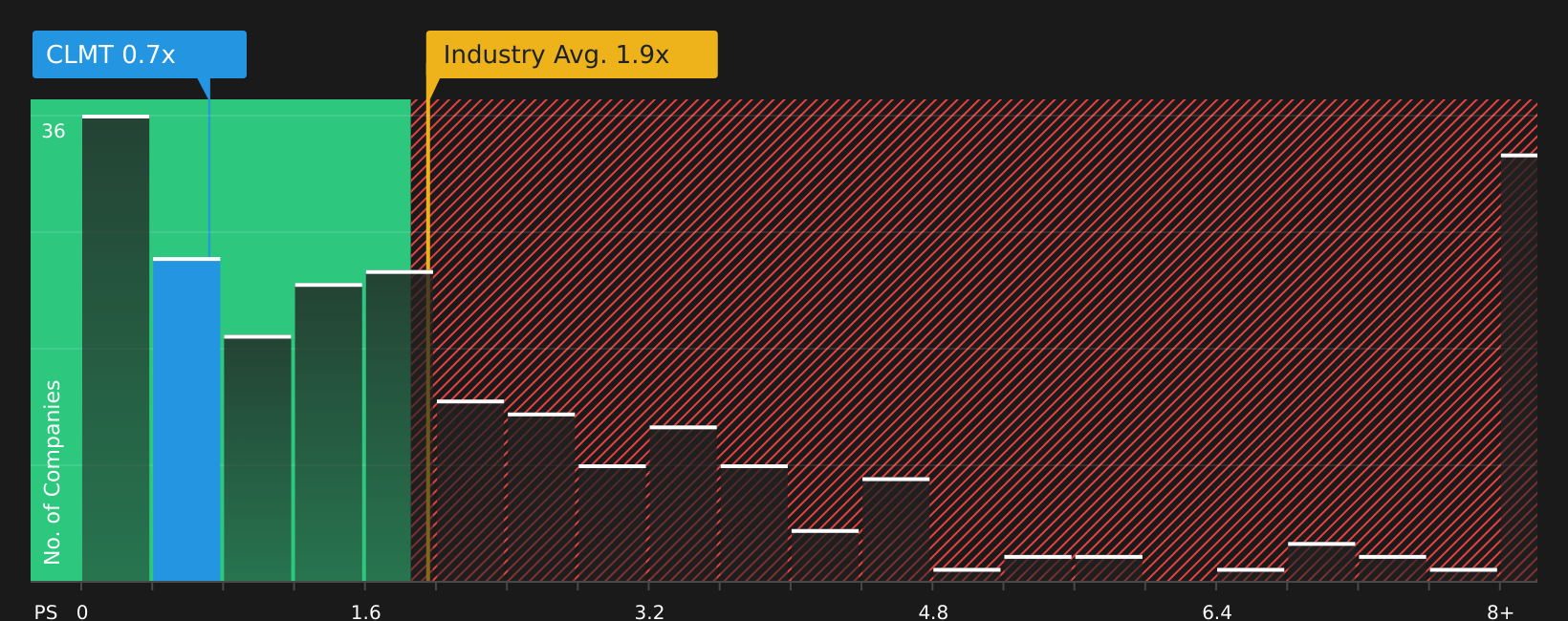

While the fair value narrative points to Calumet trading about 34% above its estimated value at $23.45, the P/S ratio of 0.7x paints a different picture. It sits well below the wider US Oil and Gas industry on 2.1x, yet above closer peers at 0.3x, and is in line with a fair ratio of 0.7x. For investors, that mix of discount versus the broader industry and premium versus peers raises a simple question: which side of the comparison should carry more weight in your own view of risk and opportunity?

Next Steps

With a mix of concerns and optimism running through this story, it makes sense to move quickly, review the underlying data, and stress test the thesis against your own expectations using the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If this update has sharpened your thinking, do not stop here. Use a targeted stock search to spot opportunities that fit your own risk and return preferences.

- Sharpen your hunt for quality by scanning 47 high quality undervalued stocks that combine stronger fundamentals with prices that may not fully reflect them yet.

- Prioritise resilience by checking 68 resilient stocks with low risk scores that score well on balance sheet strength and overall risk metrics.

- Get ahead of the crowd by reviewing a screener containing 23 high quality undiscovered gems before they sit on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.