A Look At Carvana (CVNA) Valuation After Record Q1 2026 Growth And Profitability

Carvana CVNA | 0.00 |

Carvana (CVNA) is back in focus after reporting Q1 2026 results that featured record retail units sold, revenue, and profitability, extending its streak to a sixth straight quarter of significant year-over-year retail unit growth.

The recent Q1 2026 beat and Chicago IRC expansion have not prevented a pullback, with the share price down 13.8% over 7 days and 16.1% year to date, while the 3 year total shareholder return remains very large.

If Carvana’s swings have you thinking about where else growth and volatility might show up, this could be a good moment to check out 19 top founder-led companies

With Q1 momentum, a pullback in the share price, and a last close of US$67.17 against an average analyst target of US$92.92, is Carvana offering a mispriced entry or is the market already factoring in future growth?

Most Popular Narrative: Fairly Valued

Carvana’s last close of $67.17 sits well above the narrative fair value of $0, which signals a highly skeptical stance on the stock’s underlying fundamentals.

There are growing concerns among some market observers that Carvana's business model may be masking deeper financial instability. The company has a long history of operating with negative cash flow followed by rapid debt expansion, and unusually aggressive revenue recognition practices that raise questions about the sustainability of its margins. Analysts have also noted that Carvana's reported improvements in profitability often coincide with accounting adjustments rather than genuine operational strength, suggesting the possibility of earnings "smoothing out." Additionally, the firm's reliance on securitizing subprime auto loans creates opacity around the true quality of its assets; rising delinquencies in the used car loan market increase the risk that these securities are overvalued. When a company simultaneously carries heavy debt, thin cash reserves and complex financial structures that are difficult for outside investors to verify, it breeds skepticism.

According to Sirupy, the key tension in this narrative is simple: reported profitability versus questions around cash generation, leverage, and how those earnings are being recognized. Want to see which assumptions sit behind a fair value of effectively zero, and how they balance revenue growth, margins, and financing structure?

Result: Fair Value of $0 (OVERVALUED)

However, sustained revenue and net income growth, or a clearer resolution of accounting and regulatory concerns, could challenge such a deeply skeptical fair value stance.

Another View: Cash Flows Point To Caution

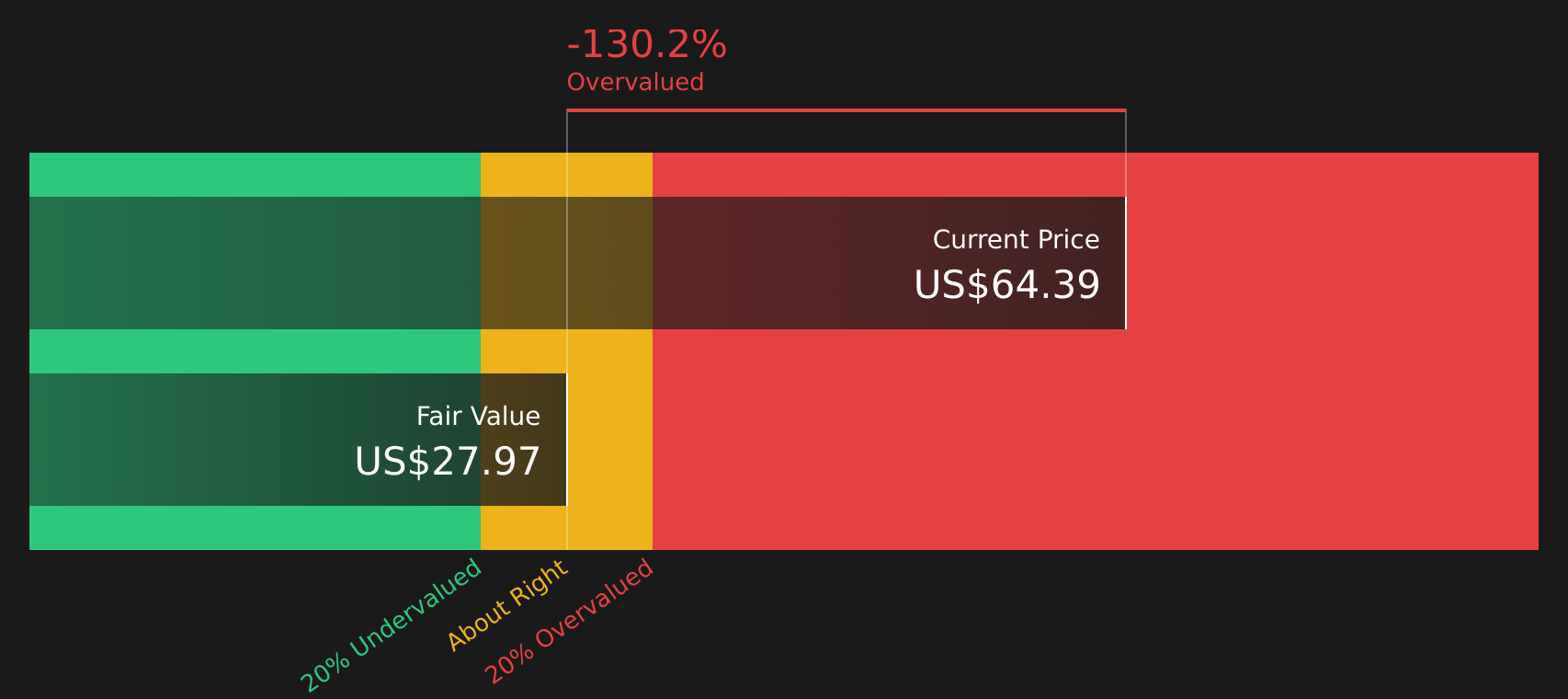

While the user narrative argues for a fair value of $0, Simply Wall St’s DCF model still comes out with a positive figure of $27.70 per share, which is well below the current $67.17 price and flags the stock as overvalued using this framework too. For you, the real question is whether the growth and profitability story justifies paying well above what this cash flow based model suggests.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Carvana for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of skepticism and optimism feels familiar, take a moment to review the underlying numbers and sentiment yourself, then weigh up the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Carvana has you thinking harder about risk, reward, and timing, do not stop here. Broaden your watchlist with a few focused sets of ideas.

- Target potential upside with companies that screens highlight as attractively priced using the 49 high quality undervalued stocks.

- Seek resilience by reviewing the 66 resilient stocks with low risk scores that aim to limit downside while still keeping you exposed to opportunities.

- Hunt for overlooked opportunities before they are widely discussed by checking the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.