A Look At Chubb (CB) Valuation After Dividend Increase And US$7.5b Buyback Authorization

Chubb Limited CB | 0.00 |

Chubb (CB) has drawn fresh attention after shareholders approved a 5.2% dividend increase and a new US$7.5b share repurchase program, putting capital return policy firmly in focus for investors.

At a share price of US$330.26, Chubb’s recent news on dividends and buybacks comes after a steady year to date. A 6.51% year to date share price return and a 16.53% 1 year total shareholder return suggest that momentum has been building rather than fading.

If you are weighing Chubb’s mix of income and growth, it can help to see what else the market is rewarding right now. You could start with 20 top founder-led companies

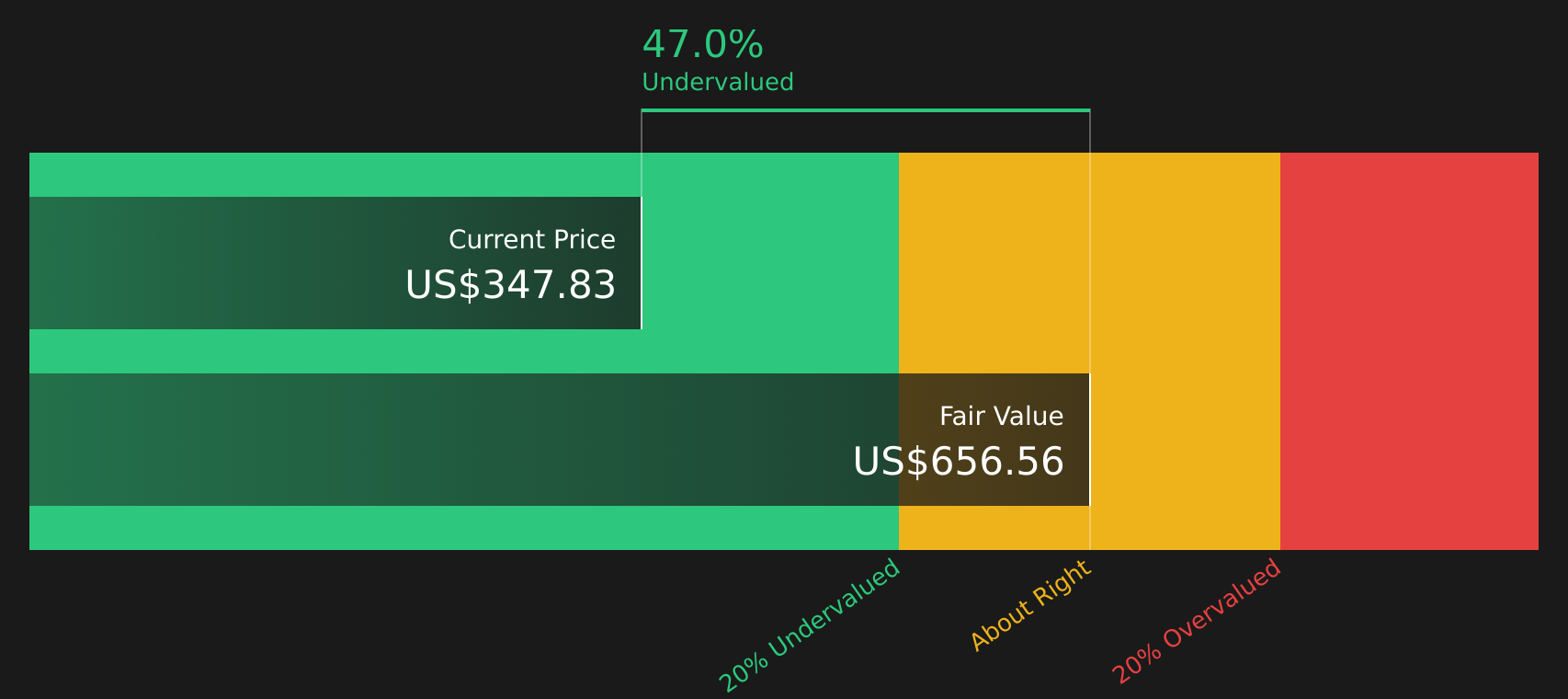

But with Chubb trading at US$330.26 and an indicated intrinsic value gap, plus only a small discount to analyst targets, should you see this as mispricing in your favor, or is the market already baking in future growth?

Most Popular Narrative: 33.7% Overvalued

According to the most followed narrative on Chubb, the fair value sits well below the last close of $330.26, which paints a very different picture to recent share price strength.

Chubb’s future growth is expected to be driven by strategic expansion into emerging markets, technological innovation, product and service diversification, strategic acquisitions, and a strong focus on sustainability and customer experience. By capitalizing on these opportunities and navigating the challenges of the evolving insurance landscape, Chubb is well-positioned to maintain its competitive edge and achieve sustained growth.

Curious how this growth story still results in a fair value below today’s price? The narrative leans on specific revenue trends, profitability assumptions, and a tight discount rate to get there.

Result: Fair Value of $247.08 (OVERVALUED)

However, this overvaluation case could be challenged if Chubb’s annual revenue and net income, which both recently declined, signal a more persistent earnings reset than assumed.

Another View: Cash Flows Point the Other Way

While the popular narrative suggests Chubb is overvalued at a fair value of $247.08, our DCF model paints a very different picture. On this view, Chubb at $330.26 sits well below a future cash flow value of $666.29. This frames today’s price as a potential discount rather than a premium. So which story do you lean toward: earnings multiples or long term cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Chubb for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split views on Chubb’s value and outlook make this a good moment to check the underlying data yourself and decide where you stand. If you want a clear snapshot of what investors are worried about and what they are excited about, take a look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit your goals even better, so keep widening your watchlist thoughtfully.

- Target consistent income potential by reviewing companies in the 10 dividend fortresses that may appeal if you prioritize yield alongside stability.

- Hunt for quality at a reasonable price by scanning the 53 high quality undervalued stocks that filters for strong fundamentals and potentially attractive pricing.

- Strengthen your downside protection by reviewing the 66 resilient stocks with low risk scores that focuses on stocks with lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.