A Look At Comstock Resources (CRK) Valuation As Quarterly Earnings Approach On February 11, 2026

Comstock Resources, Inc. CRK | 16.27 | +0.12% |

Comstock Resources (CRK) is set to report quarterly earnings on February 11, 2026, an event drawing attention as investors weigh its 47.75% revenue growth versus peers against higher debt and an expected EPS of $0.11.

At a share price of $20.42, Comstock Resources has seen a 9.12% decline in its 7 day share price return and a 19.03% decline over 90 days. However, its 1 year total shareholder return of 10.86% and 5 year total shareholder return of 282.61% show that long term holders have still been rewarded even as near term momentum has cooled ahead of earnings.

If this earnings update has you reassessing energy exposure, it could be a good moment to look across the sector with our screener of 87 nuclear energy infrastructure stocks as potential alternatives.

With the stock trading at $20.42 and an intrinsic value estimate suggesting a wide discount, yet only a small gap to the analyst price target, you have to ask: is this a buying opportunity, or is future growth already priced in?

Most Popular Narrative: 1.4% Undervalued

With Comstock Resources last closing at $20.42 and the most followed fair value estimate at $20.71, the current price sits only slightly below that narrative line.

The analysts have a consensus price target of $19.036 for Comstock Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $10.0.

Curious what justifies a fair value near today’s price, yet such a wide spread in analyst views? Earnings, margins and the required return assumptions all carry the story.

Result: Fair Value of $20.71 (UNDERVALUED)

However, the heavy focus on Haynesville, along with ongoing capital needs for drilling and infrastructure, means any regional setbacks or cost pressures could quickly challenge this undervalued story.

Another View: Earnings Multiple Paints a Tougher Picture

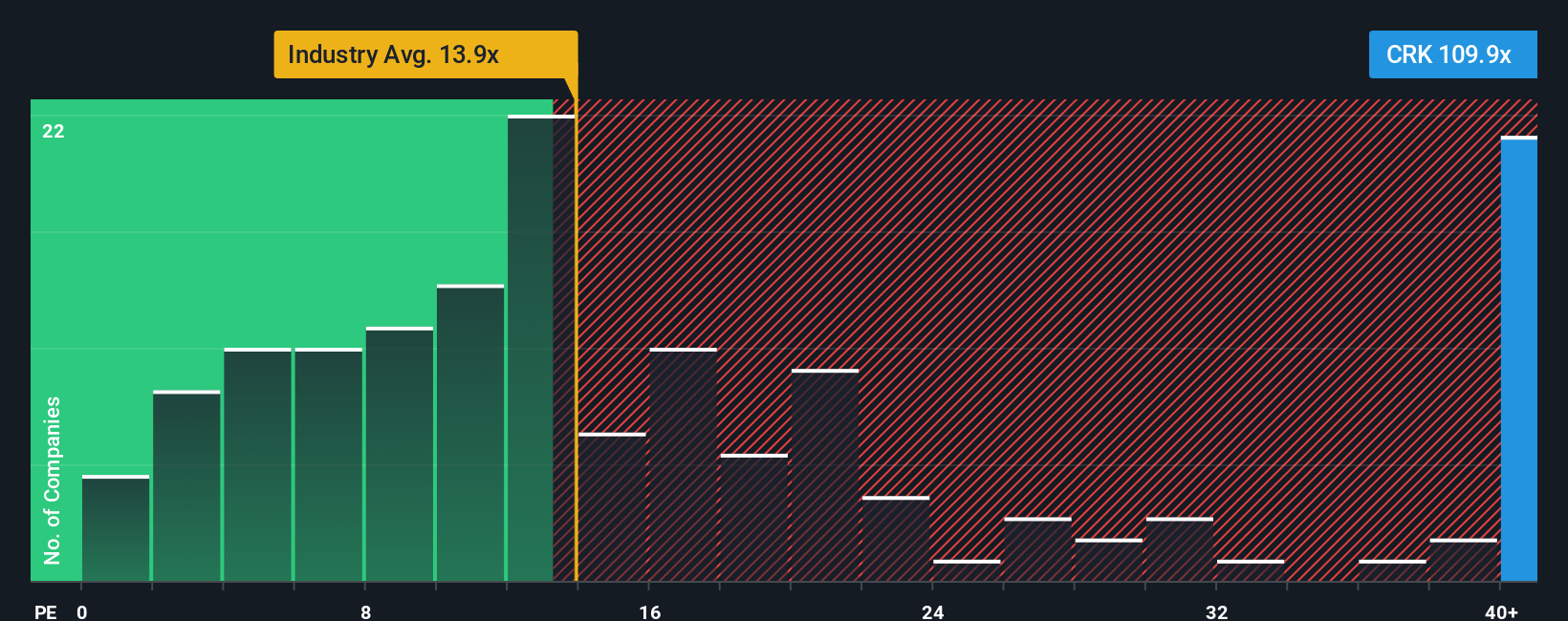

While the most followed fair value narrative points to Comstock Resources looking modestly undervalued, the current P/E ratio of 88.7x tells a very different story. That level is far above both the fair ratio of 27.8x and the US Oil and Gas industry average of 14.1x, which suggests investors today are paying a steep price for each dollar of earnings compared to peers.

Against that backdrop, the question for you is simple: are you comfortable paying such a high earnings multiple when the fair ratio and industry markers sit so much lower, or do you see that gap as valuation risk that is hard to ignore?

Build Your Own Comstock Resources Narrative

If you are not fully on board with this view or prefer to test the numbers yourself, you can build a custom thesis in just a few minutes, starting with Do it your way.

A great starting point for your Comstock Resources research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Once you have a view on Comstock Resources, do not stop there. Widen your watchlist with a few focused sets of ideas that fit different goals.

- Target value first and see which companies our screener flags as 51 high quality undervalued stocks with strong fundamentals to back up the story.

- Prioritise resilience and stress test your portfolio by checking out 83 resilient stocks with low risk scores, built around businesses with more robust risk profiles.

- Hunt for earlier stage potential and scan our 27 elite penny stocks with strong financials for smaller names that still pass key financial quality filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.