A Look At Cummins (CMI) Valuation After Earnings Volatility Guidance Update And Dividend Increase

Cummins Inc. CMI | 549.68 | -0.07% |

Cummins (CMI) is back in focus after its latest quarterly earnings update, a mixed market reaction to GAAP results, fresh 2026 guidance, a higher dividend, and sharper priorities for its Accelera business.

The recent earnings volatility, updated 2026 guidance and higher dividend have all landed against a strong run in the shares. Cummins’ 90 day share price return of 27.28% and 1 year total shareholder return of 62.62% point to momentum that has been building rather than fading.

If this has you thinking more broadly about industrial power and electrification themes, it could be a good moment to see what else is out there through our 24 power grid technology and infrastructure stocks.

With Cummins trading near its analyst price target and showing an 18% intrinsic discount estimate, the real question is whether recent earnings noise has left value on the table or if the market is already pricing in future growth.

Most Popular Narrative: 5% Overvalued

Against Cummins’ last close of $588.79, the most widely followed narrative points to a fair value of $560.57, suggesting the recent share price sits slightly ahead of that modeled view while still reflecting confidence in the long term cash flow story.

The company's two year plus backlog and continued capacity expansions in Power Systems position it to sustain elevated sales growth and margins, especially as additional production capacity comes online in 2026, directly benefiting future revenue and margin expansion.

If you are curious what kind of revenue path and margin profile justify that fair value tag and higher future earnings power, along with the profit multiple this narrative leans on, and how the discount rate ties it all together without assuming tech like growth but still baking in steady improvement, you will want to see how all those moving pieces fit in the full story.

Result: Fair Value of $560.57 (OVERVALUED)

However, there is still meaningful execution risk if North America truck demand remains weak for an extended period and Accelera continues to report EBITDA losses without clear traction.

Another Take On Value

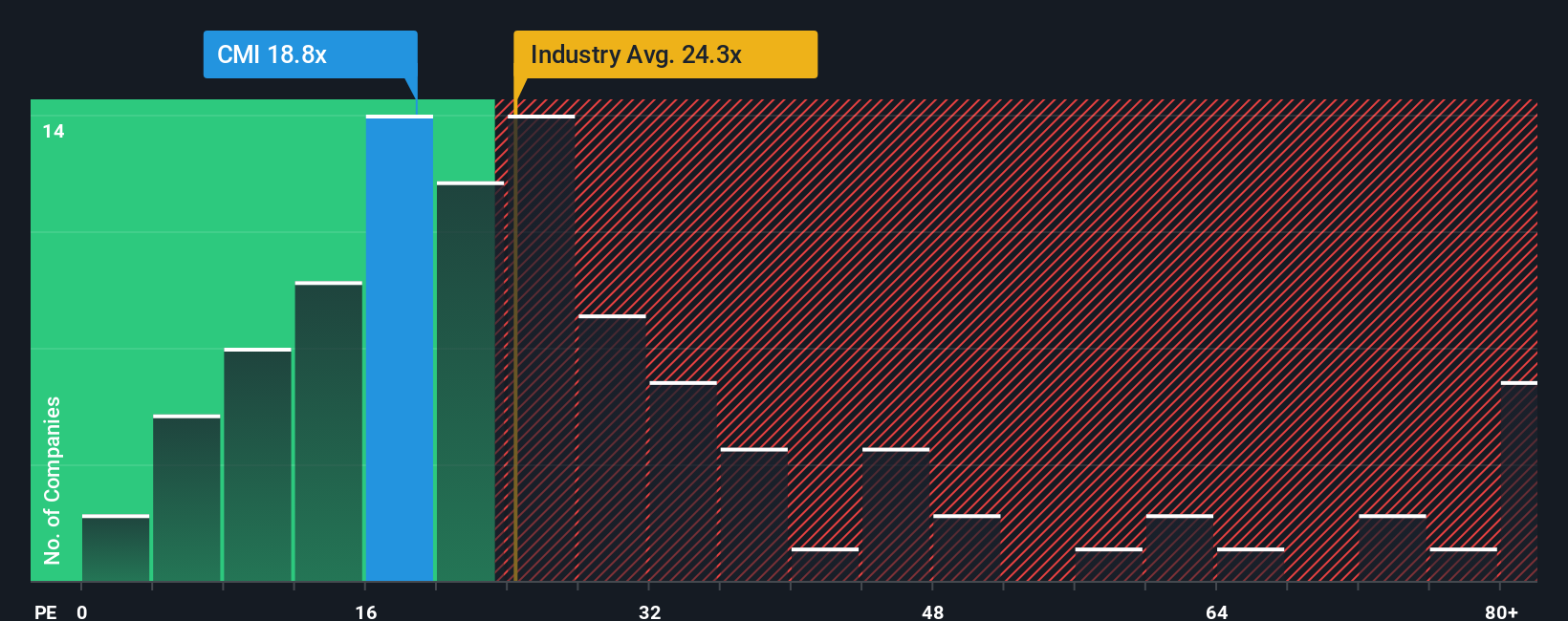

The earlier narrative leans on a fair value of $560.57 that leaves Cummins looking about 5% overvalued. Yet on simple earnings terms, the picture flips. At a P/E of 28.6x versus a fair ratio of 38.8x, and slightly below both industry and peer averages, the market is actually paying a thinner premium for each dollar of profit. That gap can mean less room for error, or room for sentiment to catch up, depending on how you see Cummins’ earnings path.

Build Your Own Cummins Narrative

If you see the numbers differently or prefer to piece together your own view from the underlying data, you can build a fresh Cummins story in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Cummins.

Ready for more investment ideas?

If Cummins has sharpened your thinking, do not stop here. A few minutes with the right screeners could reveal opportunities you will not want to miss.

- Target potential value opportunities by scanning companies our screener flags as 55 high quality undervalued stocks before others pay attention.

- Prioritise resilience by focusing on companies highlighted in our 85 resilient stocks with low risk scores and see which names score well on overall risk.

- Hunt for underfollowed opportunities with our screener containing 23 high quality undiscovered gems that surface quality businesses many investors may still be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.