A Look At Custom Truck One Source (CTOS) Valuation After New Sourcewell Procurement Contract

Custom Truck One Source Inc CTOS | 0.00 |

Sourcewell contract opens new procurement channel

Custom Truck One Source (CTOS) has been awarded a cooperative purchasing contract through Sourcewell, giving more than 50,000 participating agencies a pre-vetted path to procure the company’s specialty trucks and equipment.

The Sourcewell contract headlines arrive as momentum in Custom Truck One Source's share price has been building, with a 90 day share price return of 33.8% and a year to date share price return of 65.17%. The 1 year total shareholder return sits at 122.79%, despite a 5 year total shareholder return that is down 11.62%.

If this procurement win has you thinking about longer term infrastructure themes, it could be a good moment to widen your search and check out 33 power grid technology and infrastructure stocks

With CTOS shares up strongly over the past year and trading at a discount of about 20% to the current analyst price target of US$11.50, the key question is whether this contract win still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 25% Overvalued

At a last close of $9.58 versus a narrative fair value of $7.67, the most followed view sees Custom Truck One Source trading ahead of its modeled worth, anchored on a detailed set of growth and profitability assumptions.

Analysts are assuming Custom Truck One Source's revenue will grow by 4.3% annually over the next 3 years. Analysts assume that profit margins will increase from 1.6% today to 1.7% in 3 years time.

Want to see what sits behind that modest growth, small margin shift and still elevated earnings multiple? The narrative leans on a long runway of grid spending, improving cash generation and a valuation tied to earnings that only just turn positive. The tension between those inputs is what really shapes that $7.67 fair value call.

Result: Fair Value of $7.67 (OVERVALUED)

However, this narrative could be knocked off course if the relatively high net leverage or ongoing margin pressure in key segments limits the benefit of new contracts.

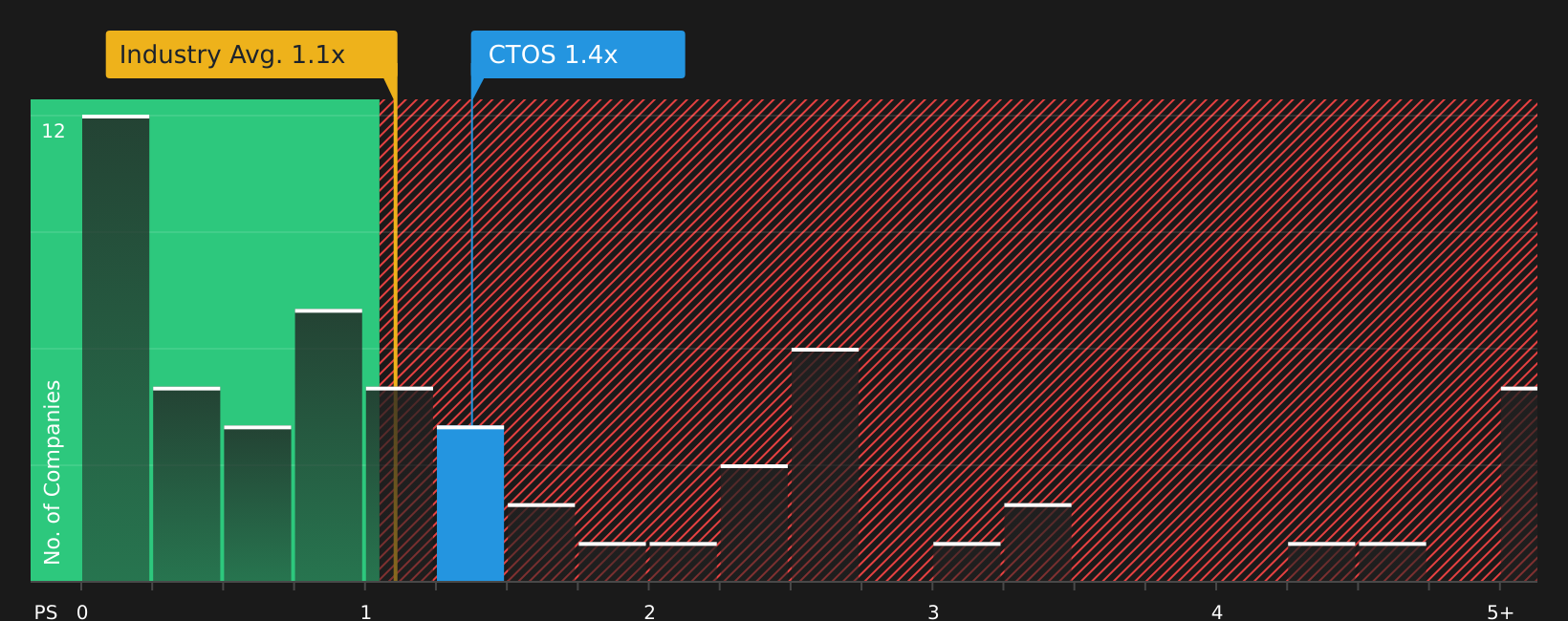

Another View: Multiples Paint A Calmer Picture

The narrative fair value of $7.67 suggests Custom Truck One Source is about 25% overvalued. However, its current P/S ratio of 1.1x lines up exactly with the US Trade Distributors average of 1.1x and sits below the peer average of 1.3x, while also matching the fair ratio of 1.2x closely enough that the market does not look stretched on this metric. This raises the question of whether the real risk is that expectations prove too low rather than too high.

Next Steps

With sentiment in the article pulling in different directions, this is a good time to check the underlying numbers yourself and decide how you feel about the setup. To see which potential upsides investors are focused on, review the 3 key rewards.

Looking for more investment ideas?

If you stop here, you only see one piece of the puzzle. Broaden your watchlist with a few focused stock ideas that match different portfolio goals.

- Target potential mispricing by scanning for companies that look attractively valued using the 45 high quality undervalued stocks.

- Strengthen your income stream by finding companies with robust yields and payout records through the 9 dividend fortresses.

- Prioritise resilience by focusing on companies with balance sheets that can better handle shocks via the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.