A Look At Custom Truck One Source (CTOS) Valuation After Q1 Results And Strong Recent Share Price Gains

Custom Truck One Source Inc CTOS | 0.00 |

Why Custom Truck One Source stock is back in focus

Custom Truck One Source (CTOS) is back on investors radars after reporting first quarter 2026 results, with higher sales, higher revenue, and a smaller net loss compared with a year earlier.

For the quarter ended March 31, 2026, the company reported sales of US$137.22 million versus US$116.26 million in the same period last year, and total revenue of US$461.62 million compared with US$422.23 million.

The business remained loss making, with a net loss of US$4.1 million versus US$17.79 million a year ago, and basic and diluted loss per share from continuing operations of US$0.02 compared with US$0.08 previously.

The earnings update appears to have caught the market’s attention, with an approximate 36% 1 month share price return and a 51% year to date share price return, alongside a 112% 1 year total shareholder return suggesting that momentum has been building.

If you are interested in other infrastructure related names benefiting from similar themes, it could be a good time to scan 33 power grid technology and infrastructure stocks

After a sharp 1 year total shareholder return of 112% and a recent 36% 1 month move, the key question is whether Custom Truck One Source’s 44% estimated intrinsic discount signals mispricing or if markets are already factoring in future growth.

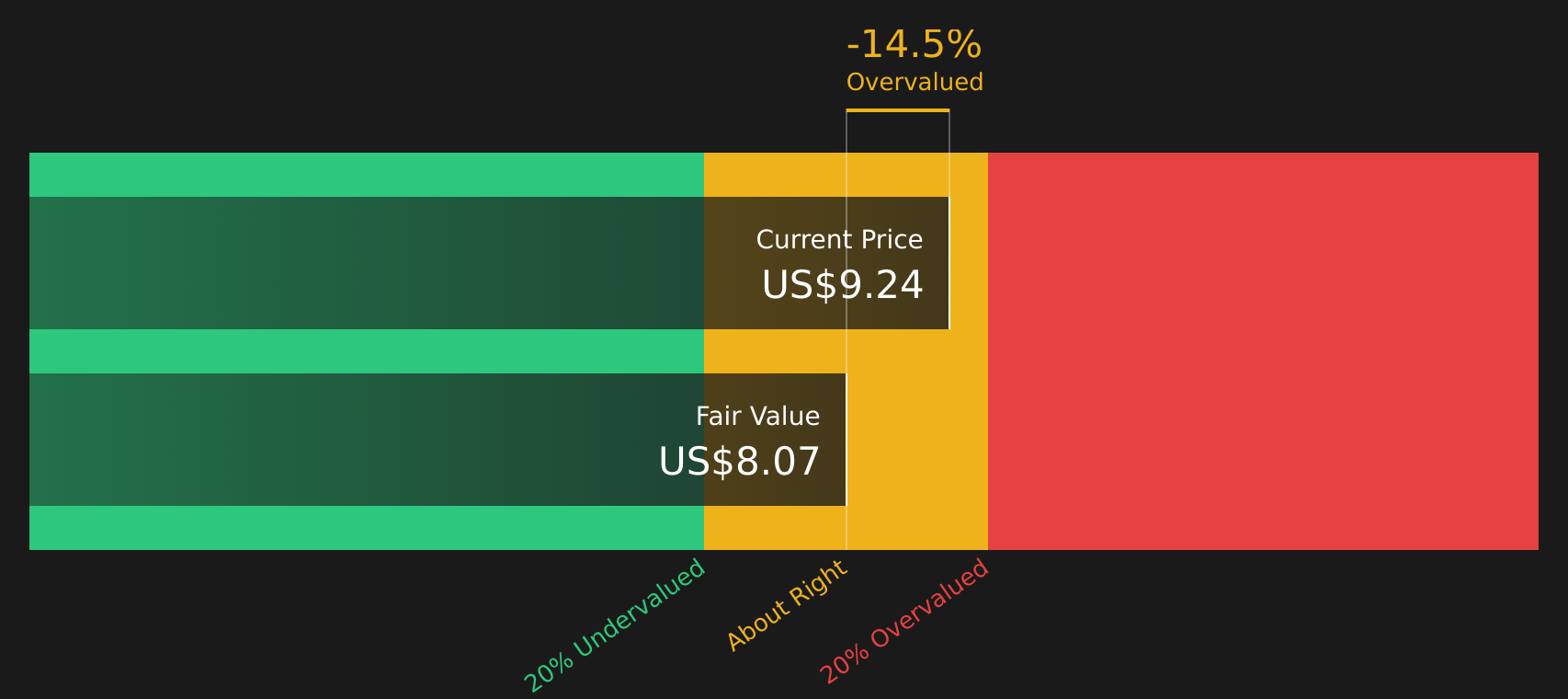

Most Popular Narrative: 14.5% Overvalued

Analysts see fair value for Custom Truck One Source at $7.67, which sits below the last close of $8.78 and frames a more cautious valuation story.

Analysts are assuming Custom Truck One Source's revenue will grow by 4.3% annually over the next 3 years.

Analysts assume that profit margins will increase from 1.6% today to 1.7% in 3 years time.

Want to see what is behind that tighter margin profile and steady revenue build? The key driver is how future earnings stack up against a much higher implied profit multiple and what that says about expectations baked into the fair value today.

Result: Fair Value of $7.67 (OVERVALUED)

However, there are still some watchpoints, including relatively high net leverage and pressure on gross margins if rental asset sales and demand mix move against expectations.

Another View: Cash Flows Point in the Opposite Direction

While analyst targets imply Custom Truck One Source is about 14.5% overvalued at $8.78 versus a $7.67 fair value, the Simply Wall St DCF model points the other way with an estimate of $15.60. That implies the current price trades at roughly a 44% discount to modelled future cash flows. Which signal do you put more weight on: cash flows or earnings multiples?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Custom Truck One Source for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The valuation signals in this update point in different directions, so now is a good time to review the details yourself and decide what matters most to you. To understand what the market already likes about Custom Truck One Source, take a closer look at its 2 key rewards

Looking for more investment ideas?

If Custom Truck One Source has your attention, do not stop here; there is a whole universe of other opportunities you can size up just as carefully.

- Target dependable income streams by scanning for companies with resilient payouts using the 12 dividend fortresses.

- Spot potential value opportunities early by running a search through the screener containing 25 high quality undiscovered gems.

- Prioritize capital preservation by focusing on companies flagged in the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.