A Look At Dollar General (DG) Valuation As UBS Sticks With Bullish Earnings And Margin Expansion Outlook

Dollar General Corporation DG | 119.26 119.26 | +3.05% 0.00% Pre |

Why Dollar General’s Boardroom Shuffle Matters for Shareholders

Dollar General (DG) just announced a leadership change at the top of its board, with David P. Rowland set to become chairman as investors weigh contrasting views on execution, earnings potential, and recent performance pressures.

Investors have already been reacting to Dollar General’s story, with a 46.1% 90 day share price return and a 106.8% 1 year total shareholder return, even though 3 and 5 year total shareholder returns remain negative and execution concerns persist.

If leadership changes and retail turnarounds are on your radar, it could be a good moment to widen the lens and check out 22 top founder-led companies.

With a recent 1 year total shareholder return above 100%, a value score of 1 and shares trading around a 17% intrinsic discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 5.3% Overvalued

Dollar General’s last close at $146.65 sits above the most followed fair value estimate of about $139.25. That estimate is built on detailed assumptions for growth, margins and valuation multiples over several years.

Remodeling efforts (Project Renovate and Project Elevate), along with expansion of higher margin nonconsumables and continued development of private label brands, are improving store productivity and encouraging higher basket sizes, helping to drive gross margin expansion and profitable earnings growth.

Curious what kind of revenue growth and margin rebuild are included in that $139 fair value, and what earnings power is used to support a higher future P/E? The full narrative lays out those levers in plain numbers and shows how they combine into that result.

Result: Fair Value of $139.25 (OVERVALUED)

However, there are still questions around rising labor costs and potential store oversaturation, either of which could pressure margins and challenge that earnings rebuild story.

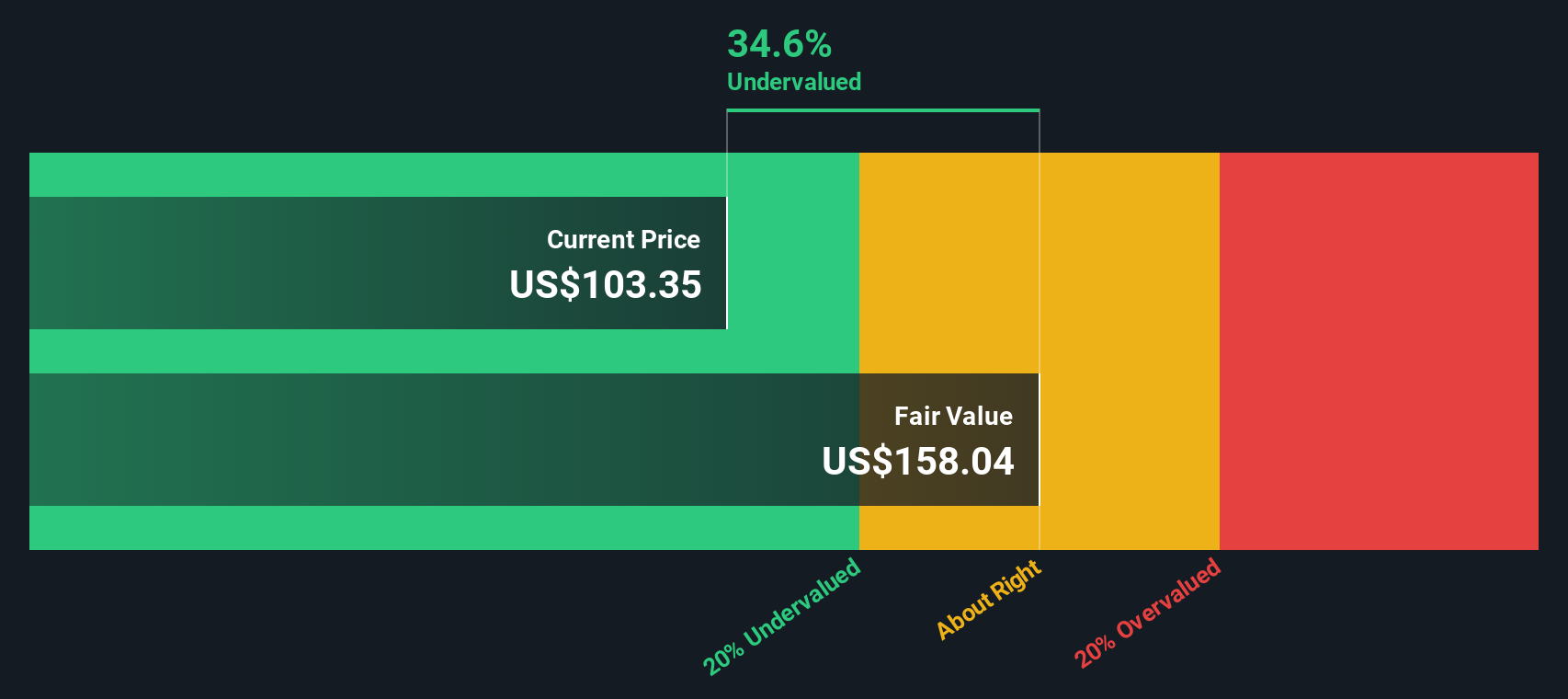

Another View: SWS DCF Flags Undervaluation

While the popular narrative points to Dollar General trading about 5.3% above its US$139.25 fair value estimate, our SWS DCF model tells a different story. It puts fair value closer to US$176.01 with shares around US$146.65, which implies the stock is trading at a 16.7% discount.

That kind of gap between a narrative driven fair value and a cash flow based estimate raises a simple question for you as an investor: which set of assumptions about margins and growth feels more realistic over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dollar General for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Dollar General Narrative

If you are not fully aligned with these views or just want to test your own assumptions against the data, you can quickly build a custom story for Dollar General, compare scenarios and see how your conclusions stack up with Do it your way

A great starting point for your Dollar General research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Dollar General has sharpened your focus, do not stop here. New opportunities often sit just outside your current watchlist, ready for a closer look.

- Target potential mispricings by reviewing companies our screener flags as 52 high quality undervalued stocks with solid fundamentals backing up their current pricing.

- Prioritise resilience first and check out 82 resilient stocks with low risk scores that may offer a steadier profile when you want to limit surprises.

- Hunt for lesser known opportunities by scanning our screener containing 24 high quality undiscovered gems that combine quality metrics with relatively low market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.