A Look At Dyne Therapeutics (DYN) Valuation After New CNS Tauopathy Data And Pipeline Expansion Potential

Dyne Therapeutics Inc DYN | 0.00 |

Why Dyne’s latest CNS data matters for DYN stock

Dyne Therapeutics (DYN) recently announced new preclinical data on its FORCE platform, showing MAPT RNA knockdown in the central nervous system. This places potential tauopathy applications alongside its existing neuromuscular focus.

For you as an investor, this update is less about near term revenue and more about how Dyne’s technology might support a broader pipeline over time, including Alzheimer’s related programs.

Despite the preclinical CNS update, Dyne’s share price return over the past 90 days is 4.4% and the year-to-date share price return is a 5.2% decline, while the 1-year total shareholder return of 55.3% points to stronger longer term momentum.

If this CNS progress has you thinking about other health focused opportunities, it could be worth scanning 35 healthcare AI stocks

With Dyne’s CNS progress, a US$3.1b market cap, and a share price at US$17.54 against a higher analyst target, you have to ask: Is this pipeline expansion underappreciated, or is the market already pricing in future growth?

Preferred Price to Book of 3x: Is it justified?

On a P/B of 3x, Dyne Therapeutics trades at a premium to the broader US Biotechs industry but at a steep discount to its closer peer group.

The P/B ratio compares the company’s market value to its book value, which is essentially net assets on the balance sheet. For pre revenue and loss making biotechs like Dyne, earnings based multiples such as P/E are not usable, so P/B often becomes a quick way for investors to compare how the market is valuing the underlying asset base and R&D platform.

Here, Dyne looks expensive against the wider US Biotechs industry average P/B of 2.5x. This suggests the market is assigning a higher valuation multiple than the typical biotech peer. However, when you narrow the lens to a more specific peer set, Dyne’s 3x P/B sits well below a peer average of 8.1x. This indicates the stock trades at a much lower multiple than companies viewed as similar.

This split picture means some investors may see the higher multiple versus the broad industry as a sign that expectations around the FORCE platform and CNS pipeline are already reflected in the price. Others may focus on the discount to the 8.1x peer average and view it as room for the valuation multiple to move closer to those levels if Dyne executes on its programs.

Result: Price to book of 3x (ABOUT RIGHT)

However, there is still material risk that Dyne’s preclinical CNS work does not translate as expected, while ongoing net losses of US$446.214m keep financing needs front of mind.

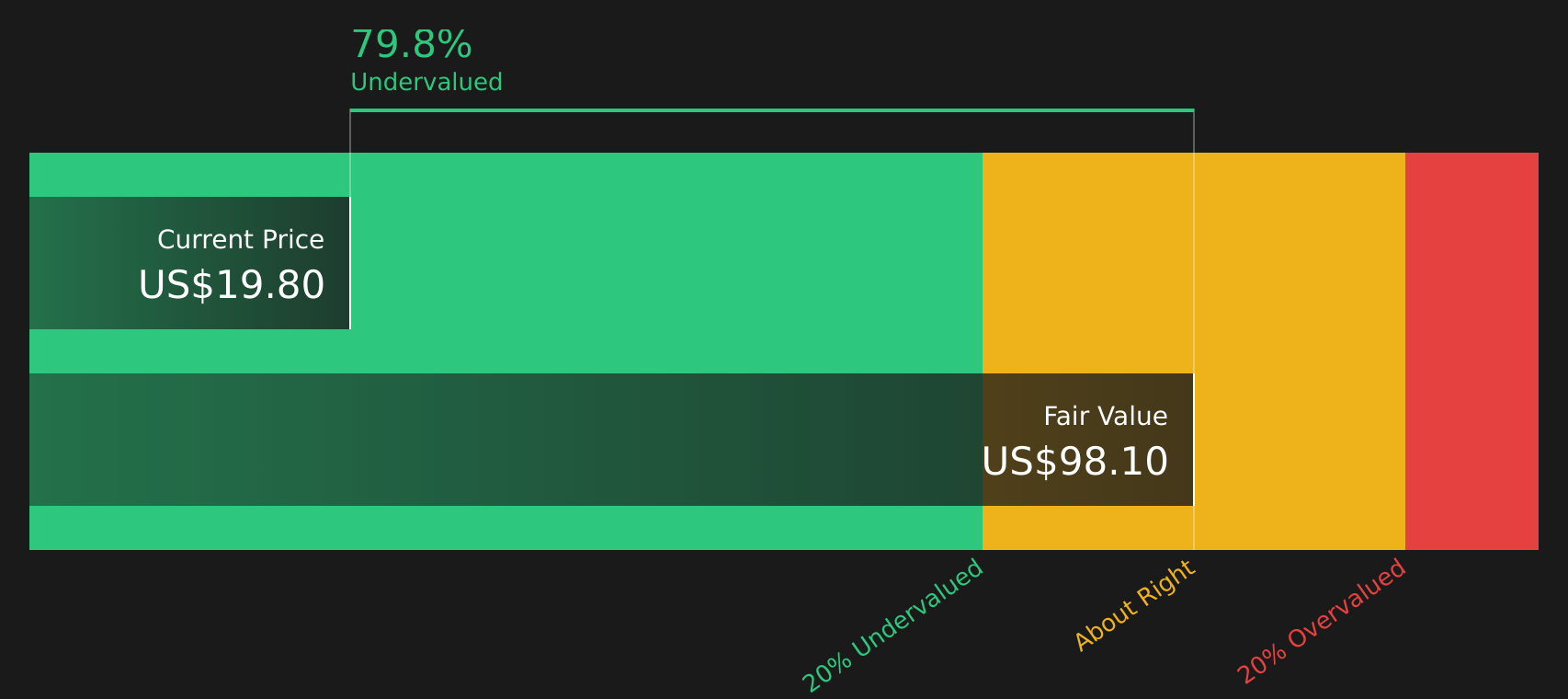

Another way to look at value

The P/B of 3x paints one picture, but the SWS DCF model gives a very different one. With Dyne trading at $17.54 versus an estimated future cash flow value of $128.34, the model presents the stock as heavily undervalued. Which view seems more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dyne Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation, risk, and reward, this is the moment to check the numbers yourself and decide how you feel about the balance of upside and downside. To help you weigh both sides of the story in one place, take a closer look at the 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If Dyne has your attention, do not stop here; broaden your watchlist with a few focused stock ideas that could sharpen your next investing move.

- Target potential bargains by scanning 51 high quality undervalued stocks that combine solid numbers with prices the market may be overlooking.

- Prioritise staying power with the solid balance sheet and fundamentals stocks screener (44 results) so you can focus on companies backed by resilient financial foundations.

- Hunt for tomorrow's potential standouts before they go mainstream by reviewing the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.