A Look At Fastenal’s (FAST) Valuation After Strong Q1 Results And New Logistics Expansion

Fastenal Company FAST | 0.00 |

Fresh earnings and expansion plans put Fastenal (FAST) in focus

Fastenal (NasdaqGS:FAST) just posted Q1 FY2026 results with net sales up 12.4% and net income up 13.8%, while also starting work on a new Southeast logistics center in Carrollton, Georgia.

The update provides new information on growth, margin pressures from tariffs, and how management is positioning the business for future industrial demand.

At a share price of US$44.36, Fastenal has seen a 7.1% decline in its 3 month share price return but a 9.7% share price gain year to date, alongside a 5 year total shareholder return of 87.9%. This suggests that longer term momentum remains intact despite recent softness.

If you are looking beyond industrial suppliers for the next potential opportunity, this could be a good moment to scan 36 power grid technology and infrastructure stocks

Fastenal now trades at US$44.36, following a recent 3 month pullback that contrasts with strong multi year returns and fresh double digit Q1 growth. Is the stock on sale today, or already pricing in its next leg of expansion?

Most Popular Narrative: 4.6% Undervalued

Fastenal's most followed narrative places fair value at US$46.49, a touch above the last close of US$44.36, which frames the Q1 update in a tighter valuation band.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains.

Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Want to see what happens when rising digital sales, richer margins, and a premium earnings multiple all get baked into one storyline? The key assumptions behind that US$46.49 figure rely on a specific revenue glide path, a modest step up in profitability, and a P/E that sits well above the broader trade distributor group.

Result: Fair Value of $46.49 (UNDERVALUED)

However, there is still the risk that trade tensions, tariffs and higher operating costs will pressure margins and make the current earnings path harder to deliver.

Another View On Valuation

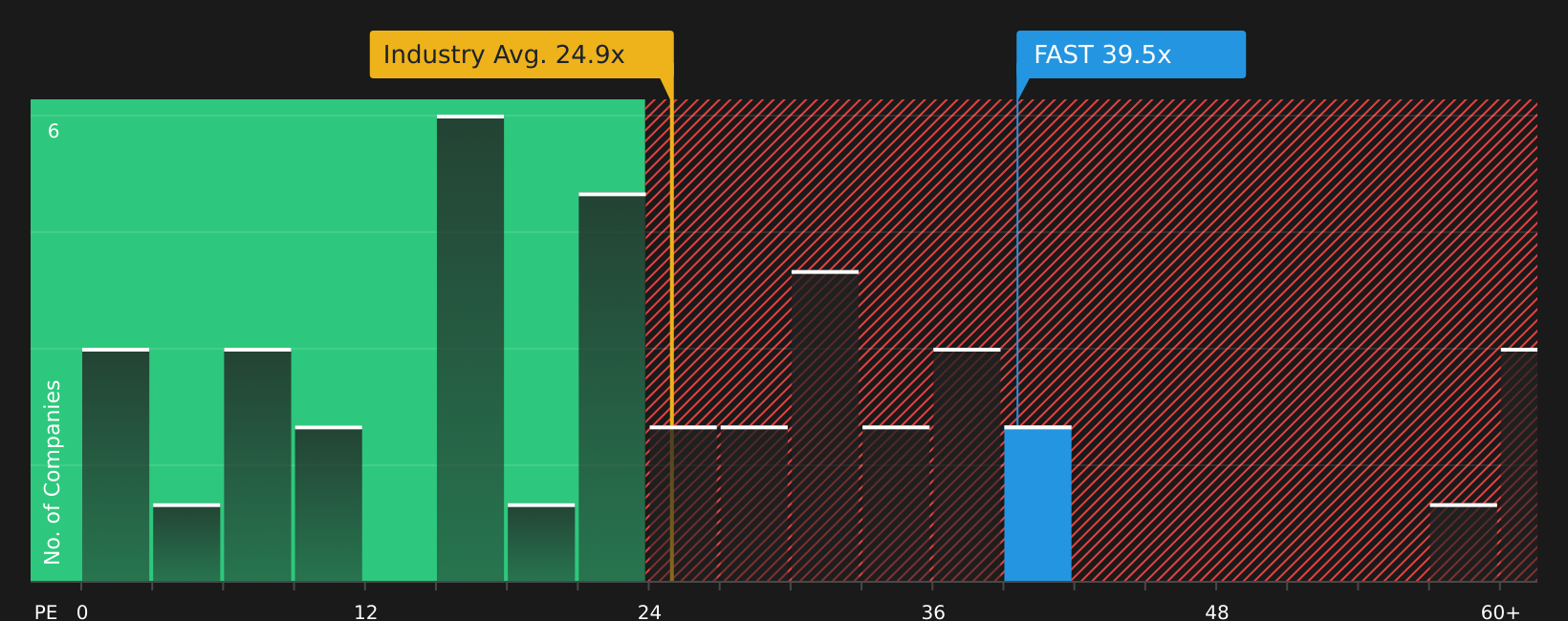

The analyst narrative points to Fastenal being 4.6% below a fair value of US$46.49, yet its 39.2x P/E is well above the US Trade Distributors average of 25.1x, a peer average of 24.6x and a fair ratio of 29.7x. This signals meaningful valuation risk if sentiment cools.

For a closer look at how this P/E gap could matter for your thesis, including what it might mean if the market shifts toward the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment in this article mixed between opportunity and concern, this may be a useful time to review the data yourself and test your thesis against 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Fastenal has sparked your interest, do not stop here. Use the Simply Wall St screener to uncover other stocks that might fit your goals just as well.

- Zero in on quality at a discount by scanning our list of 51 high quality undervalued stocks that combine strong fundamentals with pricing that may appeal to value focused investors.

- Strengthen your income toolkit by reviewing a hand picked set of 12 dividend fortresses that could complement or diversify beyond your current holdings.

- Dial back risk without stepping away from the market by checking out 71 resilient stocks with low risk scores that score well on resilience and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.