A Look At First Busey (BUSE) Valuation As Shares Trade On An 11x P/E And DCF Suggests Upside

First Busey Corporation BUSE | 0.00 |

Event context and recent price performance

First Busey (BUSE) shares have been relatively stable in the short term, edging up about 0.04% over the past day and around 0.2% over the past week, while sitting down roughly 2.9% for the month.

Looking beyond the recent softness in the share price, First Busey’s 9.7% year to date share price return and 21.4% 1 year total shareholder return point to momentum that has been building rather than fading.

If you are comparing First Busey with other financial opportunities, it can help to widen the lens and look at 19 top founder-led companies

With solid 1-year and 3-year total returns on the table, along with an indicated 48% intrinsic discount and growth in revenue and net income, is First Busey still undervalued, or is the market already pricing in its future growth?

Price-to-Earnings of 11x: Is it justified?

First Busey currently trades on a P/E of 11x, which, together with a 47.7% discount to an estimated fair value, points to a valuation that looks undemanding relative to its recent $26.21 close.

The P/E multiple compares the share price to earnings per share and is a common yardstick for banks, where steady profitability and dividends are central to the investment case. With earnings forecast to grow 6.3% per year and revenue growth expectations at 3% per year, the current P/E indicates the market is not pricing in especially aggressive profit expansion.

Against peers, the picture is quite restrained. First Busey’s 11x P/E is below the peer average of 13.3x and slightly below the US Banks industry average of 11.2x, while still lining up closely with an estimated fair P/E of 11.3x that the market could move towards if current assumptions hold. On top of that, the SWS DCF model suggests the stock, at $26.21, trades below an estimated future cash flow value of $50.07, which indicates that the current earnings multiple sits at the lower end of what the company’s cash flow profile might support over time.

Result: Price-to-Earnings of 11x (UNDERVALUED)

However, this hinges on steady credit quality and earnings, and any reset in analyst expectations for the US$28.57 price target could challenge the current valuation story.

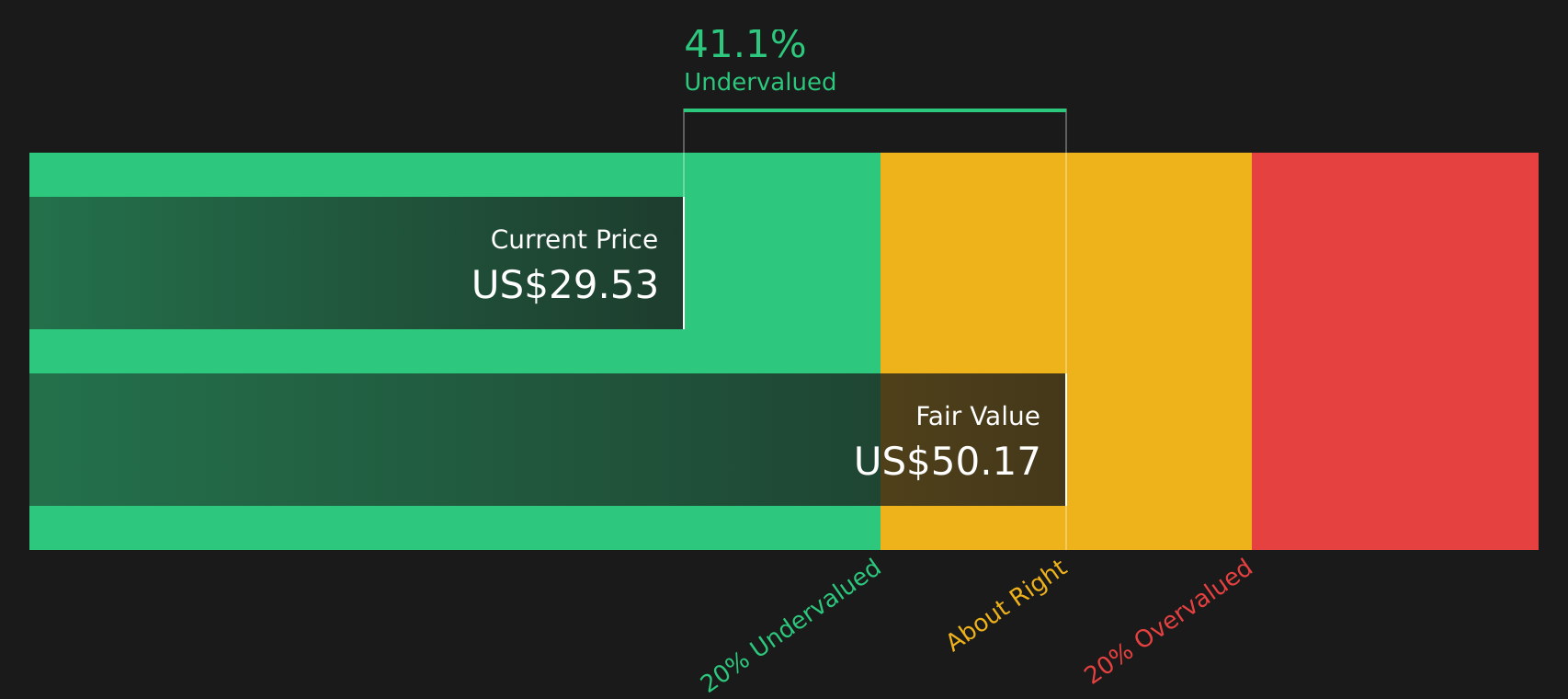

Another angle on value: DCF fair value gap

The SWS DCF model values First Busey at $50.07 per share, compared with the current $26.21 price. This implies the stock trades at a very wide discount to estimated future cash flows. That is a large gap, so it raises a simple question: are the cash flow assumptions too cautious or too generous?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First Busey for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of potential upside and valuation questions has your attention, move quickly to check the details and form your own view by reviewing the 5 key rewards.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock. Widen your search with focused stock ideas built from clear data.

- Target potential mispricing by checking companies that screen as 54 high quality undervalued stocks before the crowd fully pays attention.

- Strengthen your income stream by reviewing 12 dividend fortresses that aim to pair yield with resilience.

- Protect your downside by filtering for 66 resilient stocks with low risk scores that prioritise financial strength and consistency.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.