A Look At FTAI Aviation (FTAI) Valuation After Crossroads Capital Highlights Capital Light Engine Platform

FTAI Aviation Ltd. FTAI | 0.00 |

FTAI Aviation (FTAI) is back in focus after Crossroads Capital LLC highlighted the stock, pointing to its shift toward a capital-light, higher-visibility model built around PMA parts and a vertically integrated engine platform.

FTAI Aviation's latest focus from Crossroads Capital and its upcoming redemption of Series C preferred shares sit against a backdrop of strong momentum, with the share price up 24.93% year to date and a very large 1 year total shareholder return and multi year total shareholder returns, suggesting investors are reassessing both growth prospects and risk.

If this shift in sentiment around FTAI Aviation has caught your eye, it could be a good moment to see what else is moving in aviation related infrastructure and 33 power grid technology and infrastructure stocks

With FTAI Aviation trading at US$262.78, sitting at a reported 23% discount to an intrinsic value estimate and roughly 33% below one analyst price target, investors may ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 16.8% Overvalued

According to kapirey, the most followed narrative puts FTAI Aviation's fair value at $225.05, below the last close of $262.78, which creates a clear value gap for investors to weigh.

FTAI Aviation is not a traditional aircraft lessor, it is evolving into a hybrid aerospace infrastructure and aftermarket platform.

Strengths: structural tailwinds, integrated model, aftermarket margins. Weaknesses: leverage, concentration, execution complexity. Key risk: dependence on aging fleet economics holding longer than expected.

FTAI's fair value hinges on a detailed view of how fast aerospace products can scale, how margins hold up and what earnings multiple that mix can support. The narrative connects revenue growth, profitability and capital intensity in a specific way that the current share price does not fully mirror on the surface.

Result: Fair Value of $225.05 (OVERVALUED)

However, this story can break if heavy leverage starts to bite, or if reliance on aging CFM56 and V2500 engines weakens faster than investors expect.

Another View: P/E Ratios Point the Other Way

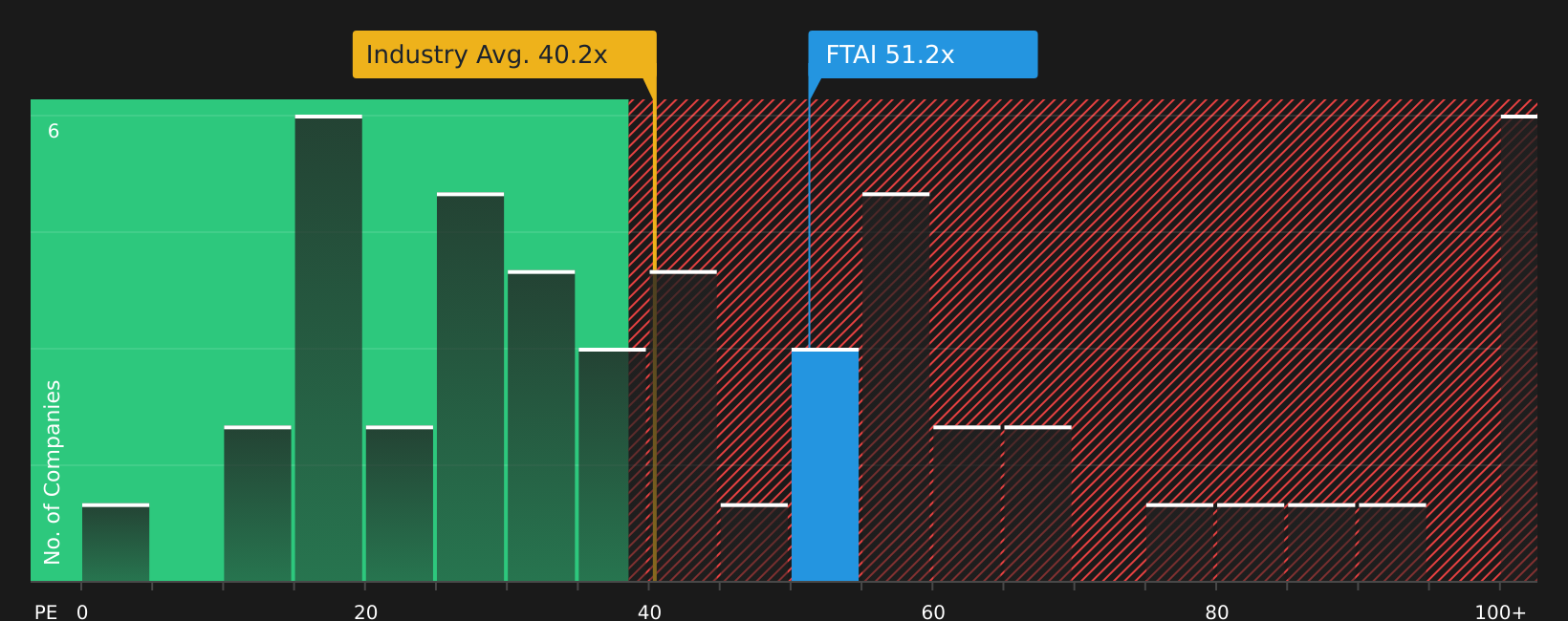

The most followed narrative sees FTAI Aviation as 16.8% overvalued at $262.78, yet the current P/E of 51.7x sits below a fair ratio of 59.7x and under a peer average of 58.9x. If earnings track forecasts, does this gap signal valuation risk shrinking or building?

Next Steps

With sentiment split between risks and rewards, this is a moment to look at the numbers yourself, weigh both sides, and act on your own judgment using 4 key rewards and 3 important warning signs

Looking for more investment ideas?

If FTAI Aviation has sharpened your focus, do not stop here. Widen your radar with other stocks that match clear, data driven criteria and stay ahead.

- Target potential value opportunities by scanning 46 high quality undervalued stocks that currently combine quality metrics with pricing below intrinsic estimates.

- Prioritize resilience by reviewing 64 resilient stocks with low risk scores that score well on risk factors and may suit a steadier approach.

- Hunt for lesser known opportunities by checking the screener containing 22 high quality undiscovered gems that still sit off many investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.