A Look At Genesis Energy (GEL) Valuation After Raising Quarterly Cash Distributions

Genesis Energy, L.P. GEL | 17.60 | +0.57% |

Genesis Energy (GEL) drew investor attention after its board declared new quarterly cash distributions, including an increased payout of $0.18 per common unit and $0.9473 per preferred unit, tied to the December 31, 2025 quarter.

The latest distribution decision comes as Genesis Energy’s unit price has moved to US$16.81, with a 7.83% 1 month share price return and a 5.86% year to date share price return. The 1 year total shareholder return of 70.11% and 5 year total shareholder return of 249.92% point to momentum that has built over a longer period.

If this kind of income story has your attention, it could be a useful moment to broaden your search and check out pharma stocks with solid dividends as another source of dividend ideas.

With Genesis Energy trading at US$16.81, while sitting at a discount to one analyst price target and carrying a relatively high intrinsic discount, you have to ask: is there still value on the table, or is the market already pricing in future growth?

Preferred Price-to-Sales of 0.7x: Is it justified?

On the numbers provided, Genesis Energy trades on a P/S of 0.7x, which looks low next to both peers and the wider US oil and gas group.

The P/S ratio compares the market value of the business to its revenue. It therefore avoids the noise of current losses and focuses on how much investors are paying for each dollar of sales. For a midstream partnership that is currently unprofitable, revenue-based measures often become a common yardstick.

Here, Genesis Energy screens as good value against its peer set, with its 0.7x P/S sitting well below the peer average of 2.3x and the US oil and gas industry average of 1.6x. However, that same 0.7x multiple sits above the estimated fair P/S of 0.3x. This suggests the market is already paying more than the level our fair ratio points to as a potential anchor.

Result: Price-to-Sales of 0.7x (ABOUT RIGHT)

However, you still need to weigh risks such as the annual revenue contraction of 37.65% and a net loss of US$160.474m, which could challenge the current valuation narrative.

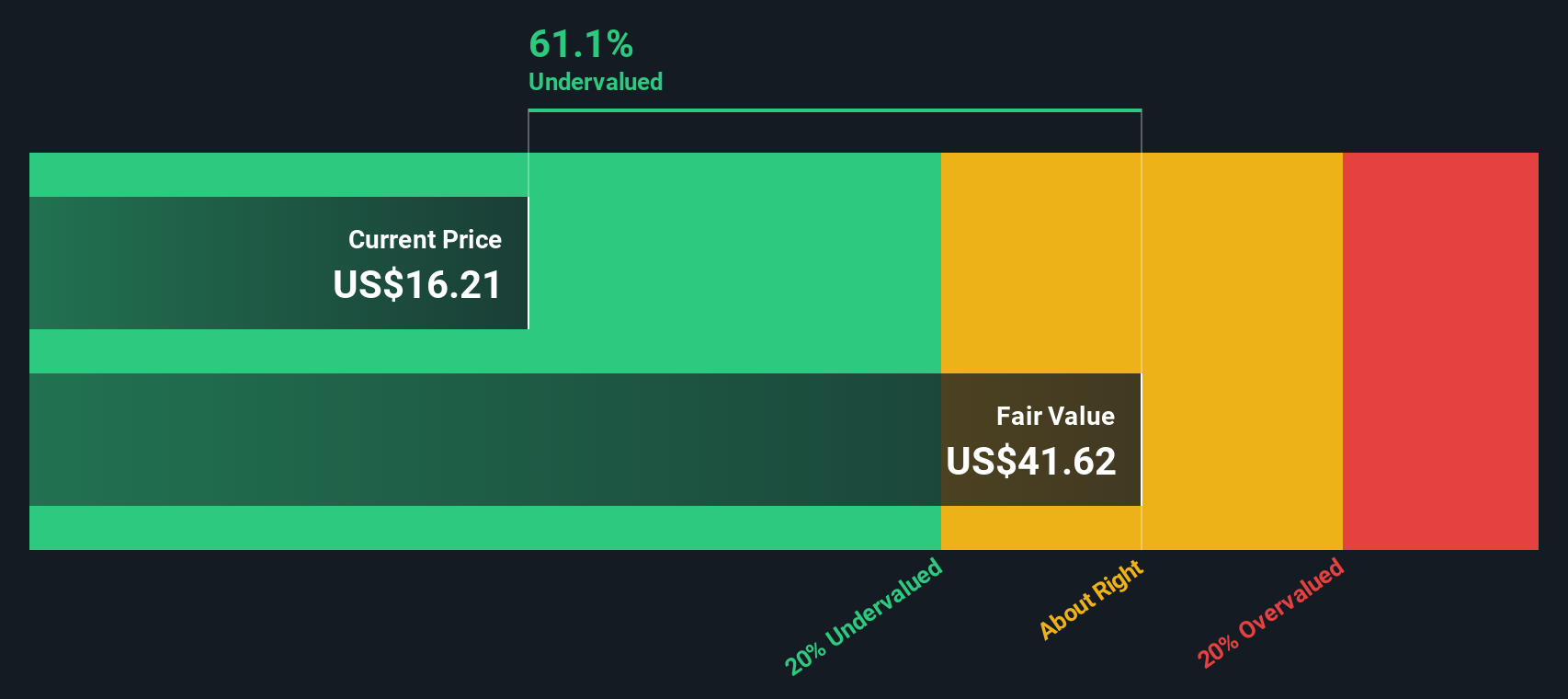

Another View: SWS DCF Flags Deep Undervaluation

While the 0.7x P/S ratio hints at relatively low expectations, our DCF model goes much further. It puts Genesis Energy’s value at $48.95 per unit versus the current $16.81 price, implying a very large gap. Is the market skeptical for good reasons, or simply cautious?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 888 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Genesis Energy Narrative

If you look at these numbers and reach a different conclusion, or prefer to test the inputs yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Genesis Energy research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Genesis Energy has you thinking bigger about your portfolio, do not stop here, widen your search now so you are not leaving potential ideas on the table.

- Target potential mispricings by scanning these 888 undervalued stocks based on cash flows, where cash flow focused filters can help you spot opportunities others might overlook.

- Consider broader themes in digital assets by checking out these 19 cryptocurrency and blockchain stocks, which highlights listed businesses tied to cryptocurrencies and blockchain activity.

- Build a cash flow focused income list with these 13 dividend stocks with yields > 3%, concentrating on companies offering dividend yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.