A Look At GXO Logistics (GXO) Valuation After New BAE Systems And London Luton Airport Contracts

GXO Logistics Inc GXO | 53.08 | -0.75% |

GXO Logistics (GXO) is back on investor radars after renewing and expanding its UK contract with BAE Systems. The six year deal extends a shipbuilding logistics partnership now entering its third decade.

The contract wins with BAE Systems and London Luton Airport have coincided with a 12.49% 90 day share price return and a 36.81% total shareholder return over the past year, suggesting momentum has picked up recently from both short and longer term perspectives.

If this kind of logistics contract flow has your attention, it could be a good moment to widen your search and check out our 22 top founder-led companies as potential next ideas.

GXO is trading close to some estimates of intrinsic value and sits at a small discount to analyst targets. The key question is whether recent contract wins leave upside on the table or if markets are already pricing in future growth.

Most Popular Narrative: 10.7% Undervalued

GXO Logistics' last close at $58.91 sits below the most followed fair value estimate of $66.00, putting extra focus on what is built into that target.

The company's focus on long term, multi year, blue chip customer contracts, coupled with record levels of new business wins and high customer retention (mid 90s%), underpins resilient and stable cash flows, reducing earnings volatility and providing a strong foundation for future capital returns and reinvestment.

Curious what kind of revenue path, margin lift, and future earnings multiple are being assumed to reach that fair value? The full narrative spells out the cash flow story behind the model. It also shows how those longer term contracts feed into the discount rate and growth runway.

Result: Fair Value of $66.00 (UNDERVALUED)

However, there is still real execution risk around integrating Wincanton smoothly and delivering the expected automation benefits, without squeezing margins or disrupting customer relationships.

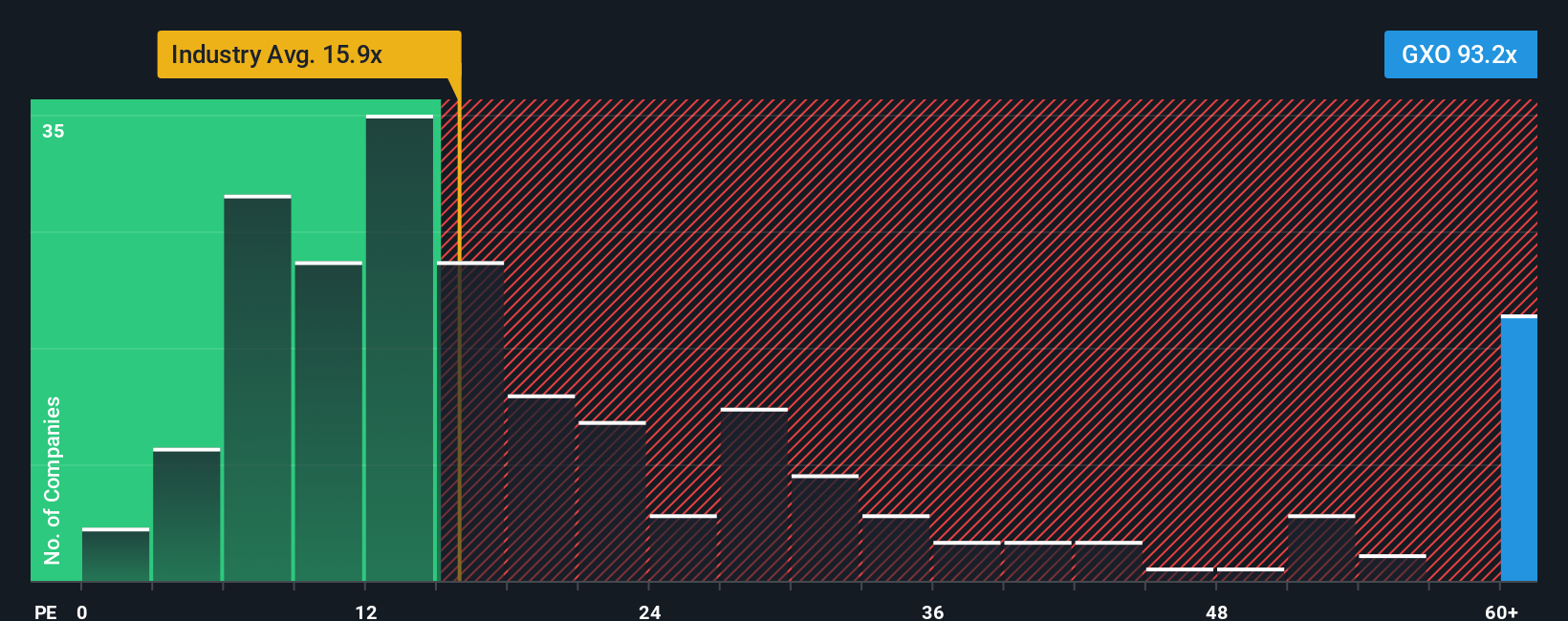

Another View: Multiples Paint A Tougher Picture

Our cash flow work points to GXO trading around fair value, with the share price just 0.5% below the SWS DCF model estimate. However, the earnings multiple tells a different story, with a P/E of 75.8x versus a fair ratio of 49.7x, the global logistics average at 16.5x and peers at 26.4x. That gap raises a simple question for you: are you comfortable paying up for this profile today, or would you rather wait for expectations to cool?

Build Your Own GXO Logistics Narrative

If your view on GXO differs from this or you simply prefer to work from your own numbers, you can build a complete story in just a few minutes, starting with Do it your way.

A great starting point for your GXO Logistics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop your research with just one company. Broaden your watchlist using focused stock ideas so you keep seeing fresh opportunities instead of the same tickers.

- Target value first and scan our list of 52 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience and review a group of 84 resilient stocks with low risk scores that score well on our risk checks and may suit a steadier portfolio core.

- Hunt for future standouts with our screener containing 24 high quality undiscovered gems picked from companies that attract less attention but pass solid fundamental filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.