A Look At Huntington Ingalls Industries (HII) Valuation After Major Defense Wins And USS Zumwalt Milestone

Huntington Ingalls Industries, Inc. HII | 396.62 | +0.84% |

Huntington Ingalls Industries (HII) is in focus after its Mission Technologies division secured spots on major U.S. Department of Defense contracts, and the company completed builder sea trials for the modernized USS Zumwalt destroyer.

Those contract wins and shipbuilding milestones come after a strong run in the share price, with a 30 day share price return of 19.21% and a 90 day gain of 38.75%. The 1 year total shareholder return of 111.32% suggests momentum has been strong over both shorter and longer periods, despite a recent 1 day share price decline of 1.31% and a 7 day pullback of 1.72%, at a last close of US$418.58.

If this kind of defense activity has your attention, it could be a good moment to see what else is moving among aerospace and defense stocks.

With the shares at US$418.58, slightly above the average analyst price target of US$380.60 but showing an estimated 9.50% intrinsic discount, you have to ask: is HII still mispriced, or is the market already banking on future growth?

Most Popular Narrative: 10% Overvalued

Compared with the most followed narrative fair value of $380.60, HII's last close at $418.58 sits above that mark, which raises questions about what assumptions are baked into that gap.

The analysts have a consensus price target of $285.8 for Huntington Ingalls Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $324.0, and the most bearish reporting a price target of just $221.0.

It is noteworthy that a higher fair value still lines up with a lower analyst target range. Revenue, margins, and a future earnings multiple all do the heavy lifting. The key question is which specific profit and growth paths would justify that valuation gap.

Result: Fair Value of $380.60 (OVERVALUED)

However, the story can change quickly if major Navy contracts slip further or if political budget debates lead to tighter shipbuilding funding than the market currently expects.

Another View: Earnings Multiple Tells A Different Story

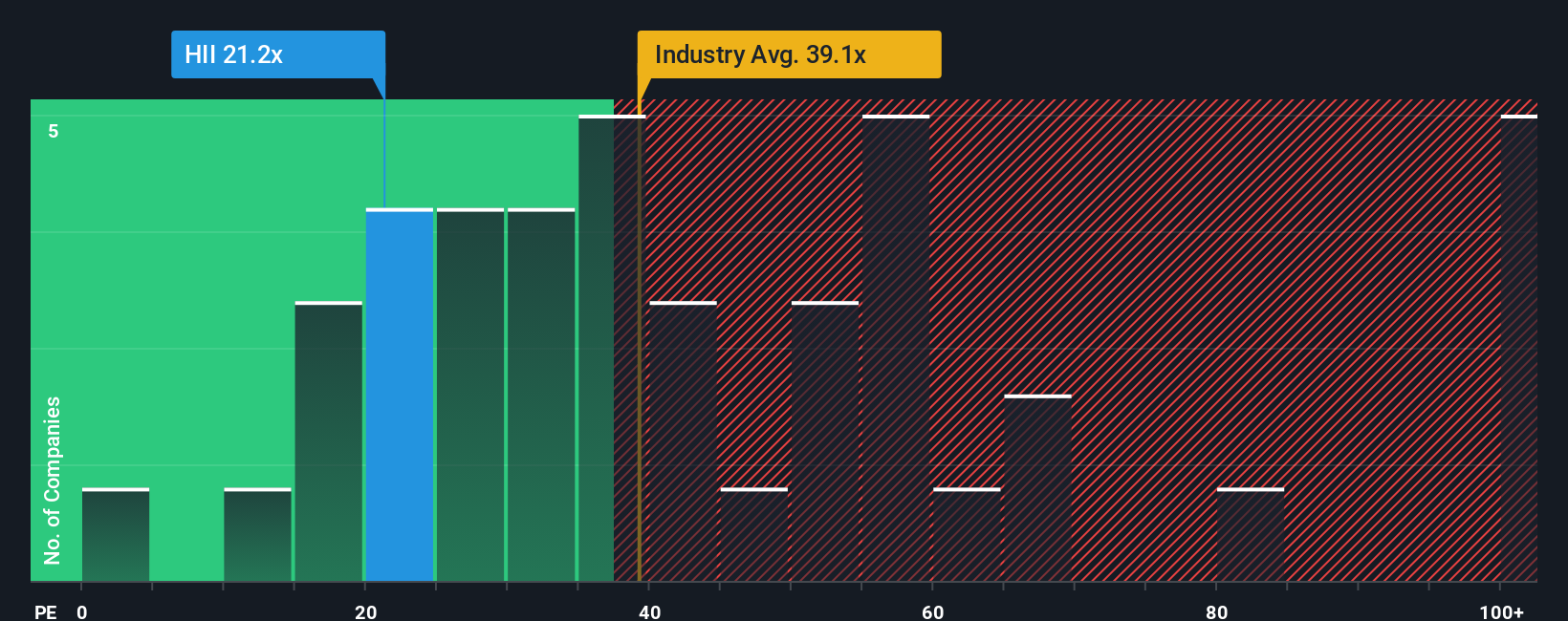

If you step away from fair value models and just look at what investors are paying for earnings, HII trades on a P/E of 28.9x, compared with 41.1x for the US Aerospace & Defense industry and 40.1x for peers, yet slightly above its own 27.3x fair ratio.

So you have a company that screens cheaper than its sector on P/E, but a touch expensive versus its fair ratio. This hints at some valuation risk if sentiment cools, or potential support if the wider group stays richly priced. Which side of that trade do you think the market leans toward?

Build Your Own Huntington Ingalls Industries Narrative

If you see the numbers differently or want to test your own assumptions, you can build a tailored view of HII in just a few minutes with Do it your way.

A great starting point for your Huntington Ingalls Industries research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If HII has sharpened your appetite for opportunities, do not stop here, the screener can quickly surface other stocks that might better fit your style and risk comfort.

- Target growing income potential by checking out these 13 dividend stocks with yields > 3% that might complement a portfolio focused on regular cash returns.

- Tap into potential growth themes with these 23 AI penny stocks that are tied to ongoing advances in artificial intelligence and automation.

- Hunt for possible mispricings using these 872 undervalued stocks based on cash flows that currently trade at discounts based on their estimated cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.