A Look At Las Vegas Sands (LVS) Valuation After Q4 2025 Beat And Macau Margin Concerns

Las Vegas Sands Corp. LVS | 56.51 | +0.44% |

Las Vegas Sands (LVS) just reported its Q4 2025 results, with revenue of US$3,649 million and net income of US$395 million. The stock sold off as investors focused on weaker Macau margins.

At a share price of US$56.94, Las Vegas Sands has seen recent momentum cool, with a 30 day share price return of 10.72% and a 90 day share price return of 12.68%, even as the 1 year total shareholder return sits at 37.43%. Recent pressure has been tied to weaker Macau margins and cautious commentary on Chinese consumer spending. The long term total shareholder return over three and five years of 3.68% and 8.43% suggests a more measured payoff for patient holders.

If you are reassessing casino names after these earnings, it could be a good moment to broaden your search and check out 22 top founder-led companies as potential new ideas.

So with earnings ahead of expectations but Macau margins under pressure, and the share price pulling back after a strong 1 year return, is Las Vegas Sands now on sale, or is the market already pricing in its future growth?

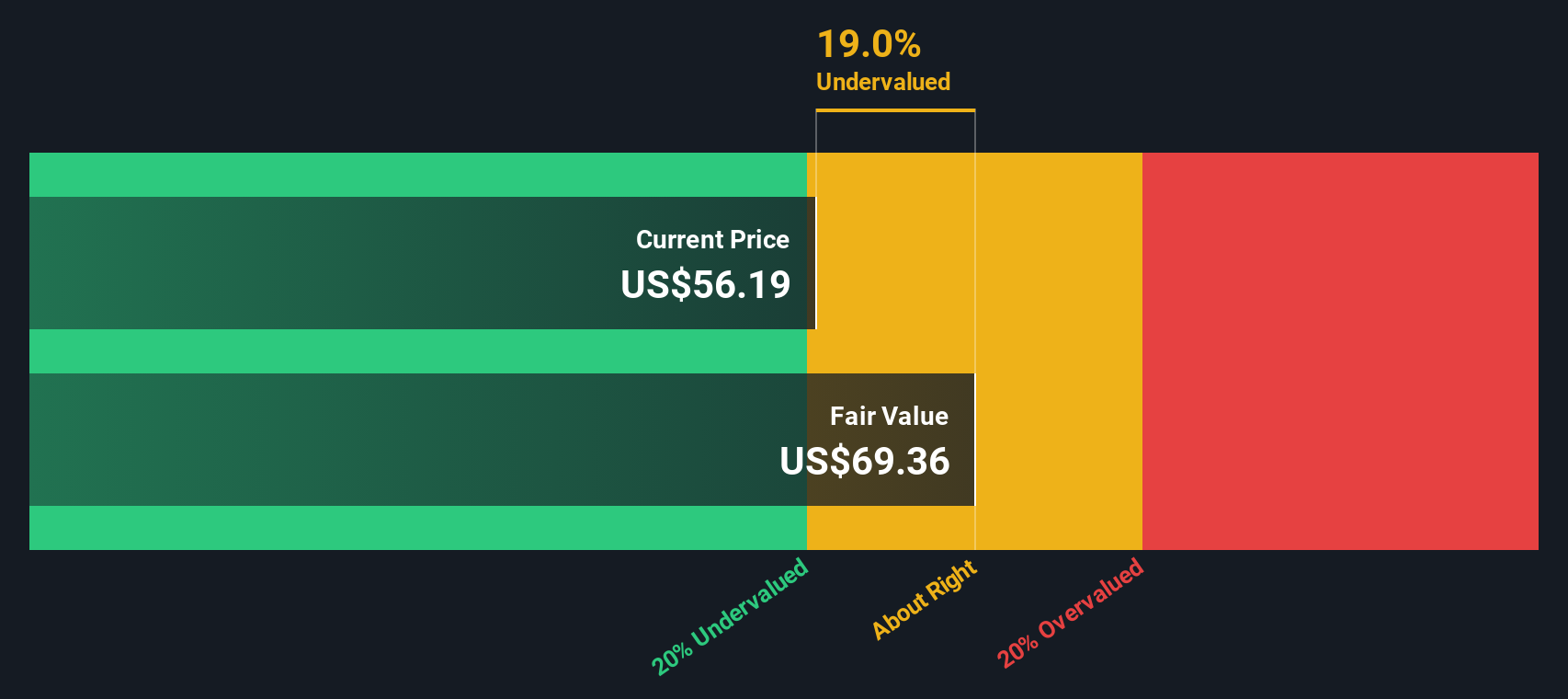

Most Popular Narrative: 13.5% Undervalued

At $56.94, the most followed narrative sees Las Vegas Sands trading below an estimated fair value of $65.85, with that gap hinging on Macau and Singapore execution under a 9.16% discount rate.

The full opening and ramp-up of The Londoner in Macao, with its 2,405 rooms and suites, is expected to boost revenues and cash flows significantly as the property leverages its scale and quality in a competitive market. Marina Bay Sands (MBS) in Singapore reported record EBITDA from high-value tourism and is expected to continue its growth trajectory supported by increased visitor capacity post-renovations, directly impacting revenue and EBITDA growth.

One question is what kind of revenue path and margin profile would justify that fair value gap. The widely followed narrative focuses on specific earnings targets, buybacks and a lower future P/E than today. The exact mix of growth, profitability and discounting may differ from what some investors anticipate.

Result: Fair Value of $65.85 (UNDERVALUED)

However, lingering Macau recovery risks and limits on new markets like New York could challenge revenue growth and pressure the earnings path behind that 13.5% undervaluation story.

Another Angle on Valuation

The fair value narrative points to a 13.5% undervaluation for Las Vegas Sands at $56.94, yet our DCF model paints a different picture. On that view, the shares sit above an estimated future cash flow value of $42.04, which frames the stock as overvalued instead. Which story do you find more convincing?

Build Your Own Las Vegas Sands Narrative

If you are not fully on board with these narratives or simply prefer to weigh the numbers yourself, you can build a fresh view in just a few minutes with Do it your way.

A great starting point for your Las Vegas Sands research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Las Vegas Sands has sparked fresh thinking about your portfolio, do not stop here. The broader market is full of opportunities that could fit your goals.

- Spot potential bargains early by reviewing our list of 55 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Strengthen your income stream by checking out 15 dividend fortresses, focused on companies offering higher yields with an emphasis on resilience.

- Sleep a little easier by considering 81 resilient stocks with low risk scores, highlighting businesses that score well on our risk metrics and financial checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.