A Look At Life Time Group Holdings (LTH) Valuation After Fresh 2025 And 2026 Earnings Guidance

Life Time Group Holdings, Inc. LTH | 26.99 | +3.37% |

Fresh guidance gives investors clearer guardrails

Life Time Group Holdings (LTH) recently issued earnings guidance for the fourth quarter of 2025 and the full years 2025 and 2026, giving investors fresh revenue and profit ranges to anchor expectations.

The company outlined projected Q4 2025 revenue of about $743 million to $745 million, with net income of $120 million to $123 million, alongside updated full year views that extend into 2026.

The guidance appears to come as momentum in Life Time Group Holdings' share price has been building, with an 18.27% 3 month share price return and an 11.09% year to date share price return, contrasting with a 2.79% decline in 1 year total shareholder return and a 55.48% gain in 3 year total shareholder return.

If this earnings update has you reassessing your watchlist, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Life Time guiding to higher revenue and solid net income ranges, a 3 year total return of 55.48% and the shares trading at a discount to the average analyst target, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 26.5% Undervalued

At a last close of $29.65 versus a narrative fair value of $40.36, the widely followed view sees meaningful upside potential anchored to specific growth and margin assumptions.

The expanding pipeline of new and larger club openings in affluent and high-density markets positions Life Time for sustained membership and top-line revenue growth, benefiting from the growing consumer demand for premium health, wellness, and lifestyle experiences.

Curious what kind of revenue growth and margin profile has to play out for that to hold, and what sort of future earnings multiple underpins it? The full narrative spells out those projections in detail and sets clear expectations for how fast earnings may need to grow, how profitable the business may need to become, and what valuation the market may be willing to pay for that story to line up.

Result: Fair Value of $40.36 (UNDERVALUED)

However, this upbeat narrative can crack if capital intensive club expansion meets tighter real estate financing, or if at home and digital fitness options curb in club demand.

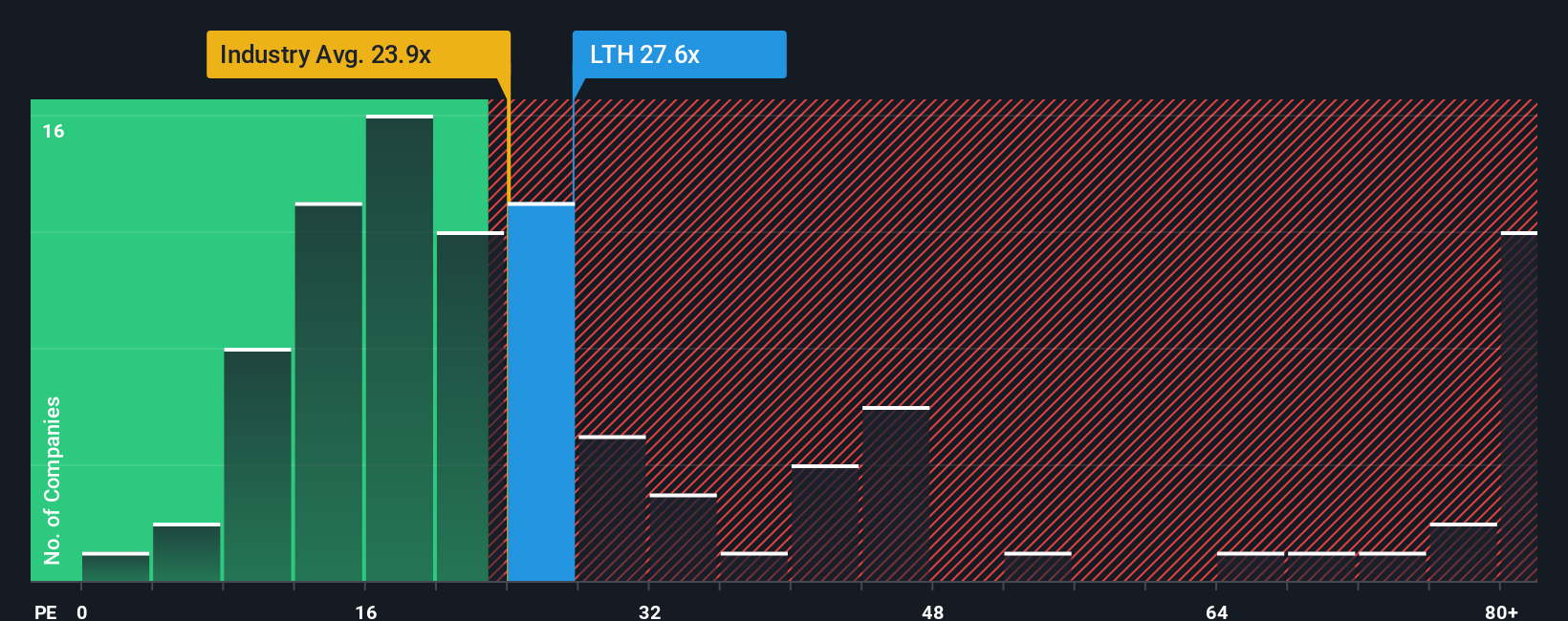

Another angle on value: earnings multiple sends a different signal

While the narrative fair value suggests upside, the current P/E of 22.7x is a bit higher than the Hospitality industry at 20.7x and also above the 21.1x fair ratio our model suggests the market could move toward, even though it sits well below peers at 39.8x. Is that a safety margin, or a sign expectations are already rich?

Build Your Own Life Time Group Holdings Narrative

If you see the story unfolding differently or prefer to test your own assumptions against the data, you can build a custom view in minutes with Do it your way.

A great starting point for your Life Time Group Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use the Screener to spot other opportunities before the crowd catches on.

- Target income potential by scanning for reliable payers using these 11 dividend stocks with yields > 3% that could complement growth focused holdings.

- Tap into long term technology themes with these 30 AI penny stocks and see which businesses are tied to real adoption rather than just hype.

- Hunt for potential mispriced opportunities through these 863 undervalued stocks based on cash flows that may offer more attractive entry points based on their cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.