A Look At Lincoln Educational (LINC) Valuation After Revenue Beat And Raised Full-Year Guidance

Lincoln Educational Services Corporation LINC | 0.00 |

Why Lincoln Educational Services (LINC) is Back on Investors' Radar

Lincoln Educational Services (LINC) recently reported a 19.7% year-on-year revenue increase that came in well above analyst expectations, paired with the largest full-year revenue guidance raise among its peers.

The revenue surprise and raised guidance have coincided with a sharp re-rating in the shares, with a 30-day share price return of 15.54% and a year-to-date share price return of 77.65%. The 1-year total shareholder return of 157.20% points to strong momentum rather than a short-lived reaction.

If this kind of move has you looking for other potential opportunities, it could be worth scanning a wider set of education and service names alongside 18 top founder-led companies

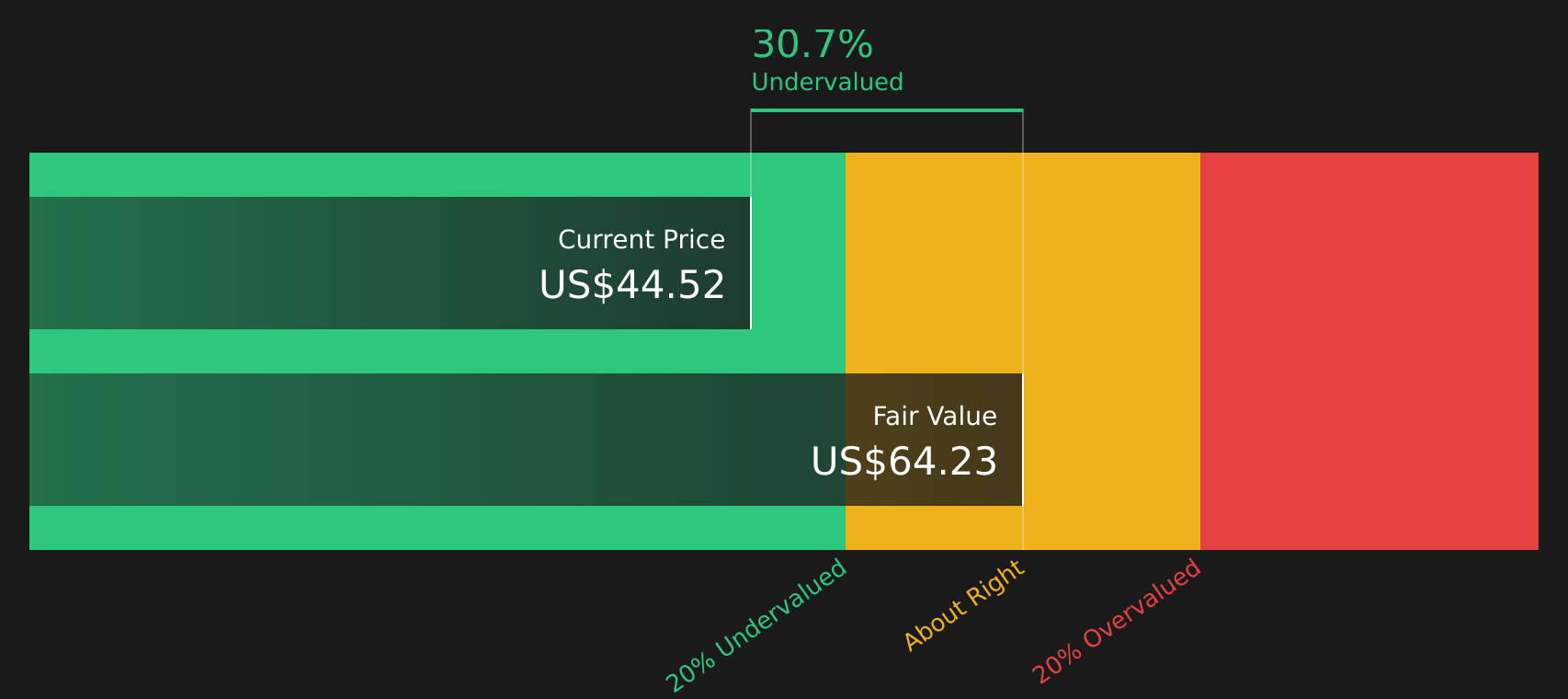

With LINC trading at US$41.41 against an average analyst price target of US$44.40 and an estimated intrinsic value gap of about 38%, investors may ask whether there is still a buying opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 6.7% Undervalued

Lincoln Educational Services' most followed narrative points to a fair value of $44.40 per share, slightly above the last close of $41.41, framing the recent rally within a still supportive valuation story.

Strategic expansion through new campus openings in high-demand, underserved metro areas, alongside program replication at existing sites, is expected to deliver significant incremental revenue and operating leverage. Guidance now calls for two new campus openings annually, with each one targeted to contribute $25–30 million in revenue and $7–10 million EBITDA by year four.

Want to see what kind of enrollment ramp, margin lift, and earnings profile need to line up for that fair value to hold up under a 7.36% discount rate and a premium future earnings multiple? The narrative lays out a detailed road map that connects campus expansion, hybrid programs and employer demand into one tight valuation picture, but keeps the assumptions just bold enough to make you pause and check the fine print.

Result: Fair Value of $44.40 (UNDERVALUED)

However, you still need to weigh the risk that heavy campus capex or tighter student aid rules could leave enrollment, earnings, and the valuation story out of sync.

Another Angle On Valuation

The SWS DCF model points to a fair value of $66.26 per share, which is above both the $44.40 narrative value and the $41.41 market price, and implies LINC is deeply undervalued. If the market is already paying 65.6x earnings, it is worth considering how much of that gap you can comfortably rely on.

Next Steps

If this mix of enthusiasm and caution has you on the fence, now is a good time to dig into the numbers yourself and decide where you stand. Start with 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If LINC has sharpened your focus, do not stop here. Broaden your watchlist with a few focused stock ideas that match how you like to invest.

- Target value: sort through companies that look mispriced on quality and fundamentals using the 61 high quality undervalued stocks.

- Strengthen your foundation: filter for businesses with resilient finances through the solid balance sheet and fundamentals stocks screener (40 results).

- Hunt for future standouts: uncover lesser-known names with strong fundamentals via the screener containing 24 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.