A Look At Lucky Strike Entertainment (LUCK) Valuation After Its Recent Rebrand And Mixed Performance Signals

Lucky Strike Entertainment Corporation Class A LUCK | 0.00 |

Lucky Strike Entertainment: Event Overview

Lucky Strike Entertainment (LUCK) has caught investor attention after its recent rebrand from Bowlero Corp, highlighting a diversified mix of bowling centers and entertainment venues across North America.

At a share price of $8.44, Lucky Strike Entertainment has seen a 6.03% 1 month share price return. Its 3 year total shareholder return of 43.47% decline contrasts with a 3.83% gain over the past year, suggesting recent momentum has improved compared with longer term performance.

If this kind of turnaround story has your attention, it can be useful to widen your search and review 19 top founder-led companies

With the share price at $8.44, a 31.65% discount to the average analyst target, and recent returns mixed across timeframes, the key question is whether this reflects an undervalued turnaround or indicates that the market has already priced in future growth.

Most Popular Narrative: 24% Undervalued

With the narrative fair value sitting at $11.11 against a last close of $8.44, the current price sits well below what the model suggests.

Strong momentum in season pass membership growth and revenue, combined with significant investments in marketing and customer engagement initiatives, are likely to drive higher repeat visitation, increased customer loyalty, and above-trend top-line revenue growth.

Curious what kind of revenue profile and margin mix could justify that gap to fair value? The narrative focuses on profitability turning a corner and a richer earnings multiple to get there.

Result: Fair Value of $11.11 (UNDERVALUED)

However, this narrative still relies on physical venues holding up against digital entertainment, and on a high fixed cost base and US$1.3b net debt not becoming a strain.

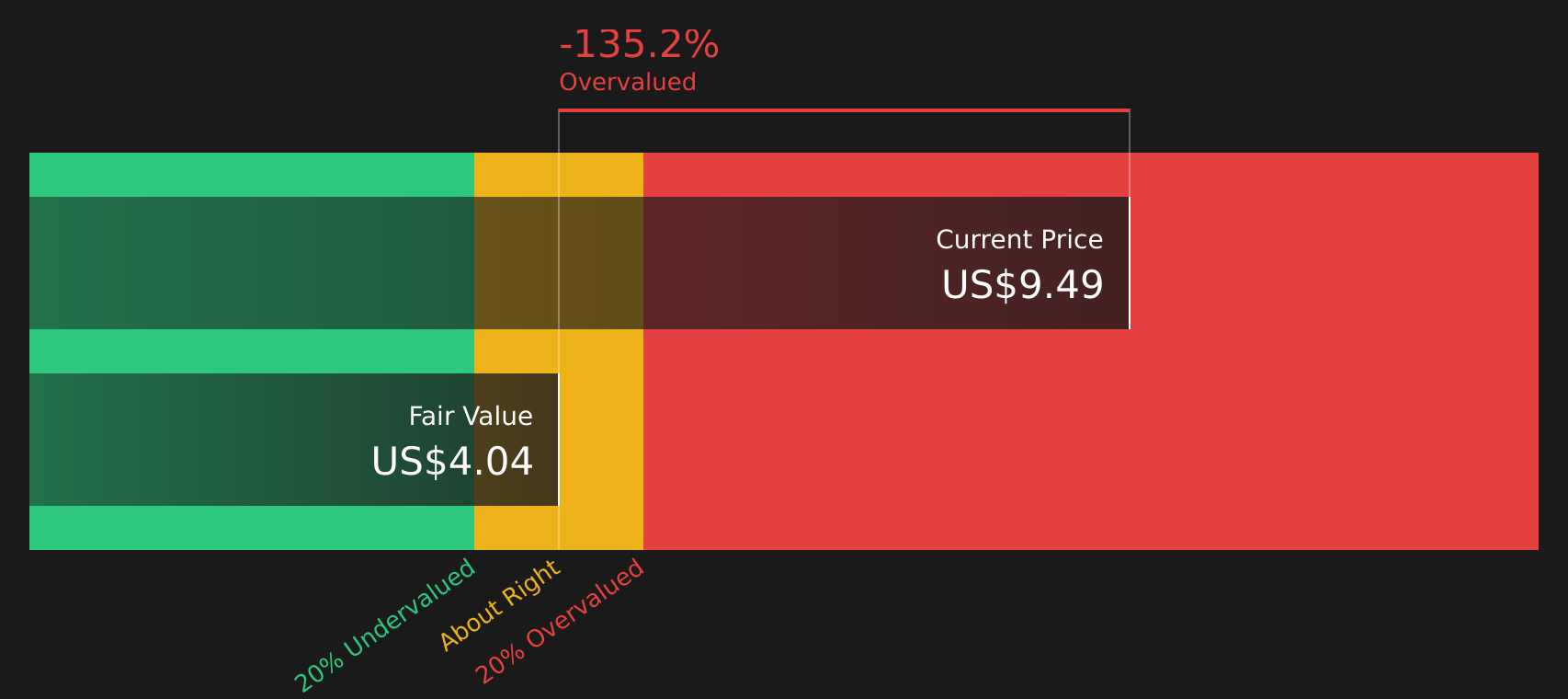

Another View: Cash Flow Model Paints A Tougher Picture

The narrative fair value of $11.11 suggests upside from the current $8.44 share price, yet the SWS DCF model points the other way, with an estimate of $3.93 per share. That is a large gap, and it raises a simple question: which story do you trust more, earnings or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lucky Strike Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 60 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals or a clear set up, either way the next move is yours. Look at the full picture, including the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

Lucky Strike Entertainment may be interesting, but your next great idea could be sitting elsewhere. Take a few minutes now to scan other opportunities before they move.

- Target income-focused opportunities by reviewing companies in the 11 dividend fortresses and see which payouts currently stand out.

- Hunt for quality at a discount by checking the 60 high quality undervalued stocks that combine solid fundamentals with appealing pricing.

- Prioritize resilience by scanning the 72 resilient stocks with low risk scores and focus on businesses with more defensive profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.