A Look At Madison Square Garden Sports (MSGS) Valuation After Stronger In Game Revenues And Media Rights Support

Madison Square Garden Co. Class A MSGS | 324.51 | +1.83% |

Why Madison Square Garden Sports is in focus now

Madison Square Garden Sports (MSGS) is back on investors’ radar after its latest quarterly earnings showed higher in-game revenues across ticketing, suites, sponsorship, and merchandise, supported by increased national media rights fees under new NBA deals.

The company also highlighted benefits from updated local media agreements and team rosters. Management pointed to what it views as strong fundamentals and demand, which has helped draw fresh attention to the stock.

At a share price of $279.29, Madison Square Garden Sports has seen a 26.3% 90 day share price return and a 36.0% 1 year total shareholder return. This suggests momentum has been building around its recent earnings and new partnership announcements.

If this mix of sports assets and media exposure has your attention, it could be a good time to broaden your search and check out 22 top founder-led companies as potential next ideas.

With the shares up sharply over the past year and trading at a discount to the current analyst price target, the key question is whether MSGS still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 10.3% Undervalued

Compared to the last close of $279.29, the most followed narrative puts Madison Square Garden Sports’ fair value at $311.50, framing the recent share price strength in a different light.

Persistent demand for live sports and premium arena experiences, as demonstrated by record-breaking gate receipts and suite revenues, combined with further investments in arena renovations and hospitality, is expected to drive stable or accelerating event-related revenue and higher average revenue per customer.

Curious what turns premium seats and global partnerships into that higher fair value. The narrative attributes it to measured revenue growth, firmer margins and a punchy future earnings multiple.

Result: Fair Value of $311.50 (UNDERVALUED)

However, there are still a few watchpoints, including the step down in local media rights fees and MSGS’s heavy reliance on only the Knicks and Rangers.

Another View: High Sales Multiple Flags Valuation Risk

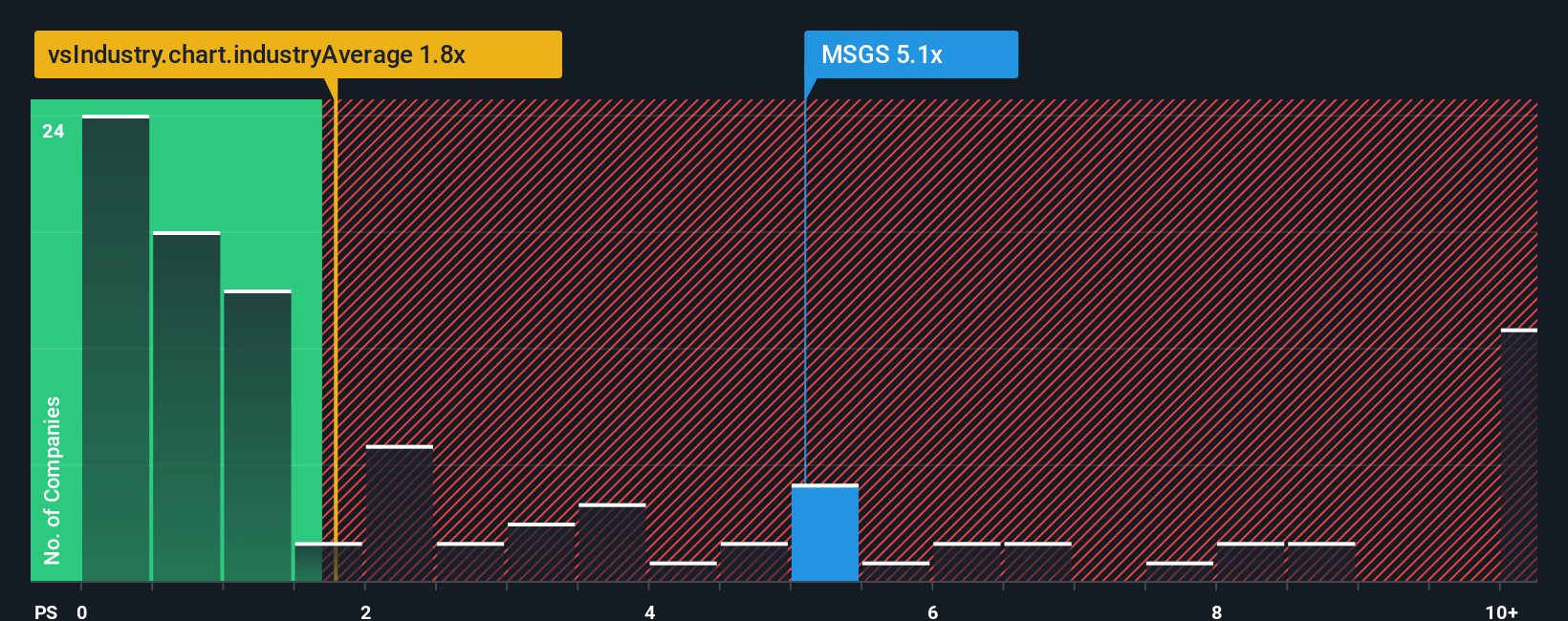

The 10.3% undervalued fair value narrative sits in sharp contrast to how the market prices Madison Square Garden Sports on sales today. The shares trade on a P/S of 6.3x, compared with 1.4x for the US Entertainment industry, 2x for peers, and a fair ratio of 1x.

This wide gap suggests investors are already paying a steep premium for each dollar of revenue, which could limit upside if growth or margins fall short of expectations. The key question is whether you think MSGS can keep justifying such a premium or if that rich multiple eventually normalizes.

Build Your Own Madison Square Garden Sports Narrative

If you see the story differently or prefer to evaluate the numbers yourself, you can build a fresh MSGS thesis in minutes with Do it your way

A great starting point for your Madison Square Garden Sports research is our analysis highlighting 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If MSGS has sharpened your interest in sports and entertainment, do not stop here. The right mix of quality and price often sits just beyond your first idea.

- Target quality at a discount by reviewing 52 high quality undervalued stocks that blend stronger fundamentals with prices that may sit below their estimated worth.

- Prioritize resilience by scanning 82 resilient stocks with low risk scores that score well on stability so sudden shocks are less likely to catch you off guard.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems where solid businesses may still be flying under most investors’ radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.