A Look At Merit Medical Systems (MMSI) Valuation As Insider Buying Follows Undervaluation Claims

Merit Medical Systems, Inc. MMSI | 0.00 |

Recent commentary around Merit Medical Systems (MMSI) has zeroed in on valuation, with intrinsic value and discounted cash flow models suggesting the stock may be pricing in a cautious outlook after a challenging year.

Merit Medical Systems' recent 1 month share price return of 4.62% comes after a tougher spell, with the 90 day share price return down 11.26% and the 1 year total shareholder return down 32.33%. As a result, recent gains look more like a tentative stabilisation than a full change in momentum.

If you are weighing Merit alongside other healthcare names, this can be a moment to scan for opportunities in medical technology using our screener of 39 healthcare AI stocks

With the share price down sharply over 1 year, yet trading at an estimated 34.1% discount to intrinsic value and roughly 38.9% below analyst targets, investors are left with a key question: is this a genuine mispricing, or is the market already accounting for future growth?

Most Popular Narrative: 28% Undervalued

At a last close of $64.48 against a fair value estimate of $89.55, the prevailing narrative sees Merit Medical Systems trading at a meaningful discount, with that gap underpinned by detailed forecasts for revenue, margins and cash flows.

The expanding global prevalence of chronic diseases and an aging population are increasing the need for interventional, diagnostic, and therapeutic medical procedures. Merit's strong growth in cardiovascular and endoscopy segments, robust new product development, and recent acquisitions (such as Biolife and EndoGastric) position the company to capture a larger share of this growing market and drive sustained long-term revenue growth.

Want to see what kind of revenue climb, margin profile and future earnings multiple have to line up to support that valuation gap? The full narrative lays out a tight set of assumptions on growth, profitability and the price investors might be willing to pay if those targets are hit.

Result: Fair Value of $89.55 (UNDERVALUED)

However, this hinges on securing WRAPSODY CIE reimbursement and avoiding further China weakness, where volume based purchasing and softer demand have already pressured international revenue.

Another View: What The P/E Ratio Is Saying

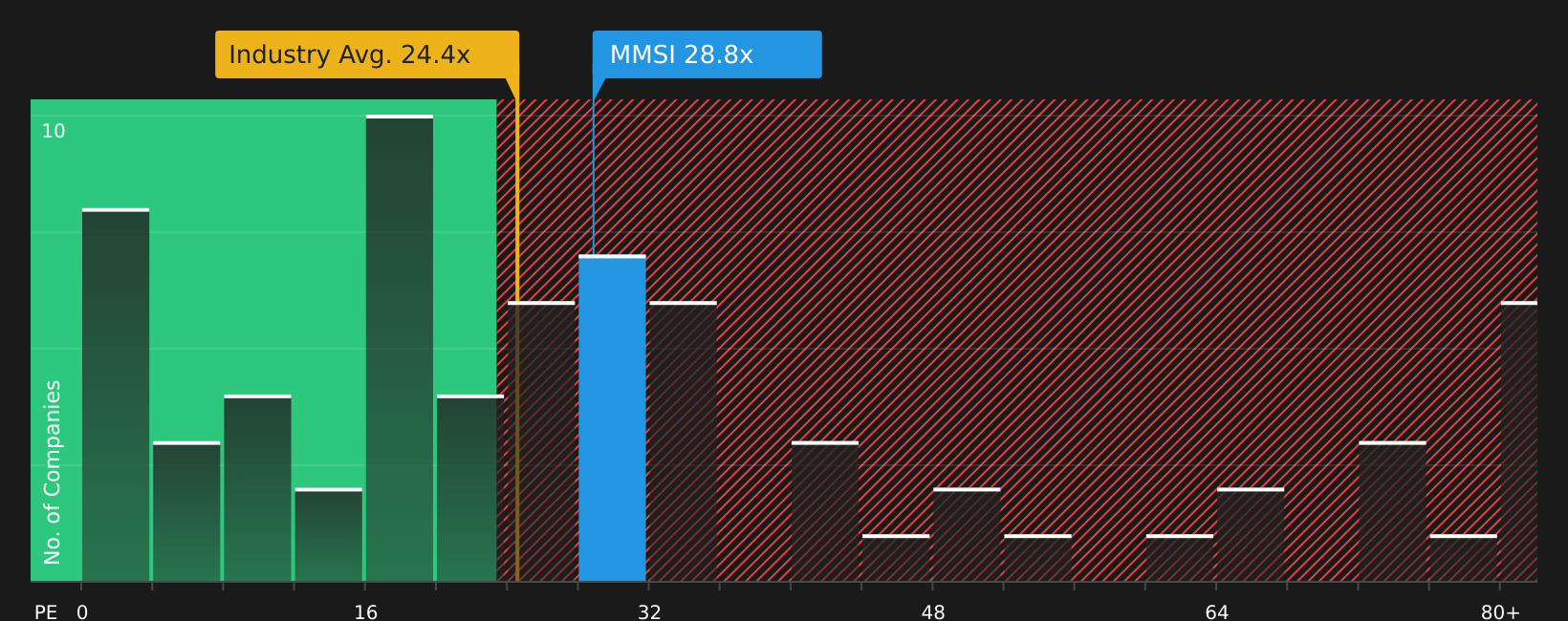

The discount to fair value and analyst targets tells only part of the story. On current numbers, Merit trades on a P/E of 27.6x, which is higher than the US Medical Equipment industry at 25.3x and above its own fair ratio estimate of 21.5x, yet still below a 38.9x peer average. For you, that mix of premium to the sector but discount to peers raises a simple question: is the risk skewed toward the valuation catching up to fundamentals, or the fundamentals catching up to the price?

To see how this compares across peers and what that gap could mean if the market moves closer to the fair ratio, have a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Is the market being too cautious, or simply realistic about the story so far? Take a closer look at the full picture, including the 4 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit your goals even better, so keep widening your watchlist with focused screeners.

- Hunt for potential bargains with solid fundamentals by checking companies in the 49 high quality undervalued stocks.

- Prioritise resilience and sleep a little easier at night by screening for 64 resilient stocks with low risk scores.

- Spot strong balance sheets that can support future plans by scanning the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.