A Look At Mirum Pharmaceuticals (MIRM) Valuation After Bluejay Deal And Strong 2025 And 2026 Revenue Update

Mirum Pharmaceuticals MIRM | 94.17 | -0.48% |

Why Mirum’s latest acquisition and sales update matter for investors

Mirum Pharmaceuticals (MIRM) has just closed its purchase of Bluejay Therapeutics and reported unaudited 2025 net product sales that topped earlier guidance, alongside a 2026 revenue outlook that points to stronger top line expectations.

Investors have reacted positively to Mirum’s deal making and sales update, with a 30 day share price return of 35.07% and a 90 day share price return of 50.45% pointing to strong recent momentum. Meanwhile, the 1 year total shareholder return of 110.02% and 3 year total shareholder return of more than 3x show how the story has built over time.

If this kind of rare disease growth story interests you, it may be worth widening your watchlist to include other healthcare stocks that could be shaping similar themes in the sector.

After a share price that has already more than doubled over the past year, and a recent run of upbeat sales news, the key question now is simple: is Mirum still mispriced, or is the market already banking on further growth?

Most Popular Narrative: 1.1% Undervalued

Mirum Pharmaceuticals closed at $105.45, while the most followed narrative pegs fair value at $106.60, a small gap that still rests on some punchy assumptions.

Multiple late-stage pipeline catalysts, including three pivotal study readouts (VISTAS, VANTAGE, EXPAND) over the next 24 months and the initiation of the Phase II Fragile X study, set the stage for further product label expansions and new indication launches, underpinning future revenue diversification and potential earnings acceleration.

Want to see what kind of revenue ramp, margin shift, and future earnings multiple have to line up for that fair value to hold up? The narrative leans on ambitious growth, richer profitability, and a premium valuation usually reserved for larger biotechs. Curious how those pieces fit together and what has to go right to support that price tag? Read on to see the full reasoning that sits behind the number.

Result: Fair Value of $106.60 (UNDERVALUED)

However, that story can unravel quickly if Livmarli underperforms expectations or if key late stage trial readouts and regulatory decisions do not land as hoped.

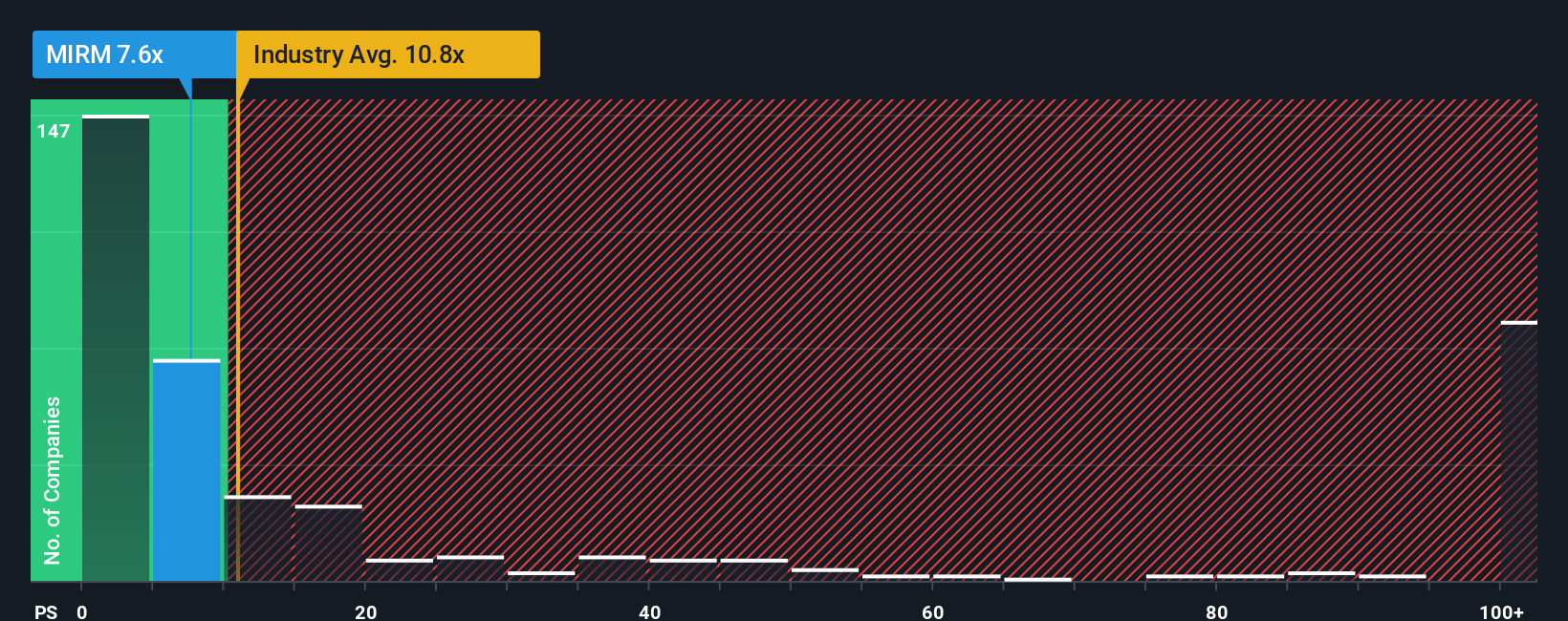

Another View: Rich Sales Multiple Keeps Expectations High

While the narrative and our cash flow work suggest Mirum is trading about 5.6% below an estimated fair value of $111.75, the P/S ratio tells a different story. At 13.4x sales versus a fair ratio of 8x, and 11.8x for the US Biotechs industry, you are paying a premium that assumes a lot goes right. How comfortable are you with that gap?

Build Your Own Mirum Pharmaceuticals Narrative

If you see the numbers differently or simply prefer to test your own assumptions against the data, you can create a custom Mirum view in just a few minutes, starting with Do it your way.

A great starting point for your Mirum Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Mirum has caught your attention, do not stop here. Use the screeners below to spot other opportunities that could suit your style before the crowd catches on.

- Tap into strong cash flow potential by focusing on these 873 undervalued stocks based on cash flows that our models flag as trading below their estimated worth.

- Zero in on future focused companies by tracking these 25 AI penny stocks that are building real businesses around artificial intelligence.

- Strengthen your income game by filtering for these 13 dividend stocks with yields > 3% that can add steady yield to your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.