A Look At Moody’s (MCO) Valuation As Shares Sit Slightly Below Estimated Fair Value

Moody'S MCO | 0.00 |

Moody's stock performance snapshot

Moody's (MCO) has drawn investor attention after recent share price moves, with the stock up 0.6% over the past day and 0.9% over the past week, while showing declines over the past month and past 3 months.

At a last close of US$453.25 and a market value of about US$79.2b, the company sits within the diversified financials sector, combining a large credit ratings operation with a sizable analytics and risk solutions business.

For context, Moody's share price is down 9.2% year to date, while the 3 year total shareholder return of 41.3% indicates that investors who stayed invested over a longer period have seen a substantially stronger outcome.

If you are comparing Moody's with other financial market infrastructure and data providers, it can also be useful to look at companies driving the backbone of modern AI and data analytics, such as those in AI infrastructure and related services, using the 47 AI infrastructure stocks

With Moody's stock down 9.2% year to date but showing a 3-year total return of 41.3%, along with ongoing revenue and net income growth, should you view the current share price as an opportunity, or assume that the market already reflects these growth prospects?

Most Popular Narrative: 4.2% Undervalued

According to the most widely followed narrative, Moody's fair value of $473.36 sits a little above the recent $453.25 share price. This frames the current valuation debate in a fairly tight range.

Ultimately, Moody’s represents a rare combination of financial infrastructure dominance and software-like economics. It is a business designed to become more valuable as global debt markets expand, regulations grow more complex, and financial institutions require deeper risk analytics. For long-term investors, the thesis is less about predicting the next quarter and more about owning a near-irreplaceable piece of the global capital system.

Want to understand what underpins that valuation gap? The narrative leans heavily on robust profit margins, steady revenue expansion and a future earnings multiple that assumes Moody's continues to compound at scale. Curious which specific growth and margin assumptions sit underneath that fair value and how they translate into the projected earnings profile over time?

Result: Fair Value of $473.36 (UNDERVALUED)

However, this depends on continued regulatory reliance on Moody's and on AI reinforcing, rather than eroding, the value that investors and issuers place on its ratings.

Another angle on Moody's valuation

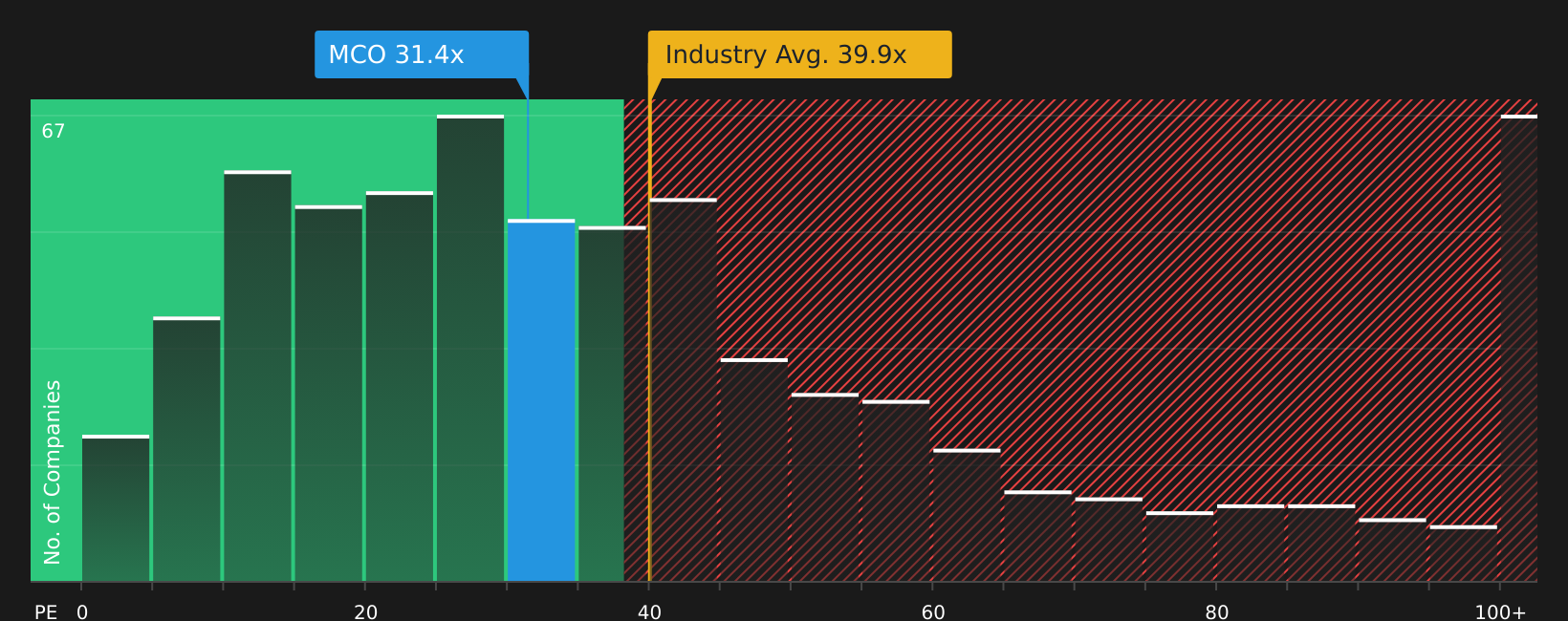

While the narrative fair value of $473.36 suggests Moody's stock is 4.2% below that estimate, the current P/E of 31.7x tells a different story. It sits below the US Capital Markets industry average of 39.5x, but far above the fair ratio estimate of 17.6x, which points to meaningful valuation risk if sentiment cools.

Against that backdrop, are you more persuaded by the earnings multiple the market applies today, or by the long term narrative that argues the premium is justified?

Next Steps

Seeing mixed messages in the story so far? Take a moment to weigh the potential risks against the upside and shape your own view with the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Moody's has sharpened your thinking, do not stop here. Use the Simply Wall Street Screener to spot other stocks that could suit your portfolio.

- Target value opportunities by checking companies that appear mispriced on fundamentals with the 46 high quality undervalued stocks

- Prioritise resilience by focusing on businesses with strong finances using the solid balance sheet and fundamentals stocks screener (46 results)

- Get ahead of the crowd by scanning for underfollowed stocks with solid metrics through the screener containing 22 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.