A Look At New Oriental Education & Technology Group’s Valuation After Upgraded 2026 Guidance And Strong Quarterly Results

New Oriental Education & Technology Group, Inc. Sponsored ADR EDU | 0.00 |

New Oriental Education & Technology Group (EDU) is back in focus after reporting third quarter results that show higher sales and net income versus a year earlier, alongside raised full year 2026 revenue guidance.

The stock has had a choppy few months, with a 30 day share price return of a 4.7% decline and a 90 day share price return of a 14.3% decline. However, the 1 year total shareholder return of 12.43% still points to longer term holders being ahead. This suggests that recent earnings, guidance upgrades and the ongoing buyback and dividend may be helping support sentiment despite fading short term momentum.

If New Oriental’s latest earnings have you looking beyond a single stock, this is a good time to see what else is moving in education focused technology. Check out 17 top founder-led companies

With stronger recent earnings, higher full year revenue guidance, and a completed share buyback in play, the key question now is whether EDU at about US$53 is still undervalued or if the market has already priced in future growth.

Most Popular Narrative: 24.1% Undervalued

With New Oriental’s fair value from the most followed narrative sitting at $70.80 versus a last close of $53.77, the current setup assumes a meaningful valuation gap that hinges on execution in newer business lines and capital returns.

Strong momentum and high year-over-year growth in new non-academic tutoring and AI-powered learning products reflects growing consumer demand for enrichment and personalized education, positioning the company to benefit from continued societal prioritization of premium educational services. This should support long-term revenue growth and improve blended margins due to scale and higher retention.

Curious what underpins a fair value well above today’s share price? The narrative leans on compound revenue growth, fatter margins and a higher future earnings multiple. The exact mix of those assumptions is where the story gets interesting.

At the core of this fair value is a set of analyst expectations that revenue will continue to grow, margins will be higher than today, and earnings will expand faster than the top line, all discounted back at 7.76%. The implied 20.4x future P/E also sits above the current Consumer Services average, so the narrative effectively argues that EDU should carry a premium as long as execution in AI-driven learning, non-academic services and capital returns stays on track.

Result: Fair Value of $70.80 (UNDERVALUED)

However, the story can unravel if overseas study demand weakens further or if intensifying competition in K 12 and non academic segments squeezes margins more than analysts expect.

Another Angle: Multiples Look Less Generous

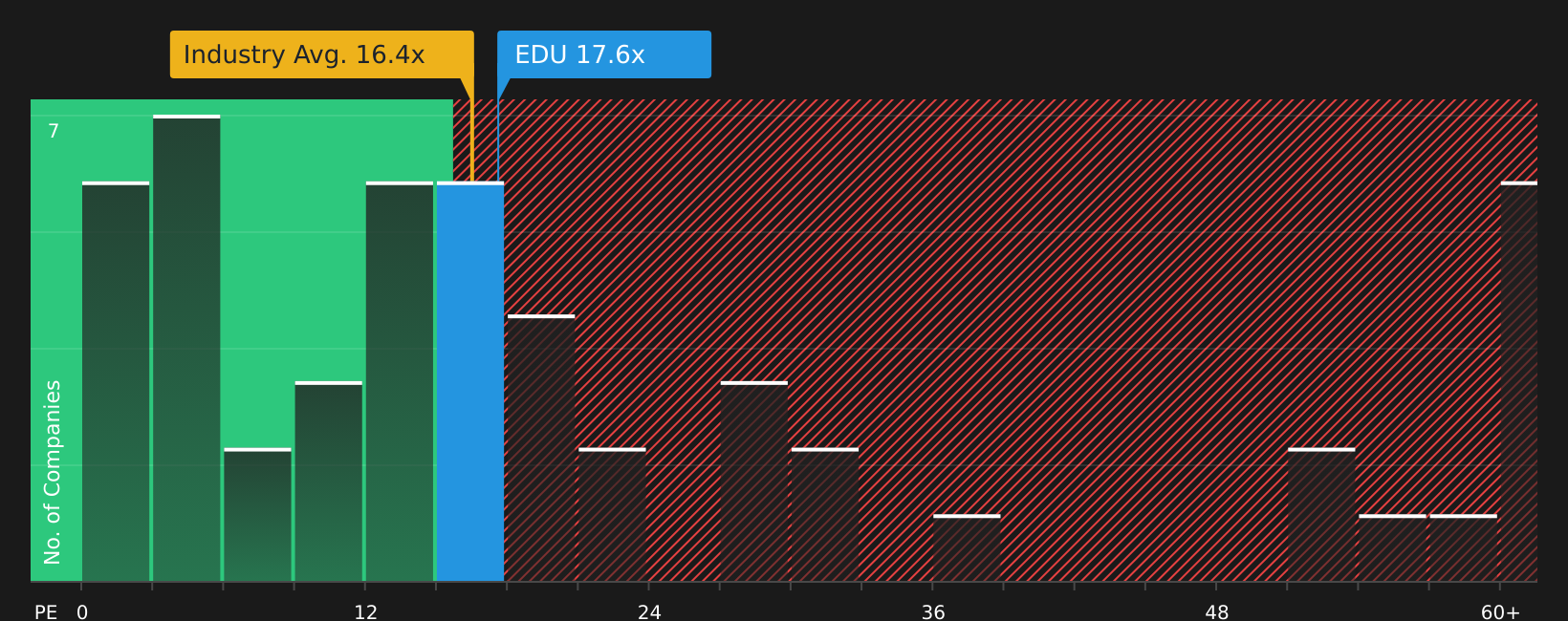

That 24.1% discount to fair value sits alongside a P/E of 20.1x, compared with 16.5x for the US Consumer Services industry and 15.8x for peers. Even against an estimated fair ratio of 27.2x, the current premium to sector and peer averages raises a simple question: How much optimism are you comfortable paying for?

Next Steps

Seen enough optimism and questions to make you curious about what really stands out here? Act while the details are fresh and weigh the potential yourself, starting with 4 key rewards.

Looking for more investment ideas?

If EDU has sharpened your interest, do not stop here. Broaden your watchlist with a few focused screens that highlight different types of opportunities.

- Target potential mispricings by reviewing companies flagged in the 48 high quality undervalued stocks.

- Prioritize resilience by checking stocks highlighted in the solid balance sheet and fundamentals stocks screener (44 results).

- Spot under the radar potential by scanning the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.