A Look At NextEra Energy (NEE) Valuation As Power Backlog And AI Demand Support Growth Narrative

NextEra Energy, Inc. NEE | 93.15 | +0.32% |

NextEra Energy (NEE) is back in focus after confirming approvals for up to 10 gigawatts of natural gas generation in Texas and Pennsylvania, tied to Japan's US$550b investment commitment under the U.S. Japan trade deal.

Those approvals arrive as the stock trades at US$93.15, with a 90 day share price return of 15.1% and a 1 year total shareholder return of 33.0%, suggesting momentum has been building alongside new power projects and rising interest in utility scale power for AI data centers.

If this kind of large scale power build out has your attention, it is a good moment to see what else is setting up for long term growth in 28 power grid technology and infrastructure stocks

With shares near US$93 and trading only about 2% below the average analyst price target, along with a value score of 1 and strong recent returns, is NextEra still mispriced, or is the market already factoring in the next leg of growth?

Most Popular Narrative: 1% Undervalued

NextEra Energy's most followed narrative pegs fair value at $93.65, almost exactly in line with the last close at $93.15, which keeps the focus on the assumptions behind that result rather than any big headline discount.

Recently enacted federal legislation (OBBB) and safe harbor provisions provide multi year tax and regulatory visibility through at least 2029 for wind, solar, and storage projects, which, combined with a large existing project backlog and strong balance sheet, allow NextEra to secure project returns, support dividend growth, and maintain healthy net margins despite broader policy uncertainty.

Curious what kind of revenue climb, margin profile, and future earnings multiple are built into that near match between price and fair value? Those moving parts, plus a specific discount rate, sit at the core of this narrative and explain why a utility scale power provider can be modeled at a premium to many sector peers while still landing so close to the current share price.

Result: Fair Value of $93.65 (UNDERVALUED)

However, this fair value story still depends on policy support for renewables and manageable financing costs. Setbacks on tax credits or a prolonged period of higher rates could quickly challenge it.

Another Angle On Valuation

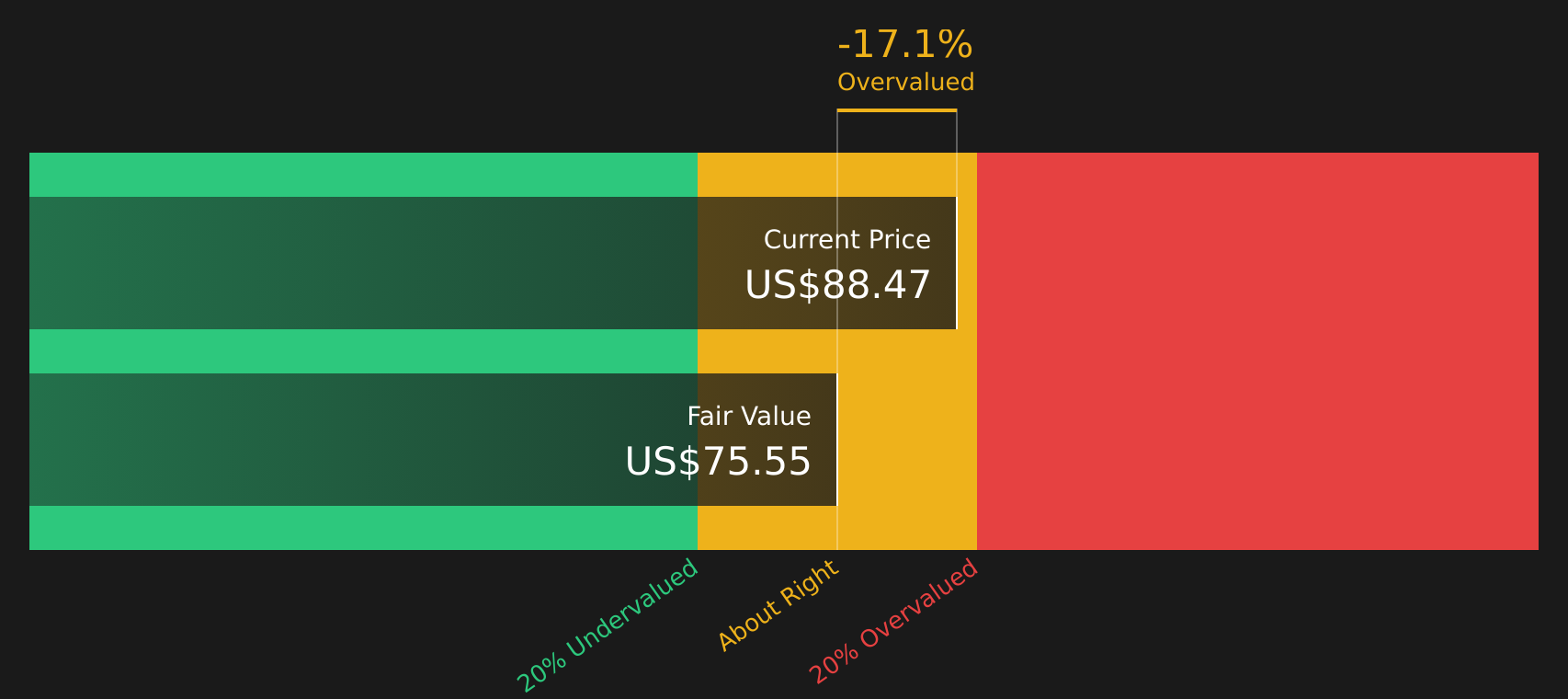

The fair value narrative suggests NextEra Energy is only about 1% undervalued at $93.65, but the SWS DCF model presents a different picture, with a future cash flow value of $76.53 and the current $93.15 share price sitting above that. Which perspective is more consistent with how you think cash flows should be priced?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NextEra Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and plenty of debate in the background, it makes sense to move fast and test the story against the data yourself. To weigh both the upside and the concerns side by side, start with 1 key reward and 2 important warning signs

Looking for more investment ideas?

If you stop at just one company, you risk missing other opportunities that match your style, income needs, and comfort with risk, so broaden your search now.

- Target potential value opportunities early by scanning 62 high quality undervalued stocks that combine quality fundamentals with room for re rating.

- Strengthen your income stream by checking out 12 dividend fortresses built around higher yield payouts that may suit long term holders.

- Protect your downside by filtering for 67 resilient stocks with low risk scores that focus on resilient balance sheets and more stable risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.