A Look at NRG Energy's Valuation Following Strong Earnings and $617 Million Houston Expansion News

NRG Energy, Inc. NRG | 149.90 | +2.57% |

NRG Energy (NRG) attracted investor attention after reporting earnings and revenue that surpassed expectations for several quarters. The company also announced plans for a $617 million natural gas power plant in Houston, supported by a substantial Texas Energy Fund loan.

NRG Energy’s positive earnings run and news of its major Houston plant build have fueled strong momentum, with the share price surging 82.7% so far this year. Investors who stayed patient have been well rewarded too; the company’s robust 1-year total shareholder return sits at 69%, and over the past five years, it has delivered a hefty 468% total return. Both short- and long-term performance underline that optimism is building around NRG’s future prospects.

If you’re interested in discovering what other fast-growing, high-insider-ownership companies are catching attention right now, check out fast growing stocks with high insider ownership.

Despite this exceptional run, NRG Energy still trades at a notable discount to analyst price targets. Is the market underestimating the company's future growth, or has the stock’s recent surge already factored in the potential upside?

Most Popular Narrative: 18.6% Undervalued

With the most followed narrative assigning a fair value of $208.14 versus a last close of $169.49, NRG Energy's current price appears to offer substantial upside. The attention stems from a blend of ambitious growth drivers and operational strategy that analysts believe could transform its medium-term outlook.

"NRG is executing on integrating digital and decentralized technologies, with rapid adoption of smart home offerings (Vivint platform) and residential Virtual Power Plant (VPP) initiatives performing far better than expected. This is likely to drive incremental cross-sell revenue, customer retention, and higher recurring EBITDA in coming years."

Want to know why this narrative sees NRG commanding such a sizable premium? Behind the scenes are eye-catching projections for future profits, surprising margin expansion, and ambitious financial targets. Curious which bold assumptions support this valuation? The details await you in the full story.

Result: Fair Value of $208.14 (UNDERVALUED)

However, ongoing regulatory shifts or setbacks in integrating new assets could quickly challenge the optimistic case for NRG Energy’s long-term earnings growth.

Another View: Looking at Market Multiples

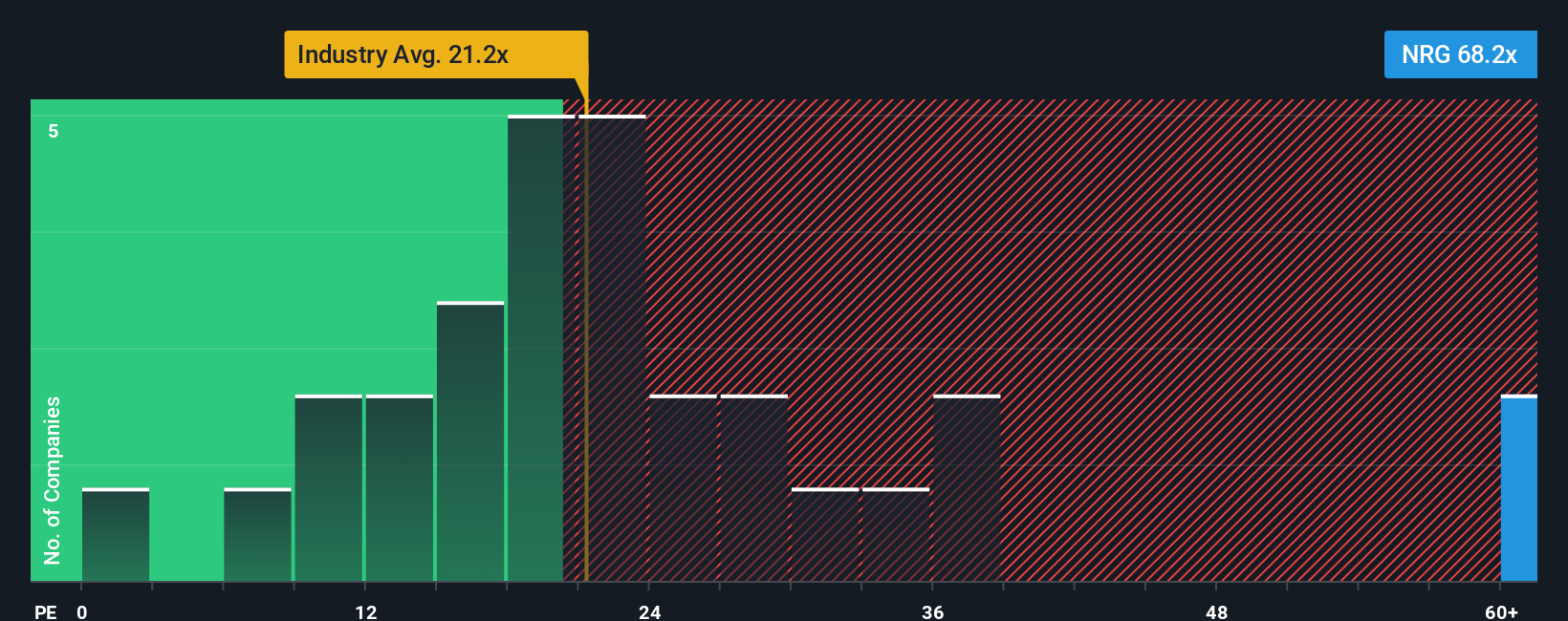

While the fair value narrative suggests NRG Energy shares are undervalued, a quick look at its price-to-earnings ratio tells a different story. NRG’s current P/E stands at 23.6x, higher than both the industry’s 21x and the peer average of 19.5x. However, it remains below the fair ratio of 39.6x. This creates a curious setup, as strong optimism might already be reflected in today’s price, increasing the risk that any disappointment could trigger a sharp market reaction.

Build Your Own NRG Energy Narrative

If you’re keen to challenge the consensus or want to shape the story your own way, you can quickly build your own perspective with just a few clicks. Do it your way.

A great starting point for your NRG Energy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Compelling Investment Opportunities?

Why stop at one winner? Uncover fresh stocks that could supercharge your portfolio by checking out these high-potential ideas available right now.

- Unlock steady streams of income with these 15 dividend stocks with yields > 3%, which features attractive dividends above 3%.

- Capitalize on market mispricings by reviewing these 921 undervalued stocks based on cash flows, which some experts believe are overlooked and trading below their intrinsic value.

- Explore companies that are redefining industry standards with these 25 AI penny stocks and are backed by robust growth engines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.