A Look At NXP Semiconductors (NXPI) Valuation After Strong Q1 Results And Upbeat AI And Data Center Outlook

NXP Semiconductors NV NXPI | 0.00 |

NXP Semiconductors (NXPI) drew fresh attention after its first quarter 2026 report, which showed higher sales and earnings, upbeat second quarter guidance, and an update on its multi year share repurchase program.

The stock has pulled back with a 1 day share price return of a 4.35% decline and a 7 day share price return of a 1.11% decline, but that follows a 48.80% 30 day share price return and a 56.91% 1 year total shareholder return. This suggests that momentum has been strong over both recent and longer periods.

If NXP’s recent AI and data center headlines caught your eye, it can be worth seeing what else is moving in the sector through 40 AI infrastructure stocks

After a Q1 surge, a strong AI and data center story, and upbeat guidance, the stock now trades close to analyst targets. Is there still mispricing on the table, or is the market already pricing in future growth?

Most Popular Narrative: 11.3% Overvalued

With NXP Semiconductors last closing at $290.35 against a narrative fair value of $260.84, the current price sits above that widely followed estimate, putting the focus squarely on what needs to go right to justify the gap.

The company's acquisitions (e.g., TTTech Auto, Kinara, Aviva Links) are focused on enhancing NXP's position in secure, connected automotive and Edge AI solutions, which is a direct play on the global shift toward secure digital payments, identity authentication, and smart mobility. These moves are anticipated to drive medium

and long-term revenue acceleration and bolster NXP's gross margin profile as these segments scale. Read the complete narrative.

Curious what earnings path, margin profile, and future valuation multiple would need to line up for that fair value to make sense? The narrative breaks those moving parts into concrete assumptions and shows exactly how they add up to its price target, so you can compare them with your own expectations before deciding what feels realistic.

Result: Fair Value of $260.84 (OVERVALUED)

However, there are clear watchpoints, including intense China competition and higher operating and inventory costs that could pressure margins if end demand or pricing softens.

Another View: Multiples Paint A Different Picture

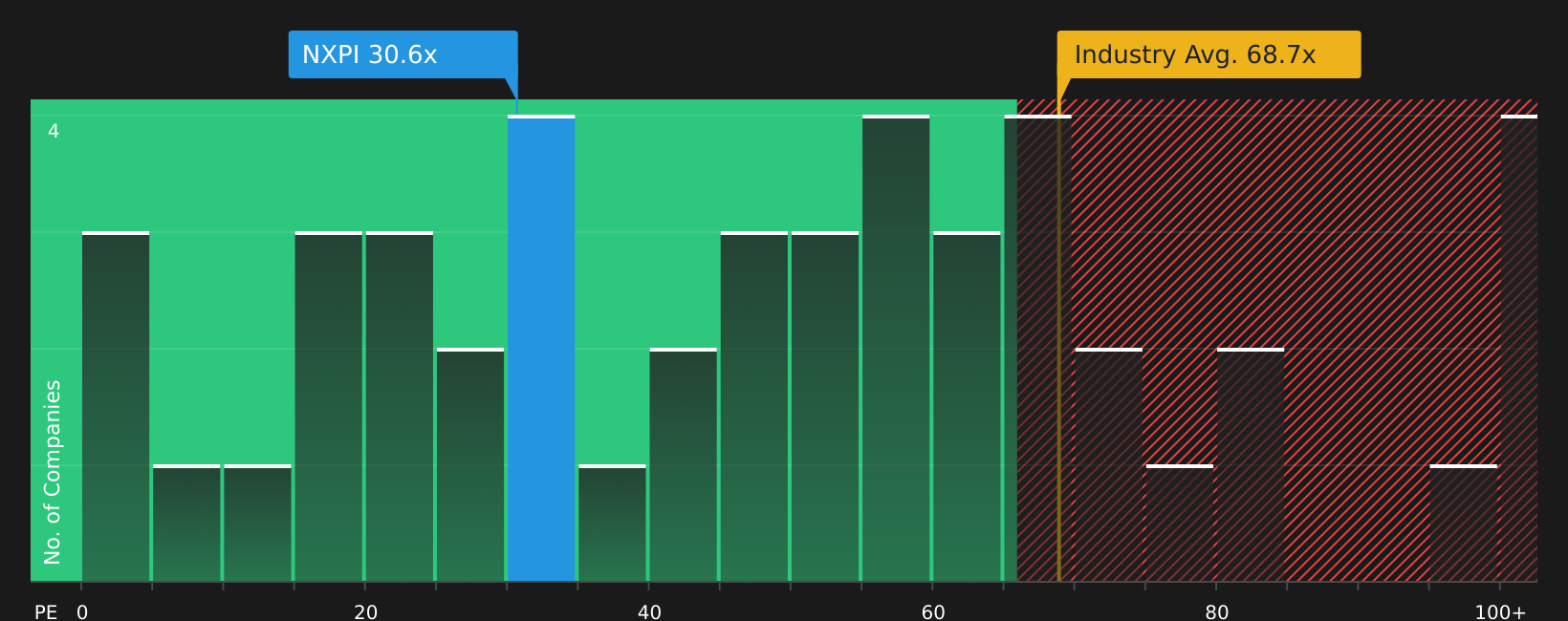

The narrative fair value of $260.84 points to NXP Semiconductors looking overvalued, yet the stock trades on a P/E of 27.6x, compared with 59.4x for the US Semiconductor industry and a fair ratio of 36.6x. That gap suggests investors are paying a lower multiple for each dollar of earnings than both peers and the fair ratio imply, so is the overvaluation story really that clear cut?

Next Steps

Feeling torn between the bullish story and the valuation questions raised so far? Act while the details are fresh, and weigh the upside against the watchpoints yourself with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If NXP has sharpened your focus, do not stop here. Broader context across sectors and styles can help you spot opportunities you might otherwise miss.

- Target dependable compounding potential by scanning companies with strong fundamentals and resilient finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Hunt for quality at a reasonable price by checking companies highlighted in the 51 high quality undervalued stocks before valuations move away from you.

- Strengthen your income playbook by reviewing stocks featured in the 12 dividend fortresses while yields and payout histories still look compelling.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.